I think of buying 10k of stock XYZ and using 5k of my own cash + 5k from IB.

Now my question:

How does this actually work?

Can I simply have 5k in cash and the buy 100 stocks of XYZ at 100 USD stock price (total 10k)?

Or would it also work to buy 100 additional shares of XYZ to 100 shares of XYZ that I already have in my portfolio?

Will the margin that I can have be calculated on my current portfolio s net liquidation value or on the cash I hold at the moment I want to establish the position with the loan?

I saw there are 2 models on IB:

risk based and rule based.

I guess for standard margin trading the rule based system applies?

And where can I see if I have an account that allows margin trading or not?

It is calculated with the margin requirements of assets you own and assets you want to buy. But when you buy, the initial margin requirement is the relevant one and not the maintenance margin requirement.

If you like a long answer, I’d recommend reading Jason Zweig’s book *The Little Book of Safe Money", especially on leverage.

For a shorter answer, Jason Zweig has a WSJ article on “Borrowing Against Yourself”. It’s behind the Journal’s paywall – I found the two paragraphs best for summaring the content:

When you use margin, you merely appear to be borrowing from yourself. Instead, you are borrowing from one of the most unstable and unreliable lenders imaginable: Mr. Market, that personification of investors everywhere, sometimes euphoric, sometimes miserable, never predictable.

If Mr. Market trashes your investments in a sudden panic, your margin debts may be “called,” forcing you to sell some of your assets to sustain the minimum account values you committed to under the terms of the loan. By definition, margin calls are most likely to come just as the prices of the holdings you borrowed against are in free-fall.

For a more recent reference point, I’d mention the most recent market crash and margin calls that even caused portfolio holders to have to sell so-called safe securities to avoid selling their risky assets at the worst time possible.

Nevertheless, it will not harm you to “study” how the mechanism work without putting real money on the table…

Start with the IB guide and be sure you fully understand it. Run some simulation with a spreadsheet in order to “play” with real numbers…

