As evidenced by your posts, one can hold both of these thoughts at the same time in the same brain.

Eventually, the thrill of dividend income will infect the rest of your brain, though … it’s unavoidable … just wait, sheer lunacy is waiting for you just around the corner.

You caught me there.

I would like to add that I hold a grand total of less than 0.1 % of my asset value in CHDVD and have it in my Yuh account for the explicit purpose of getting the joy of seeing a few CHF appear in my CHF history. My monkey brain is satisfied. Judge for yourself if this is comparable.

My brash statement is based on the fact that you have triggered me. I have fallen into these traps a few times already.

I take issue with calling such a gamble something cute like “monkey brain”. It might lead to people having less experience in the stock market get in on this and find it harmless fun.

There is a very significant chance that you won’t see your money again.

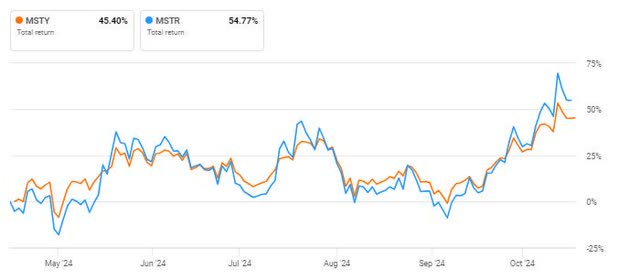

Returns of this size (taking MSTY as an example) can come from four sources:

Leverage: Chance of being wiped out: very high. It’s a ticking time bomb. Like MSTY.

Trashy assets: High risk, low reward, like high-yield bonds or Argentine sovereign bonds

Depleting capital to prop up the yield: See my roof-chimney analogy

Ponzi scheme: Robbing Peter to pay Paul (see Madoff)

None of these sources are sustainable in the long run.

I don’t disagree, I neither have nor plan to have any of the yieldmax stuff, I think if you go back to my posts on this thread you’ll see, I hope to be fairly balanced on it.

The5z has it and also published how many.

I wonder if that ETF with 182% dividend yield means that he should only pray for a bit more than half a year that it doesn’t go to 0 and after that it is free money…

I’ll agree with our colleague above, I don’t understand or like these, and think they are indeed very dangerous for anyone who doesn’t understand the risks and has no patience.

On the other hand, who knows, the overarching feeling I have of these “modern” products is that they are sort of “traders for hire”, they are not investments. People do make money trading so perhaps these products offer a service of sorts, participating in risky leveraged trading for a small fee, without being a trader yourself. It’s scalable as the trader (the fund manager) just executes an algorithmic process, it circumvents the risks of options for the individuals buying these products (because their account can go to zero, but not minus). They will have a place, I feel, I just don’t call them investing.

Anyway, don’t understand how they work and won’t have them, probably many will be burnt by these given they are shilled by social media idiots. I feel we here are neither the target audience or at risk.

In defense of “high dividend” and “high yield strategy” ETFs.

US ETFs are designed for US residents, not for you, %USERNAME%. As it was pointed out many times, taxation is an integral part of personal finances and its optimization should be an integral part of the investment strategy. Taxes work differently in US and in Switzerland, so what looks like a total nonsense for a Swiss portfolio, might make a lot of sense for a US one.

US has capital gains tax, but qualified dividends, which seems to be most dividends, have some preferential tax treatment. This alone could be a reason enough to focus on dividend yield instead of selling the securities. The highest pure dividends yield (no derivatives) that I have seen in an ETF on US stocks market was around 4%, in a superconcentrated ETF on high dividend stocks that hardly grow in 10 years or so.

Covered calls strategy can be seen as a way to convert some capital gains into an immediate income. I am not sure how taxation of these gains in US works, but at least I guess that these gains are accumulated short term, and you don’t have to tax gains accumulated in a 10 year long bull market.

I was playing with a scenario of constructing a high yield portfolio on US stocks using a combination of normal total market ETF(s) and covered calls ETF(s) on SP500. The dividend yield can be easily boosted to 4-5% without losing much of diversification (but losing on the upside participation). To me it looks like a better deal than a concentrated high dividend portfolio. Nevertheless, I don’t need it and I haven’t implemented it.

However I totally agree that a high yield strategy using all kinds of junk as collateral is not a sound strategy. It might work and it will be fun, but not more.

