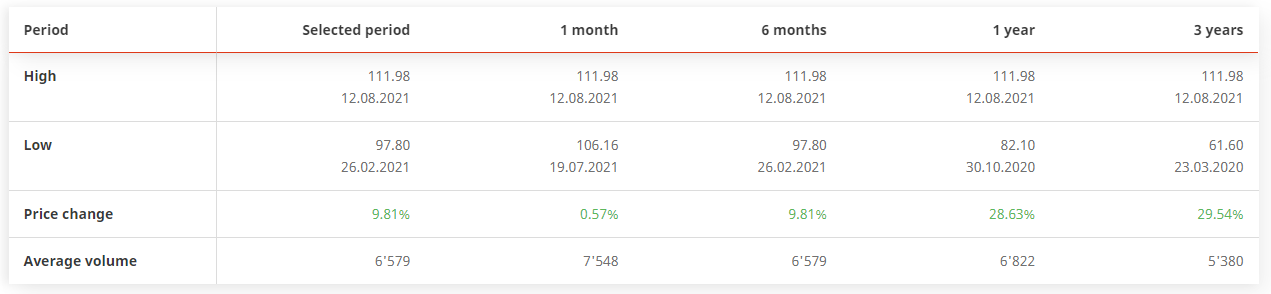

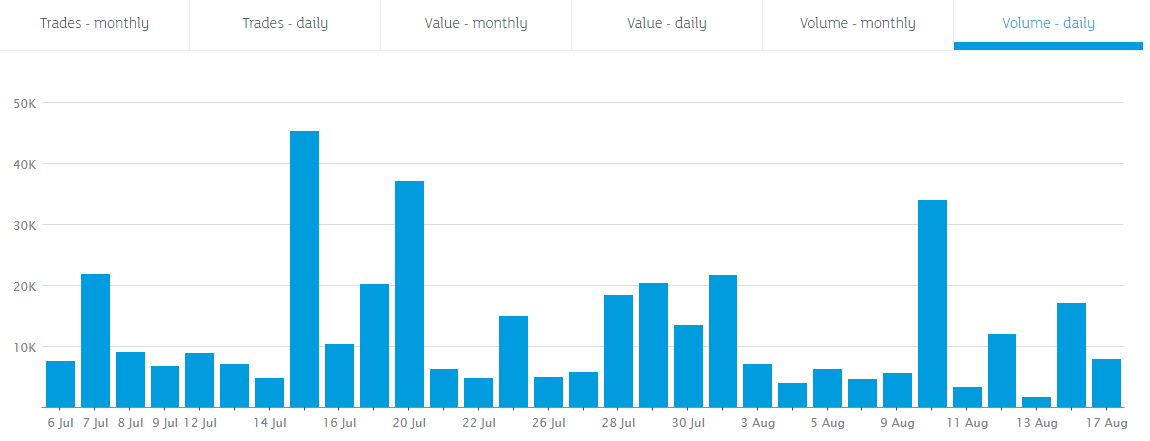

According to SIX, the average daily volume is around 7’000 shares. That’s some CHF 700’000 in one day. I guess you would have trouble to fill such a large order in one day. Interesting point.

Would anyone have a suggestion? Is there an Ireland-based (or simply, ECITS) ETF with enough volume to handle a trade of CHF 500’000 without getting heavily hit by spread?

A low volume does not necessarily mean that it is impossible to trade large chunks, especially in the case of ETFs. There are usually market makers waiting to buy/sell under-/overpriced shares of an ETF. Maybe you would lose a bit of money (0.5 %?). But it would certainly possible.

Then look into trading algorithms. IB Pro has order types that support you with trickling a large junk of securities into a market while trying to preserve a good price (Order Types and Algos | Interactive Brokers LLC).

Buying on most liquid instrument on most liquid market is good thinking on your part. You might have to do the trickling manually and pay separately for each trade. Unless you go to the pros (i.e. established brokers) and pay them a fee to do it for you

IIRC in one of the Fundsmith ASMs Terry Smith says that they consider their positions to be liquid / no real lump sum risk if their position is up to 10% of the average daily volume. So I’d not really think about moving up to 700 shares per day, even if market makers don’t do too much.