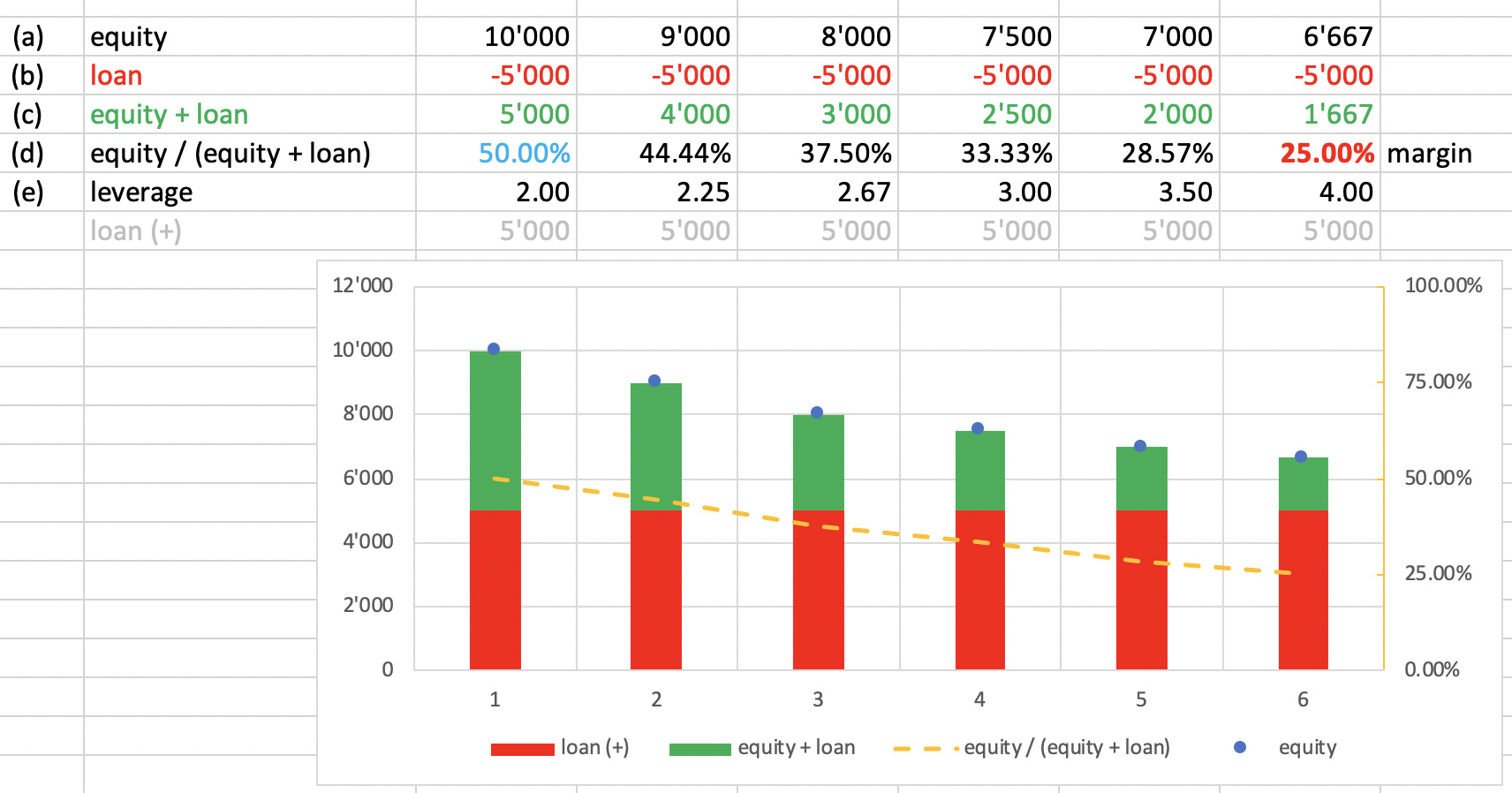

Start analyzing RegT margin, whose requirements are fix and easier to understand (initial margin 50%, maintenance margin 25%)

Both your examples should work as the ratio between ‘equity’ and ‘equity + loan’ in order to buy should be >= 50% (where ‘equity’ is the total value of shares held and ‘equity + loan’ what “your belongings” are worth…)

Below a possible evolution of the situation until the triggering of a margin call

“In order to finish first, you must first finish” - someone clever

Leverage should be used sporadically with the intent to cover the debt relatively soon. Not as a long term deal because the risk of margin call becomes too great.

My advice: don’t put your portfolio at risk of a margin call (forced selling). Using a little bit of leverage (maybe 10-20%) for a short period of time is fine in my opinion (up to 1-2 years), because you might want to take advantage of some opportunities (for instance, during the March panic). But even when you’re conservative, there is the risk that you get addicted to essentially free money and increase your leverage more and more. Then a crash occurs and you’re in a really bad position and worst of all, you can’t buy at these distressed prices because you have to make up for the debt.

For what it’s worth: my leverage ration is about 1.08 at the moment. I took advantage of the March panic by buying more stocks than my savings allowed. But I am reducing my margin every month and in December it will be completely gone. I would never use leverage to regularly (every month) buy stocks at regular prices and keep my leverage ratio constant.

Margin loan is as any other loan. Never take one if you cannot pay it back easily and safely.

With interest rates at 0%, it is obviously very tempting. Just keep in mind that when the rates go up, the stocks go down. A potential financial catastrophe may be around the corner.

I’m not afraid to admit it, I’m on margin. I went as far as 1.7 in March. Now is about time to go back to 1.0.

Hi @cyberhigh in my humble opinion the answers have been quite patronising. Of course, you should read, learn and know what you are doing before starting. After you make sure of that, it is my suggestion you try it out. 5k is not the world after all and if you take a hit I’m sure you can recover.

Let us know how it goes with IB as I have the same intentions as you in the future.

This is interesting. Do you have any preference for the stock outlook (bullish/bearish) or is it all the same to you? I’d also be interested in what your profit % from the ITM calls would typically be. Obviously the premium has to be fat enough to cover the difference between the strike price and the current share price - but how fat exactly

It let us understand that he can borrow up to 50% of it’s capital before his positions are sold and so he uses only 25%.

I’m actually in a very similar case as my margin is called at 25% so I use only 12.5% max and I have cash on “non leveraged positions” in other portfolios + emerengy funds I could use in case …

Anyways my question is why does IBKR only let me use 25% of margin and not 50% ? Did something changed in some regulations ? Do I not have enough capital to get 50% ? Is there an option to activate I am not aware of ?

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.