I moved to Switzerland earlier this year and have accumulated around CHF 40000, which is currently just sitting in my bank account. I recently started investing in ETFs by purchasing a fixed amount of shares each month, but I don’t feel comfortable investing the entire amount (or a big chunk of it) at once.

I’m currently with Yuh, but their savings account offers 0% interest, which isn’t ideal.

What do you usually do with your “idle” cash? Are there any Swiss banks or platforms that offer a guaranteed 1–2% return (something similar to Trade Republic)? Or do you prefer to buy bonds or other low-risk instruments instead?

Assuming you got paid 10 times, that’s about 4k of savings each month.

I guess you could keep it as cash for an emergency fund.

Though if you don’t want it to grow bigger, you should start investing at least 4k per month to keep at the same level (or whatever your savings rate is).

You could invest in a fund like CHDVD which invests in Swiss companies and pays dividends.

Swiss national bank has the interest at 0%. So outside some special temporary offers, you‘ll not get more. Europe‘s ECB has the interest rate at 2% currently, that‘s why TR is able to offer 2%.

The CHF however is also expected to apreciate compared to €, at about that interest rate differential. (Interest rate parity theory).

Only things giving a little interest are term deposits at banks. But you need to lock you money away for a fixed term. So i.e. 1 year gives 0.3% interest currently.

For anything more you need to take on some amount of risk.

For temporary stuff, for short-term small but non-zero returns might also consider prepaying health insurance, or pre- and overpaying taxes.

Conditions vary, but you might get some 1% discount, respectively interest..

In Zurich you get 1% on pre-paid taxes, on a federal level you get 0.75% the last time I checked.

That’s about as risk-free as it gets IMO (aside from government bonds).

Demanding higher returns will require you to take higher risks.