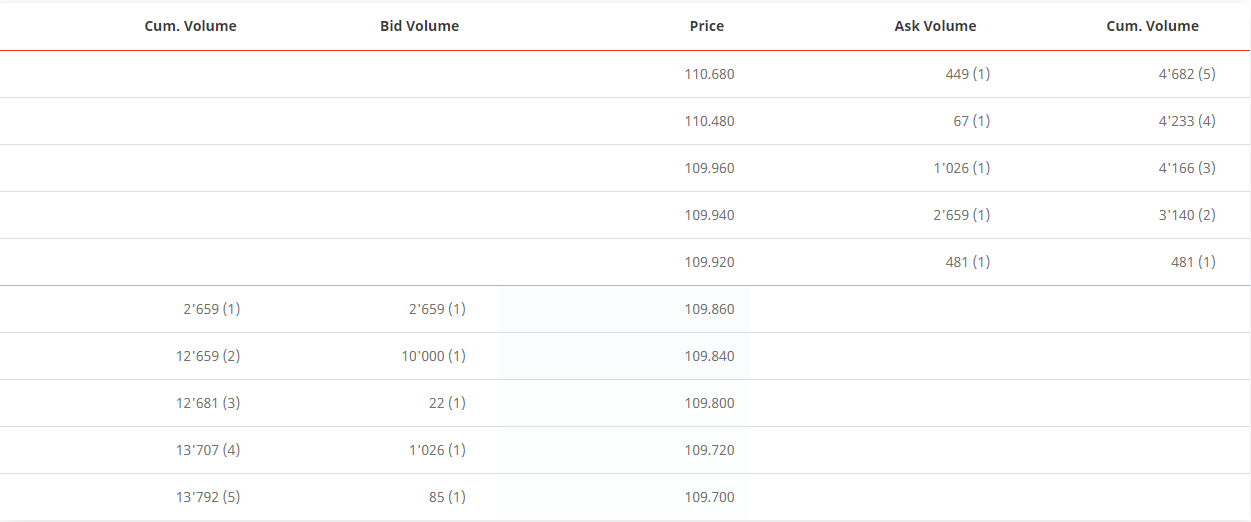

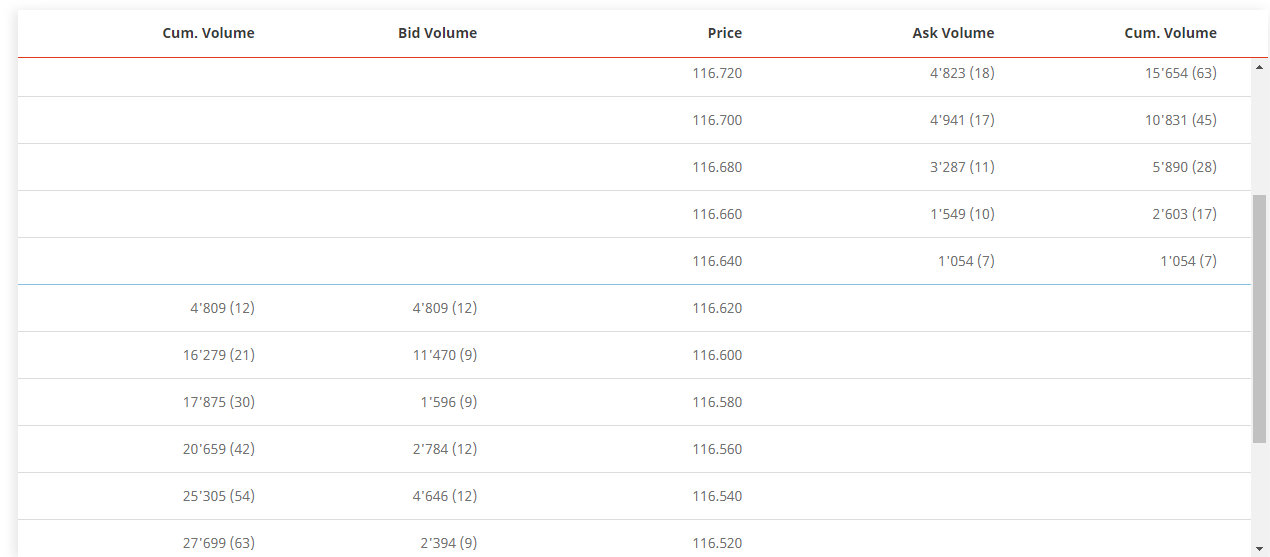

One thing I don’t get. If you would like to sell 50’000 shares, then we can see that the current orderbook does not show you how deep down with the price you’d have to go if you went with whatever the market is offering (cumulative offer of 13’792 shares).