TBH instead of those ETFs, I’d prefer a “wizard” interface on IBKR, where you pick your Stock (or ETF), insert the values and then have your whatever strategy with options I think something similar exist on robinhood, but just for the simplest ones.

If someone want to implement the iron butterfly* , it would be possible to do with it. Those ETF are for the lazy and maybe too obscure.

Thanks, after I wrote this I walked my dog and was mulling it over a bit more. I remembered this post, using a strategy even my options-naive brain can understand. Of course the underlying stocks make a huge difference, slow and steady growth stocks should generate far lower premia (and losses) than highly volatile ones, so maybe the difference in yields achieved by our colleague could be fully explained by that (I didn’t look at what stocks they’re applying the strategy to, just hypothesizing).

The next thought was that to get these yields that the yieldmax funds are getting there has to be either big risk, or even bigger opportunity cost (Microstrategy is +272% YTD, the fund’s yield is claimed to be 190%, and YTD appreciation is ~6.6% so there’s a 75% opportunity cost right there). One can argue, I’d fall into that camp myself, that selling can be stressful, so consciously settling for lower returns not requiring selling is a viable and respectable approach.

I’d surely hope there is regulatory oversight and it’s not a Ponzi, but indeed as referenced in this thread Madoff fooled many rich and powerful so what chance do small time impressionable get-rich-quick chasers have to survive?

This sounds like a good idea - though I can’t stand the “robinhood” name - but it’d need to be caveated by several walls of text and big red letter warnings about getting ones account blown up, and being in the wrong side of a debt collection agency. Of course people will promptly click “Agree” and ignore because 0ptionDud3 told them how they’ll become millionaires in three clicks on TikTok.

It’s where you draw the line, though, isn’t it? These strategies appear fairly safe but I haven’t spent serious time to understand them, or even dreamt of trying to apply them in practice. Any sort of naked option shouldn’t be allowed, and the cash requirements for puts should also be very strict, in my opinion, to prevent people from being on Jimmy Burke’s hit list.

Edit: personally I’m both chicken and simple, I’d use cash-secured puts to get things I want, that’s all

Ever after all the comments, I still don’t know what is the problem we are trying to solve right now

As far as I know , most people here are not actually retired or FIREd yet. So any high dividend strategy for Swiss investors is counter productive for time being until they actually need to consume the dividends for expenses. Do we agree with it?

If yes, then is the discussion focussed on future options to consider when one actually needs the income?

If no, then can someone explain to me under which circumstances a high dividend yield strategy is better for CH investor (still employed) vs. a normal MSCI ACWI strategy (approx 1.7-2% dividend yield) ?

Assumption -: total returns from all strategies is same as long as we are talking about well diversified funds focussed on global exposure. Because let’s face it no one beats the market in long run

When a high yield strategy leads to someone irrational and highly skeptical of the stock market staying invested instead of high-tailing it out of here and putting all their money under their mattress?

I would first say that this topic – at least for me – has the vibes of mainly being a fun one. It even contains “monkey-brain” in the topic title …

It’s thus perhaps a little maximalistically absolutist* to implicitly be asking for a problem to be solved?

Or maybe your comment was second level thinking, aka meant in an ironic way: we’re just having fun here, not trying to solve a problem, and you are just re-stating the obvious?

Yes, the tone of the thread is mostly to have fun. But… it’s also true that I (and others) own dividend ETFs. Sometimes because people are near FIRE-d (not me), sometimes because they like to see dividends (me). It’s of course irrational or so someone said, but like @assemblyrequired and @Abs_max clearly said, if this sub-optimal (better definition than irrational imho) is going to help people stay invested, then this thread is officially also a thread to help people stay invested and sleep well. If my monkey-brain helped at least one person to invest in any level of optimal way, then I’m happy.

Having said that, I’m still waiting for a message @THE5Z and his epic* portfolio.

* Epic in a not-so-serious way (imho)

(omg I’m starting to star stuff like Your_Full_Name )

side note: I am also not a fan of changing my portfolio near retirement. It seems that some people are using Acc ETF and switch to Dist just before retirement. That sounds scary.

Actually I didn’t realise it was only for fun. I thought we were trying to come up with suggestions for high dividend (yield & frequency) and I was not sure what was the driver for this.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.