PS: I saw a 10y tranche priced at 1.18 last week, most probably a client with connections, 1.35 would be a good rate these days.

3 Likes

1.39 is ok but you can get better. I would target 1.35 at least.

1 Like

1 Like

Looks like rent reductions are near as well.

Hi Phil - I think BVK is similar to some of the bigger banks, they don’t seem to be very aggressive on the fix rates (they seem to be about 0.15 higher then what should be obtainable). As far as I can tell the fixed rates haven’t changed much in the last 1 week.

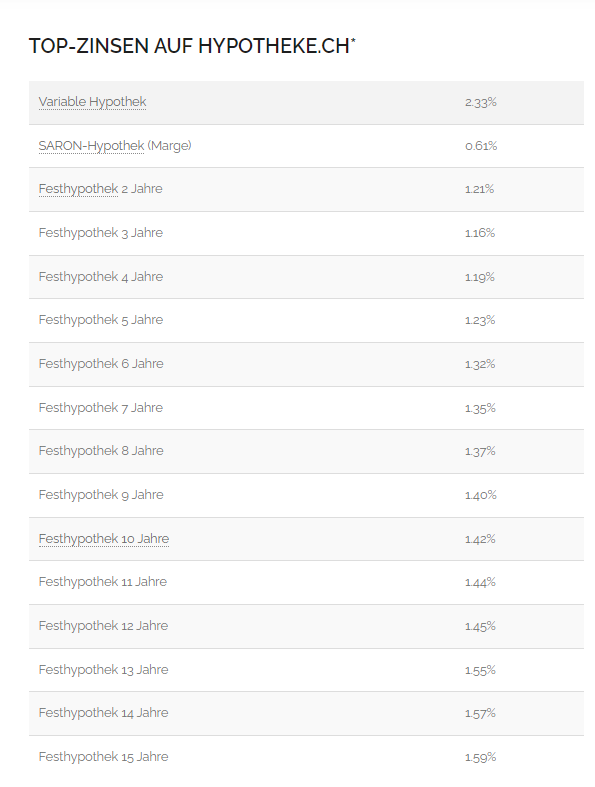

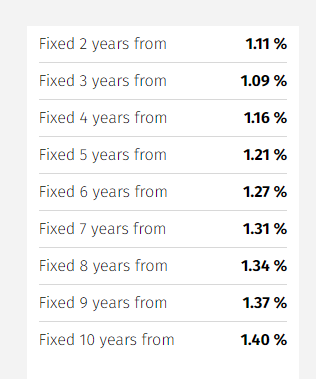

Normally I check on hypotheke.ch (10y = 1.42) and moneypark.ch (10y = 1.40) to see approximately what kind of 10 year rates are “possible”

… of course it depends on your situation, the home, and the financial institution if you would be eligible for that kind of rate.

1 Like

I’m currently on SARON for one of my properties. I think I will fix the rate on it. 1.4% is higher than I’d like but it is still a decent rate.

I agree. Hard to have a financial seppuku with a 1.4 rate; may be worth it for peace of mind. If I was offered that today I would bite (at least on a tranche).

I will wait longer as I have some fixed at 1.0 and some SARON (which is expected to drop soon), and I’m certain I can’t get the 1.40 while we are still “locked” with a fixed tranche.

I have to either:

- “eat” their fat margin padding on the fixed rates today which I don’t want to do because I also lose the ability to amortize via SARON (and the whole world is in dove-ish mode).

- wait another year to go open market on fixed rates (and decide then if it’s worth it vs keeping SARON)… which for the moment is what I’m expecting to do.

0% SARON again in 12-18 months is my bet.

Eurozone and US are crawling under debts payment and can’t keep rates high. Inflation will repay their debt.

On the other hand SNB will have no other choices than switching to “repression mode” to fight further CHF appreciation.

In this scenario cash is trash, Rental properies and equities with leverage are the winnings horse.

4 Likes

I wouldn’t be surprised given Martin Schlegel’s comments at the last SNB news conference.

I’ll def be listening to the next one on Dec 12.

What I like about fixed rates is that I can pile the surplus savings into the market with a known cost, so I hope those come down even if it’s just a bit more from here.

1 Like

I agree with you on this, but I wonder if SNB will try to keep rates high to fight inflation. They were one of the first in the western world to raise. Then again, maybe there won’t be any inflation if there is a downturn/recession.

They’re currently a lot more worried about deflation I think.

2 Likes

Yes for medium terms you are totally right. Deflation is their concern

Anyway we have no idea if a bigger second inflation wave comes again in 2026 or 2027. Probabilities are far from 0

1 Like

If the probably was very high wouldn’t we see that reflected in e.g. 5y or 10y mortgage? Or in the long duration SNB rate?

Just my opinion - personally I don’t see the 2nd wave of inflation coming any time soon. Pretty sure this wave was caused from all the money printing / covid stimulus worldwide, which is why it is already subsiding.

Fixed today with existing bank for 1.5%. Decided it wasn’t worth the hassle of switching provider for 0.1%

3 Likes

If you plan to stay at your place in the next 10y you probably made a wise decision.

We’re not in this case and still young with good abilities to take risks so we’ll carry on with SARON. One more year to wait to have it again cheaper than fixed (normally!!)

It’s actually a rental. I was going to sell it but the sale fell through. Otherwise, I would have fixed at 1% at the time!

1.5% for fixing how many years if I may ask?

10 years.

1 Like