I see USD 218 Mio. for the whole ETF in the latest factsheet. For just one year since inception, this doesn’t seem that bad to me. I’d suggest trading when liquidity is highest, which is typically in the afternoon when US exchanges are open as well.

Out of curiosity, do you have a financial reason for this or is it solely for keeping it extremely simple?

A 1% currency conversion fee on 2% dividends results in a cost of 0.02% p.a. If you weren’t already invested, you could even go with 90% VEVE and 10% VFEM where you have those unwanted USD dividends but you’d have a 0.13% TER with otherwise equivalent holdings as VWRL (0.22% TER). I.e. VEVE+VFEM would be significantly cheaper than a hypothetical VWRA in CHF.

If you anyway invest regularly, the extra effort is negligible, in my opinion, just roll the dividends into your next trade. If you invest less regularly, I can understand if you don’t want to do extra trades.

Also keep in mind that foreign accumulating ETFs such as V3AA and VWRA don’t pay any Swiss taxes, i.e. you have to use your liquidity to pay dividend (and wealth) taxes.

Right. So 700 CHF + 900 CHF. 1’600 CHF. They’re nuts here in Switzerland…

I saw my number somewhere else. In the factsheet it says:

Total assets (million) $227 | Share class assets (million) $135 as at 28 February 2022

So yeah, you’re right, it’s more. Just not sure what the other number means.

It is only for the sake of minimalism. I am really obsessed about keeping things simple. I’m disgusted by chaos and repetitive chores

I’m not that convinced that the TER really makes the nominal difference. When you compare ETFs which track the same index but have a different TER, I noticed they don’t necessarily diverge in return.

I don’t really invest regularly, more like in tranches. But let’s say I’d like to do it once a quarter. It’s not just about the effort of converting the USD to CHF and reinvesting. It is also about the tax statement and all those unnecessary transactions that are generated with a distributing ETF. I really thought that if an ETF is traded in CHF, also the dividend is paid out in CHF.

You should factor in that SwissQuote / PostFinance charge a lot for currency exchange (0.5% or sth?). So you’d bleed 0.5% off each dividend.

I think you formulated this sentence a bit confusingly why should an ETF pay taxes? But yes, I know, no dividend is paid, that’s the point of the ETF. Yet the income tax is still due. I think once I’m retired and rely solely on this ETF, I will need to make a sale let’s say once a year to cover my living costs and taxes. This I would anyway have to do as the regular dividend of 2% will probably not be enough to cover living costs.

The ETF has two share classes, accumulating and distributing. They are both part of the same fund, though. USD 227 Mio. is for the whole fund, USD 135 Mio. is for the accumulating share class alone. An important factor whether to keep a fund alive is the AUM for the whole fund. For Vanguard it shouldn’t matter how much money is in the accumulating share class and how much is in the distributing share class.

This really depends on the ETF. E.g. the iShares MSCI ACWI ETF has significant and varying tracking error (up to 0.7%), presumably because it uses sampling, only investing in 1’671 holdings (compared to 2’900 in the index). However, the mentioned Vanguard ETFs follow the indices much closer. E.g. VWRL investing in 3’804 out of 4’088 index holdings with an average tracking error of 0.02%. For V3AA it’s 5’892 out of 8’057 but that’s probably reasonable given the inclusion of Small Cap.

You’ll also need a line for dividends for accumulating ETFs. It will be a single line instead of a quarterly line. Good tax software handles this automatically, though, so the only real downside is a potentially longer WV, unless your canton’s tax software is painful to use.

I’ve even assumed 1% in my example calculation above. Swissquote charges 0.95% for conversion < 50k.

I meant this in comparison to CH-domiciled funds, which do withhold 35% of dividends even if the fund is accumulating.

More like 1%. So it costs you like 0.02% per year.

Your transaction makes sense if your invested money times number of years you hold it is more than 8 000 000 CHF. So for example 400k which you don’t touch for next 20 years. But if in 1 year you decide to sell and buy again, you have lost a non-mustachian load of money.

Also note that with a distributing ETF you need less transactions to get money when you need them, so this alone might speak against an accumulating ETF which is expensive to sell.

I’m using the web version of ZH Private Tax, it does everything automatically indeed. And yeah, I know, the accumulating ETFs have 1 line for the whole year in ICTax.

