Basically one can structure as many tranches of the loan as one wishes, between fixed and variable (SARON) interest rates.

The interest rates respectively varies depending of the duration of the loan.

Does anyone has any recommandations on the most suitable loan structure?

Really depends on your personal situation and your preferences.

But those rates are rather bad, especially the Saron. I work as a private client advisor and I can offer 2.80-2.90% for 5-10 years (as of today) and 0.60-0.75% margin for Saron (no duration).

P.s. This isn’t meant to be marketing for myself. Just to give you alternative rates that you should be able to get.

For the structure itself know that they will push you to have as many tranches with different durations as possible so that you are stuck with them for the long run without being able to escape. When the first renewal comes you will basically have to agree with their price since you won’t be able to negotiate anything.

@Pgl32

Besides that, regarding structure of the mortgage: As @HoiZame already pointed out, don’t go for different fixed-rate mortgages. It gives you literally zero room for negotiation once one mortgage runs out, because you are locked in till the last one runs out. You’ll have to accept any rate that they will offer you in the future.

My personal recommendation: If you want to play the safe card and have an exact budget, go for a single 10 year mortgage. Just keep in mind that long-term you’ll end up paying more interest than with Saron which has no fixed interest rate.

Saron gives you way more flexibility (you can always change it into a fixed-rate when the rates are better again, you can always switch banks etc.) and over longer periods of time (20-30 years) you’ll end up saving approx. 1%/year in interest. But you also have to be able to endure periods of higher interest rates like 2000-2002, 2007-2008 and 2023-2024.

There’s a bank (with French roots) in your area which is running currently an ad campaign with the following rates:

saron +0.6 %

10 years from 2.55%

15 years from 2.77%

If you are interested I can introduce you (just to clear I have no incentive in doing so, I just know some of the team since I worked on their IT migration project).

Wow, those are pretty awesome in todays environment.

@Pgl32

Just keep in mind the following when fixing long fixed-rate mortgages: The maximum duration should be also the time you plan on staying in the same place. If you fix a 15-year mortgage with 2.80% and want to sell the house 5 years later, it will still run for another 10 years. If the buyer doesn’t want to take over the existing mortgage (for example because interest rates are much lower again), you’ll be forced to cancel it prematurely if you don’t buy something else at the same time. The penalty in such a situation can be huge, as high as left duration x interest (10x 2.8% = 28% in this example, so 280k on a 1 million mortgage).