So instead you could place a limit order, for example at CHF 109.86. Then you would await the market maker, who could step in, or not. In the meantime, let’s say the real NAV goes up by 1%, at which point your order gets filled. You just suffered a 1% loss, because you could have sold 1% higher. Or am I missing something?

But you are obviously at the mercy of the market makers. If they suddenly step away or lower their prices because they think everyone is cashing out and going long boats then you may not get the price you expect.

If you do not want to run the risk of having an open bid then you can buy the shares that are being offered and await more shares being offered before placing another bid. But who is to say that the real NAV does not drop 1% while you play this game.

If you know you have a high risk of impacting the price with a large sell block (which, realistically, is a possibility with the scenario), you can try the Arrival Price Algo.

This order type will attempt to get the mid-point of bid-ask spread at the time of the order for the full sell order (however, its execution speed is very much not guaranteed).

If you were trading a US product, you could have tried to use a Fill or Kill order, in which case, in the theorical situation, either the market maker’s apetite is enough to buy your full order, or the order is immediately rejected.

Welp, that’s quite disappointing how limited their order types are, they don’t appear to have FOK orders (And Arrival Price algo are indeed a IB specific order).

On ETF on liquid underlyings there is no problem to trade large volume. Don’t look at daily volume, it is meaningless. You’re not going to trade against someone else buying but with market maker.

Just put a large limit order at current bid and market makers will be happy to take the spread.

ETF volume is meaningless. You need to look at basket volume and it’s going to be big on your etf.

Only problem might be if you have etf on Iranian small cap and you’re trading it on a day when there’s bank holiday in Iran etc.

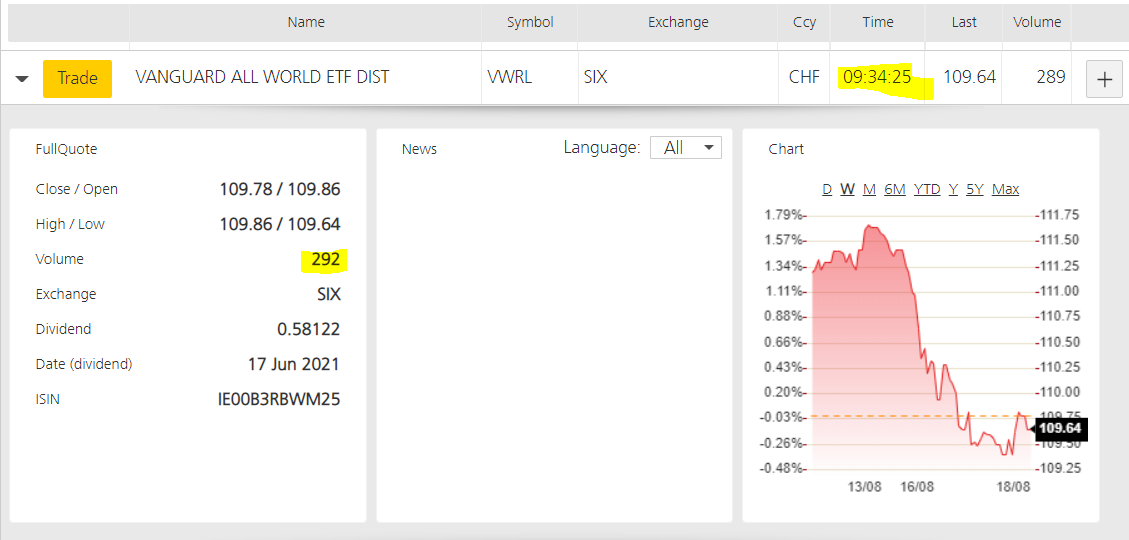

You find a lot of information about VUSA on the website of the swiss stock exchange.

Liquidity and spread is not always the key issue. One important issue is the currency used for the trading of the ETF. If you have to change currency trading it could end more expensive than the trading itself with some brokers.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.