Sorry I overlooked it. Yes 1% of 2% is 0.02%. Additionally this ETF has small caps and ESG, which could also influence the return (although it’s unknown if positively).

ok now I get it.

Well, I’m stll undecided. It’s a lot of money to spend on such a minor correction, I wish I have invested in V3AA from the start.

Yes, of course. Already once I sold VUSA & VEUR to buy VWRL when I moved from CT to PF. My goal is to hold that ETF for 20 years, as you said, and yes it is around 400k. That is unless this ESG decision proves to be a mistake.

With PostFinance, the fee is regressive with the amount. I don’t think the fee would make much difference if I had to pay out 20k or 40k. The stamp duty would also be manageable. We’re talking maybe max 100 CHF per year of extra cost.

I don’t actually plan to send any more money to IB. My whole TSLA sits there and I expect it to grow a lot in the next decade. If I’m super lucky with it, by the end of the decade I could be looking to exceed the estate tax threshold. And I don’t want to place so much of my wealth in a US-domiciled asset and a US broker. So I keep the ETF part in Switzerland, even if it costs a lot. Call it an insurance policy.

Oh, and I was thinking, there is a possibility that if the TSLA investment goes well and it starts paying dividends, I would use it to pay my living costs and if there was anything left, I would send it to Switzerland and put it into VWRL/V3AA. So it could be that I would not need these dividends for a long time.

I mean, if TSLA reaches 90% of my portfolio, I will have to rebalance. But I don’t want to sell any shares. So if there are dividends, I would use them to buy the ETF and slowly rebalance over years.

It’s spare change, compared to even the intraday volatility in your TSLA investment.

I don’t quite get the discussion here.

You stated you want to invest in a more “ethical” fund.

You also stated that you don’t want to do it all in the U.S.

It all doesn’t sound as if it was about “most cost-efficiency”.

So just do it and make the switch!

Am I missing something?

That’s true. Like, in the 10 days that I was pondering my costly switch to V3AA its price has gone from $4.92 to $5.26. If we’re talking about 100’000 shares, that’s a loss of $34’000, more than I’ll pay for any kinds of fees in my entire life. But it can go both ways. I don’t know if it’s actually correct to compare these two things.

I was just expressing the pros and cons that I see and waiting for any additional feedback from the crowd. If I do this and it’s a bad decision, I will needlessly spent 1’600 CHF.

Think about what’s important for you. How important are your pros, e.g. simplicity without dividend and ESG? Plus, put the CHF 1’600 into context regarding duration of your investment. How much will it be if you plan to invest for another 10 or 15 years, in terms of percentage.

On a side note: think about how long you have been thinking about switching to V3AA (internally, here in the forum asking questions etc). You are also kinda self-employed, so just calculate those hours vs. your rate.

As a last note: set yourself a due date / time. E.g. “I’m not going to spend more than 2 hours for this topic going forward”. Then you concentrate on the things which are really important, which is taking a decision. Your mind is trying to trick you into overthinking, when in reality you are just scared because of the total amount (which is small compared to the amount you invested)

@FIREstarter Good points. Of course we’re prone to overthink our decisions. I would just like to have a really lean financial setup, make all the planning and tough decisions now and then stick to it. But I made mistakes over the years, and reshuffled my portfolio again and again. First I went with Corner Trader and VUSA + VEUR, then I added IB and VT, then I closed CT and moved to PF, sold VUSA & VEUR and bought VWRL (simplicity was the motivation), finally I sold VT and bought TSLA. And each time the plan was to “stick with it for 20+ years”, but as I learned along the way, and as my preferences changed, I found the need to tweak.

@Patron I know I could do this, I just think I am too much of a perfectionist. It will bug me for years to come that I have 2 ETFs that do the same thing. I’m sick, I know . I can’t even stand that I have another World ETF in my 3rd pillar.

I’m with you on this ! I started with VWRL and then (I think 4 years ago) switched to VTI+VEA+VWO, but kept my VWRL shares to avoid losing some money in transactions… but it still bugs me every time I log into my IB account and see it !

But at the end of the day, the performance can be fairly similar to other relatively close products - there is no need to stick to that one in particular.