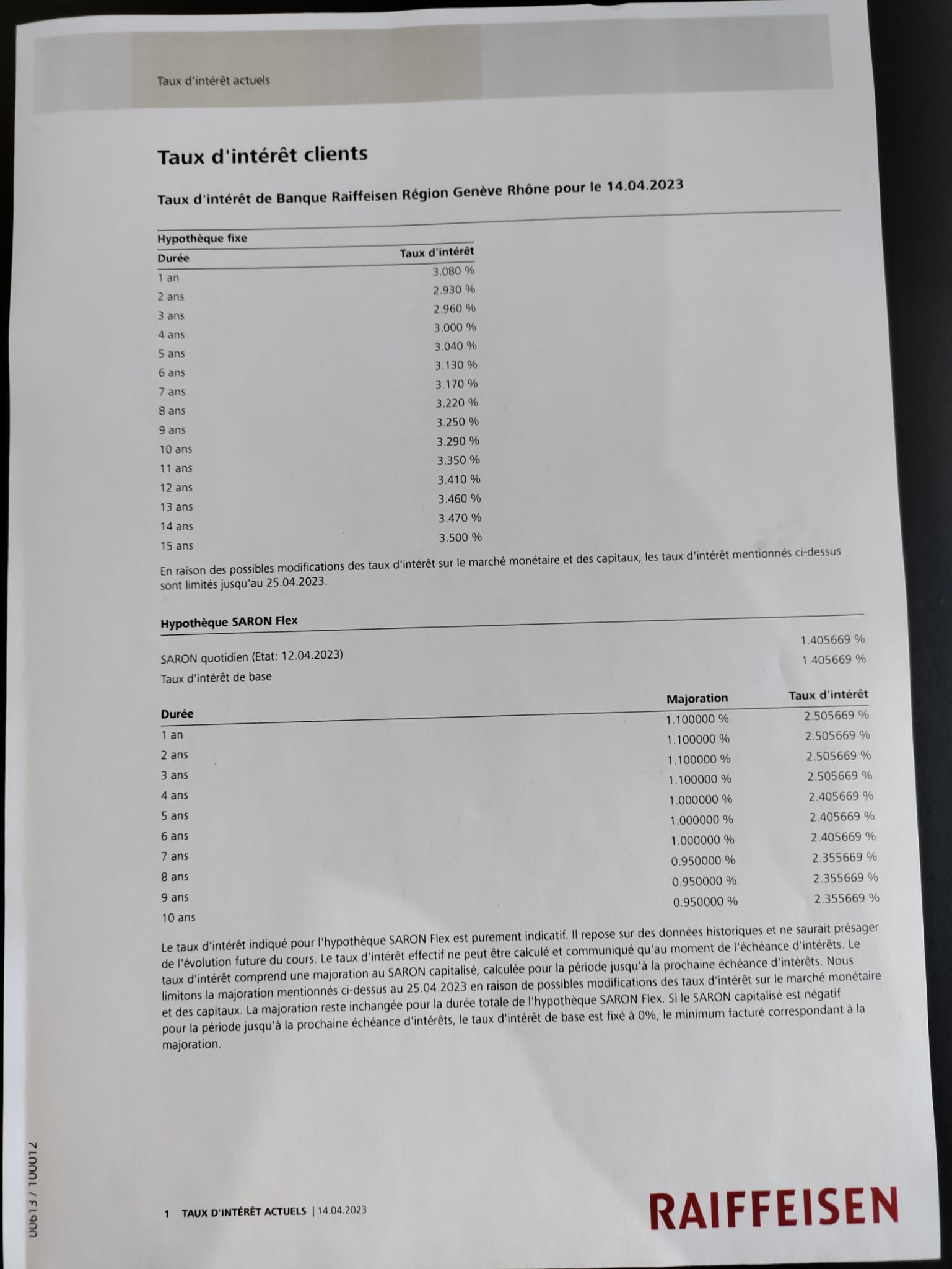

Thanks HoiZame, much appreciate your offer. The thing though is that the house we’re buying is on plan, and we have to sign a construction loan with the bank (Raiffeisen) that’s backing up the project. Hence we really don’t have much choice, but to go with this bank.

But your comments bring tremendous light as to which direction to take, and I’m tempted to go with Saron for 2-3 years and then get out of this bank, where conditions are obviously not competitive

I should have specified that we are buying the house on plan and have to take a construction loan with the bank that’s financing the project (Raiffeisen).

So given your insightful perspective on fixed rate vs Saron, the latter on a shorter term seems to be the wisest.

It’s a Genferei thing I guess, because I did not experience that when I was in Zürich…

Basically they’re forcing you to take the construction loan with that bank, but once it’s built, the loan becomes a hypothek, which theoretically you could then take with any other bank.

But because the bank is financing you for the interim interest during the construction, the trade-off is then that you remain with the bank after the construction loan is over.

You pay 20% when you sign a contract and pay the rest at delivery, in that case the promoter has himself to be financed by a bank (has to show proof of that), you do not need any mortgage until the delivery

You buy the land, resp. part of the land if there are other people in the project when you sign and you have to finance the construction based on the progress of the construction. As new invoices are issued your loan principal increases. But you are the one financing the construction not a bank, the bank has a contract with you, not with the promoter. The promoter just issues invoices that are then paid by the bank (in general the account is blocked) in your name. In that case there should not be any relationship between the bank and the promoter. The promoter has a contract with you and you have a contract with the bank. Of course The bank will verify things like solvency of the promoter and how serious they are and check any invoice that is received against the actual progress (send people on site, ask for photos, etc.).

Maybe they do not want to go through the solvency assessment with another bank but you should

definitely verify whether forcing you to take a specific bank is really legal, someone is surely making money at your expense in that scenario.

Sounds like good advice if you are stuck with this bank. After one year you shop for better rates again (Raiffeisen recently offered me 0.6% margin for a 5 years contract, 1% is quite a lot more).

Hey Paul

We have also signed our mortgage contract with Raiffeisen more than 6 years ago and are stuck for another 4 years. I wouldn’t do it again. They are more expensive than the competition and really complicated and old fashioned to negotiate with, especially if you want special conditions. Why not check out more options from nimbler and more digital providers like VIAC? If that’s not possible I’d go for a short contract and renegotiate after 1-2 years.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.