Hi,

I have my current “lazy” portfolio made of 50/50 IWDA(MSCI world) and DBZB (global Bond edged ).

For some reason I always converted the CHF I earn from my salary in EUR to buy the above mentioned funds but I thought it could be more efficient to find similar funds in CHF since the EUR is losing value big time compared to CHF in the long term.

Do you have something similar to suggest in CHF? Does it make sense considering that I might leave CH in 6/12 months(at least)? Not sure I am forced to sell those when moving back to europe.

I don’t know what/where to search to find such information. The broker I use is Interactive brokers

Thanks

EDIT: spoiler conclusion: no it is not worth.

For an unhedged MSCI World ETF such as IWDA, the fund or trading currency doesn’t matter, with the exception of currency exchange fees (but they are very low at IBKR as long as you don’t convert tiny amounts). I.e. there is no real reason to change your equity ETF.

For a hedged (bond) fund, the currency can make a significant difference, though.

If your future expenses will be in CHF, the EUR-hedged bond fund seems like a bad idea. The CHF-hedged IGLC (iShares Global Govt Bond) may be similar to DBZB. Alternatives are AGGS (iShares Global Aggregate Bond) or VAGX (Vanguard Global Aggregate Bond), which also hold non-gov bonds. You could also invest part of your bond allocation into a CHF bond fund (SBI index) to reduce hedging costs.

On the other hand, if you’ll definitely move back to the EU before you actually need this money and thus, your future expenses will be in EUR, it probably makes sense to keep the EUR-hedged DBZB.

If you don’t know yet whether you’ll stay in Switzerland or move back to the EU, it’s less clear what fund makes more sense. You could split your bond allocation into a CHF-hedged and a EUR-hedged part. Or into a Eurozone bond fund and a CHF bond fund (SBI). Or even invest into an unhedged global bond fund.

I don’t see why you would be forced to sell CHF funds when moving to the EU. However, if you move to the EU permanently, CHF is likely no longer relevant to you, so you probably don’t want to hold any CHF-hedged funds anymore.

Blockquote

For an unhedged MSCI World ETF such as IWDA, the fund or trading currency doesn’t matter, with the exception of currency exchange fees (but they are very low at IBKR as long as you don’t convert tiny amounts). I.e. there is no real reason to change your equity ETF.

Why the currency does not matter? If I could invest in IWDA(CHF) then when it is time to covert the value to EUR when I reach the retirement age , I would have an additional gain coming from the currency exchange.

Euro currency lost 20% of its value in the last 5 years compared to CHF

I think I got the point. I will try to reformulate it in my own words (hopefully understandable in english language ) and with my lack of technical knowledge.

My understanding is that the ETF will use the purchased quotes in CHF to buy an underlying pool of currencies/stocks , then when I have to sell those quotes (supposedly ,after a long time) , the pool of currencies will be converted to a very strong CHF (stronger than EURO)

When I do the operation with the ETF in EURO then I initially buy a smaller (compared to CHF) number of underlying quotes/currencies but when it is time to sell those, the EURO currency will be cheaper to buy than CHF…so that makes the operation equivalent (or sort of equivalent…as far as they say)

I hope that make sense. It would be good if someone can confirm.

will always be the respective foreign currency exchange rate between the given currencies.

If you buy the same ETF, you’re buying the same “thing” underlying basket of securities.

You’ll invest in the very same companies at the very same composition (percentages).

Imagine buying an small bar of gold at its current price of CHF 1731/fine ounce.

You then drive a few kilometres to France or take a quick plane ride over to Canada.

What do your fine ounce of gold is worth there?

When you convert your CHF into EUR and then buy securities, you’ll buy the very same amount of underlying shares (save for transaction costs, i.e. the tiny cost of currency conversion and different commission rates/pricing in different brokers or at different stock exchanges).

Thanks for your comment.

I can’t still get my head around that.

I thought that ETF shares purchased in CHF instead of euros, being CHF a stronger currency against the pool of stocks/currencies within the ETF, would allow to buy more shares.

I will google for an example showing some calculations because I am curious to understand this.

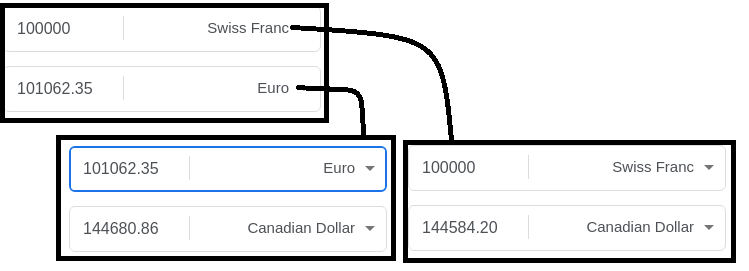

Actually it turns out that I buy a bit more more CAD with EUR for some reason, starting from CHF. I was expecting a much different result between the exchange EUR-CAD and CHF-CAD. So if the underlying ETF shares are in CAD, this proves the amount of CAD purchased is quite similar.

That’s interesting. I thought all the currencies exchanges values were independent each other.

Let‘s assume 1 CHF is 1 EUR and will be worth 1.20 EUR in 10 years. So the CHF will strenghten another 20%. You can buy gold for 40‘000 CHF/EUR per kg. 10 years later you can sell the gold for CHF 60‘000. With that money you can get EUR 72‘000. So you could also sell the gold for EUR 72‘000 and then convert it to CHF 60‘000.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.