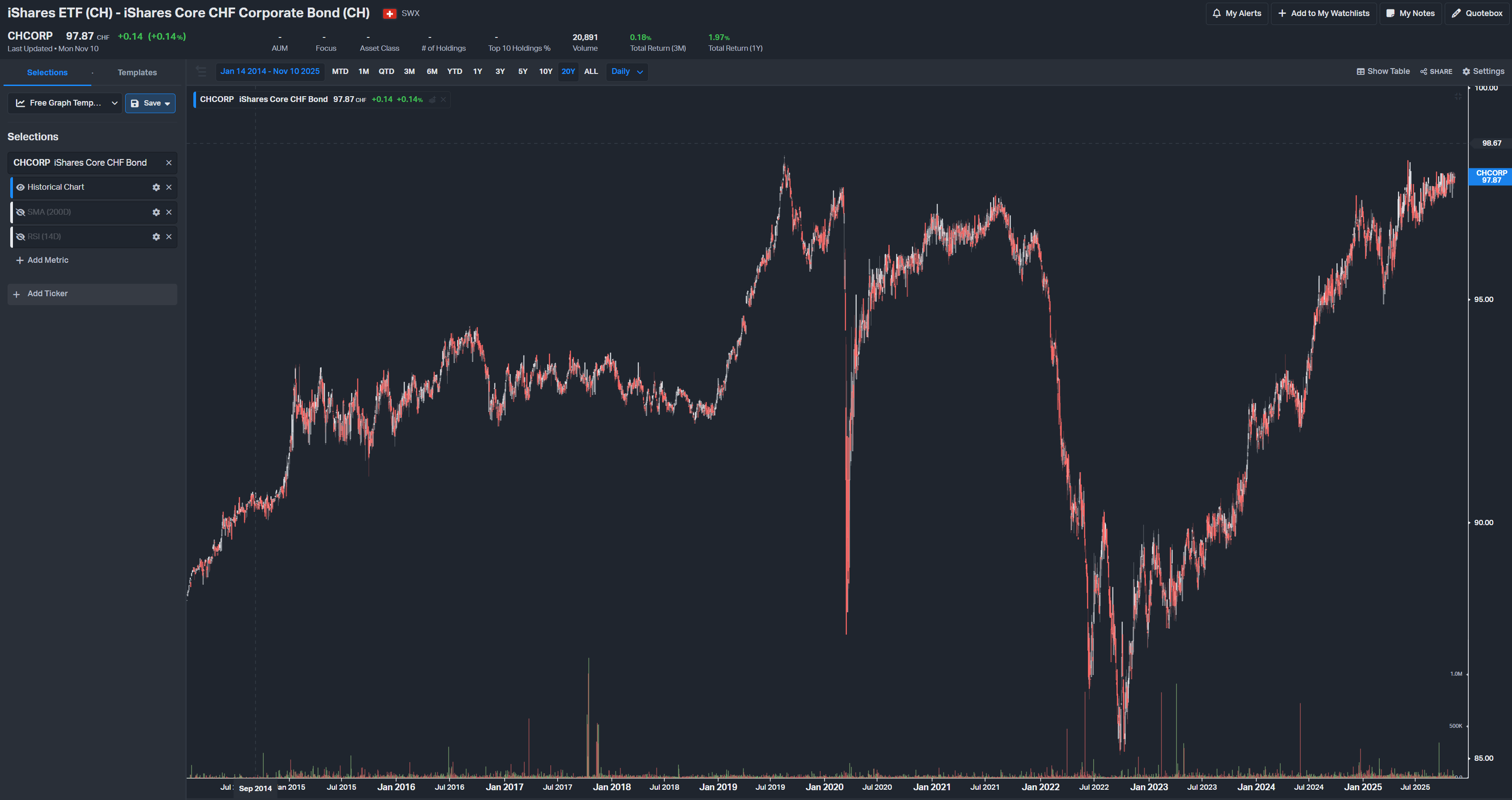

Even investment grade Swiss corporate bonds fluctuate quite a bit …

… and if you trade the ETF on a Swiss broker, they’ll probably take a nice cut via fees, too.

Discussed elsewhere on this forum in multiple corners: using backtesting it’s best to lump sum. That said, I couldn’t bring myself to lump sum, either. The psychological damage of a market drop after my lump sum investment would seriously mess with me …

Or use this weird mental trick: since you just moved into Switzerland, maybe think of your cash pile in terms of your home country’s currency. I bet the equivalent of your CHFs accumulated have grown considerably in your home country’s currency.

Edit:

You didn’t say what ETFs you invest in. If you invested into, say, VOO or some other large US exposure ETF denominated in USD, you could of course convert your CHF into USD and park your USD cash by buying US treasuries, currently yielding about 3.8% or so.

Of course, you’re not necessarily getting a higher return (in CHF) as now you are taking FX risk.

I see. I guess at that point bonds would be more appealing, although there could be some level or risk involved.

This is true, I hadn’t considered that. Good advice.

Yes, I am aware that a lump sum is a better strategy than dollar-cost averaging. However, as you mentioned, it is mentally harder, and I probably would not be brave enough to do it, also given the little experience I have in investing.

I invest in VWCE/VWRA. I would prefer to avoid non-UCITS ETF to avoid issues with taxes

Thanks a lot for the detailed explanation! I’m still a beginner at this and therefore do not fully comprehend your strategy yet, but this is all on me. I will look better into this in the near future, since it is not fun to have a lot of idle cash sitting in a bank account.

Whilst we can’t know the future with certainty, we have some history and some logic to make an educated guess. Selling options insures the tail risk of others. Anecdotes (“works for me”) are particularly ill-suited to understand such instruments and the actual expected return.

Also, most cash secured puts strategies are not tax free in Switzerland. The cash part has taxable interest. Securing USD contracts with 0%-interest CHF is an optimization with its own additional risks.

Learning is good. Please make sure you always understand well what you invest in. Those other users didn’t dogpile on “cash secured puts” because they want to maliciously keep you from arcane knowledge to get rich quick. Quite the opposite, actually.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.