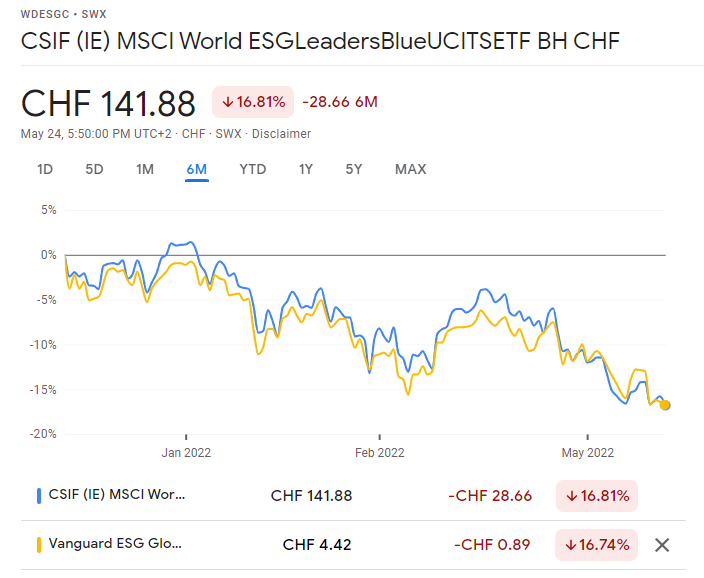

Below is a comparison with WDESGC.SW, hedged in Swiss francs, TER 0.18%.

Global EU-based ETFs are rather expensive, but it’s changing. Amundi Prime Global, LU2089238203 has a TER of 0.05%.

Until cheap ESG ones become available in Swiss francs, I stick to a portfolio of a few proven ETFs per region : Cheap, accumulating, listed in Zurich and in Swiss francs, like XSPX.SW, XESC.SW, XMME.SW

@leman

WDESGC.SW is hedged, so not good.

LU2089238203 is not traded on the SIX or in CHF.

XNZW.SW has a TER of 0.19, but is still very very small 18 million AUM. It’s quite frequent that new ETFs have low TER and the provider increases it after. I

My point was that a focus on small variations of TER or characteristics can be misleading. What matters most is the performance. Here, the hedged WDESGC performs as well as the non-hedged V3AA, and even slightly better.

Same if we take an equal-weight tilt, for example with a multi-factor strategy, compared to the classic capital-weighted approach, that is by nature less diversified and concentrated on a handful of stocks.

Long story short: A focus on TER and the Vanguard “brand” is not always the best way to get good returns.

Sure, so we should have bought Bitcoin in 2015. Oh sorry, it is too late.

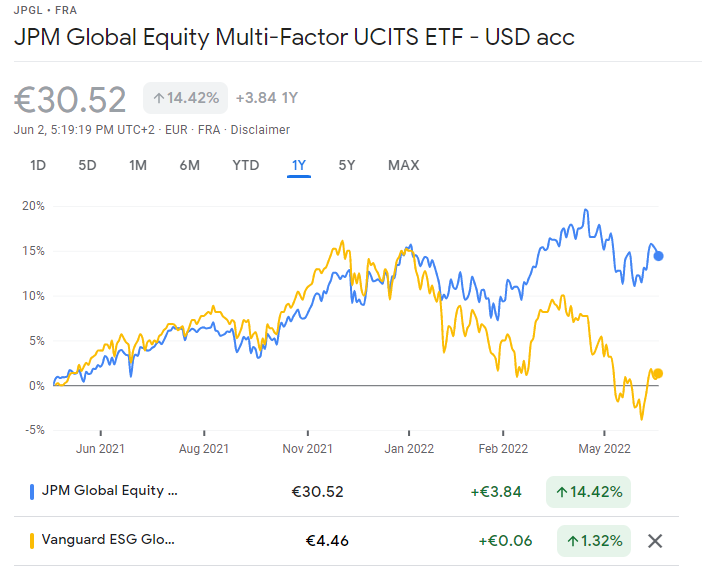

You compare two different baskets of stocks during one year. This comparison is totally useless. At some point I was comparing Credit Suisse CSIF Index Fund shares of the same index with and without hedging (eg. World ex CH ZB and ZBH), for many years. Hedged classes always sucked. I can try to pull and update these data, or you can also pick up this idea and do a comparison yourself.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.