How can I replicate the following portfolios with VIAC? I have 5 portfolios there, all have the same strategy and I have lost track of the funds offered (CS/Swisscanto).

a) Golden Butterfly

b) All-Weather Portfolio (Ray Dalio)

c) Harry Browne permanent-portfolio

You can’t replicate the Golden Butterfly or Harry Browne’s Permanent Portfolio because your gold allocation is capped at 15% in VIAC with either 10% of the Swisscanto/CSIF gold fund and 5% of the other.

You should be able to replicate the All-Weather now that there is a commodities fund. Be aware that it is mainly a bond-heavy portfolio and even Ray Dalio has been saying that bonds are trash came 2022 (so it was an “all-weather” except for those weathers where bonds don’t do good enough). Also, there’s no guarantee that a 1:1 conversion toward CHF assets, in particular bonds, would allow the porftolio to keep the properties you are searching in it, even though it was what I was considering doing when I was toying with the idea.

When I was considering it, I had arbitratily decided that real estate could roughly be considered as having a 50% gold and 50% stocks behavior, so I would have used it to artificially increase the “gold” allocation. There’s no litterature supporting that assumption of mine that I am aware of, which is to say said assumption rests on nothing.

In short, VIAC isn’t the right tool to do what you are trying to do. Others would recommand Finpension; my alternative would be to consider your whole porftolio as a single entity and hold more gold outside of the 3a, which would bring your target allocation where you want it to be.

Edit: to note that you also lack actual long term bond funds, which, when they are mixed with short term ones, can be replaced with an appropriate amount of medium term ones.

Are you expecting people here to do the work for you? It’s not that hard, but if you’re not able to find funds for small caps, short and long term bonds or gold by yourself from these pretty limited pools of funds at VIAC/finpension, you should probably just stick to pre-made strategies.

Why did you narrow it down to those three portfolios? In what ways do you think are they appropriate for your investment goals?

When asking my question I was hoping that someone used these lazy portfolios at VIAC. In addition I

think VIAC is a awful in describing their 13 bond and cash offerings and their differences.

In my main account i hate bonds, but why not take advantage of 3a tax breaks and automatic re-balancing?

my goal is to replicate VT, MSCI world or something similar within saving apps such as finpension/ viac / findependent.

Please find my approach below, what do you think? How would you do it differently?

1 Findependent (non-P2/3a money)

This one is easy, as they offer VWRL (link) with max weight 100%

2 Finpension (P2/3a)

Offers

CSIF (CH) III Equity World ex CH Blue - Pension Fund Plus ZB (link)

Swisscanto (CH) IPF I Index Equity Fund World ex CH NT CHF (link)

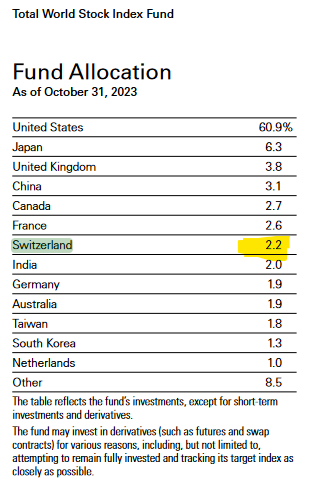

which are almost identical and both follow MSCI World ex Switzerland. that means I’d have to mix in some SPI or such to reflect swiss equity. however, when looking at the composition of VT, i find

I.e. only 2.2% allocation in Switzerland. So I consider just dropping Switzerland exposure for the sake of a simple one-fund-(almost-)all-world-portfolio

3 VIAC (P2/3a)

offers the same two as finpension above, plus iShares Core S&P 500 (link) which is not all world

=> same approach as finpension

I‘ve linked this whitepaper at another place here already, but will do so again:

It‘s really good and talks about an all-weather approach and touches on the original idea by Harry Browne, with his permanent portfolio.

It‘s not really lazy though what the paper proposes, as it has quite some components.

I‘m trying to persue a lite-version of risk-parity/all-weather like approach, while levering it up a ton to essentially try to match equities in good times and outperform them in bad times.

For sure it increases risk, that‘s the intention. It‘ll essentially just increases the overall volatility.

If I lever up a risk-parity/all-weather portfolio with 10% volatility by 2x, I get 20% volatility.

So similar risk measures as an unlevered 100% equity portfolio.

Or what specific risks are you refering to? Margin call risk specifically?

In generell such a portfolio was never of risk of a margin call in history, so far.

Take a risk parity profile x2 and backtest it, you‘ll see the max drawdown is still not more than 100% equities.

Leveraging something with low volatility overall 200% is totally different than levering stocks only 200%.

One of the risks going forward is of course correlations being substantially different then in the past.

Some reasons, from the top of my head:

not everyone has access to cheap leverage

holding such a portfolio is insanely hard, right now for example my managed futures are performing terrible and are in a 10%+ percent drawdown, dragging down my returns, while the equity portion of my portfolio is ripping. Times like these you feel like an idiot holding substantial parts of the portfolio. Most can‘t stay the course. In an equity drawdown, at least everyone is in the same boat essentially.

high conplexity, either you need to be knowledgable yourself or have an advisor that can handle it for you, but as stated above it‘s a hard sell to clients.

Tax implications, in other countries the rebalancing costs you a lot of tax. We can do it tax-free

taking out a loan to invest is pretty tough psychologically as well, especially when a part of the portfolio underperforms.

Stacked products to get leverage more easily only recently became available.

and of course 20% volatility are still 20% volatility. People who struggle with 100% stocks will also likely struggle with a leveraged risk parity approach.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.