What about Festgeld from NKB?

1% interest for a period of 7 months and commission-free. But minimum amount is 100k CHF.

I do not know if a private account with them is needed.

What about Festgeld from NKB?

1% interest for a period of 7 months and commission-free. But minimum amount is 100k CHF.

I do not know if a private account with them is needed.

Don’t forget to look at real rates too. Inflation’s been at 3.3% this year. So what you’re getting are still negative real rates.

Better to invest as much spare cash as you can in real assets (stocks, real estate, gold etc.)

Why does it matter? Just get the highest rate regardless of inflation. It’s still comparable.

Real rates might be relevant for long term financial planning, but that doesn’t really matter here.

Sure, for short-term needs I agree. But if you find 2.75% nominal interest attractive for 10 years: nope, sorry. Personally, I already find 1.5% nominal interest for 2 years a bad deal.

Depends how the future is. Such nominal CHF yield would have been amazing for a risk free investment in the past 10y.

Sure, better than before in nominal terms. But considering inflation, it’s actually not that much better. Sure, you can always hope for deflation. But in deflation, stocks usually do much better, especially if we’re talking long-term horizons (5-10 years).

So if you take the 2-year rate of 1.5% and inflation stays at 3% you’ll have a real rate of -1.5%: you’ll have lost 1.5% at the end of 2 years.

Just saying, only looking at nominal rates is deceptive. People are stuck in nominal thinking because we haven’t had inflation for a long time.

Would you mind explaining further why you think it doesn’t matter here?

Exactly, for such short duration you want a low risk investment, whether it beats inflation or not is not relevant, what matters is how much value you preserve/gain.

I’m afraid by focusing on short term inflation (we don’t know how long that will stay high), people might end up chasing riskier assets beyond their investment horizon.

Additionally, if the purpose is to compare the best available returns for a given amount of volatility we are willing to bear, the inflation adjustment will be the same over all the alternatives and comparing nominal returns makes sense.

In this specific situation, the investment is meant to cover a nominal expense (taxes for last year, so an amount that is not affected by 2023 inflation), too.

Using real (inflation adjusted) data becomes necessary when doing expense planning and considering what amount of risk we are willing to take to reach our goal. Our future expenses are subject to inflation so not planning for it bears the risk of falling short on our actual goal.

Given that year-on-year inflation increased again to 3.3%, I expect the SNB will raise rates again in the next annoucement, perhaps to 1.5%.

My big fear though is that the SNB has permanently changed their mindset and will lower the interest rates again once inflation is back to <2%. People (as in the real estate lobby, the government and big corporations) have gotten way too comfortable with easy money, low interest rates and the SNB going on these massive buying sprees to artifically support the export industry. I really hope we’ll go back to normal levels of interest rates (average for CH historical is 2.5%) but realistically we’re probably stuck with real rates below zero. And you can’t even escape this by buying foreign bonds unless you want to take a big fat forex risk.

/rant

No, not yet. Will think about it soon.

any online application possible ?

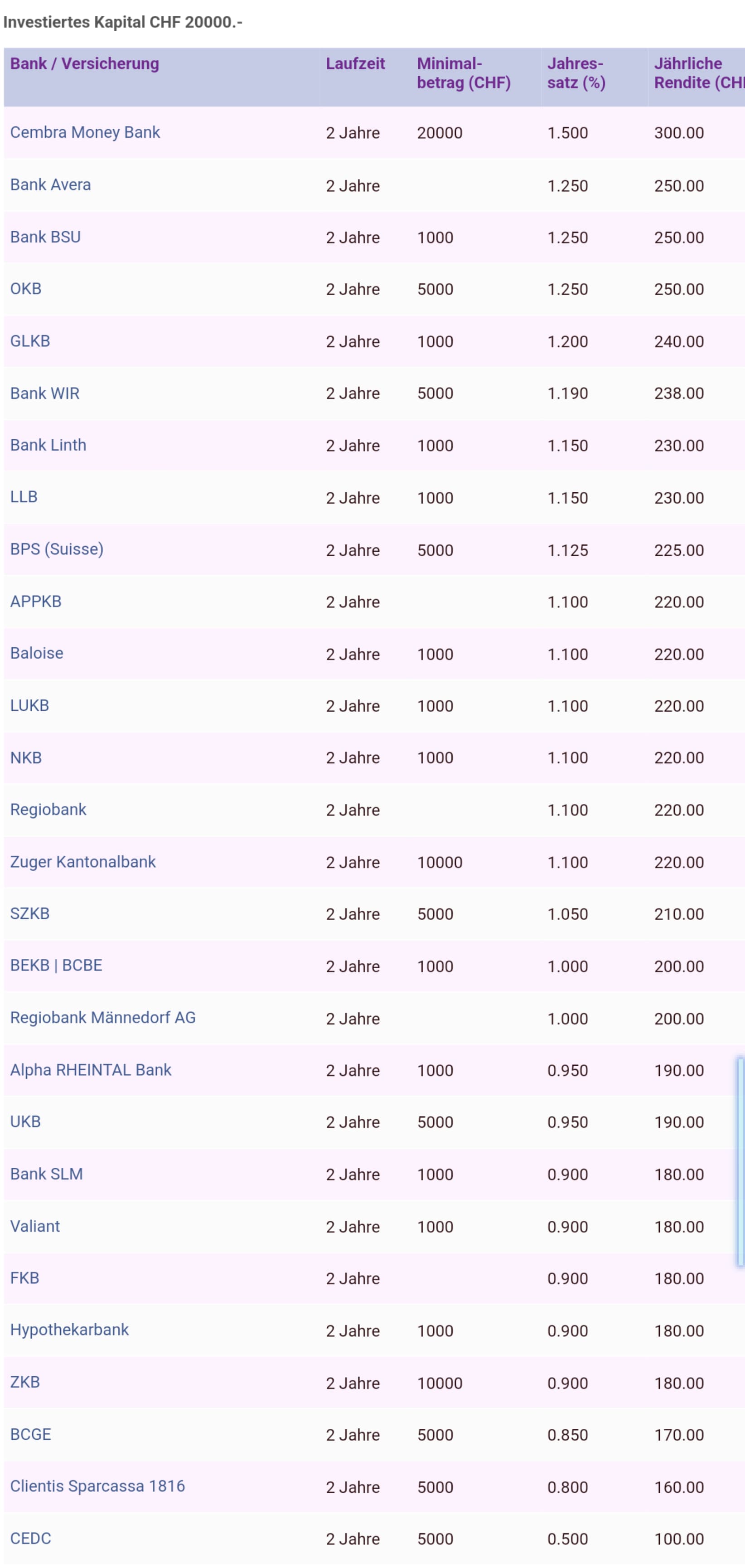

Was looking at the Cembra possibility.

Looks interesting, yes.

I esp. like, aside from the competitive interest ![]() that, in these uncertain times, “Die Kassenobligationen der Cembra Money Bank AG sind durch die Schweizer Einlagensicherung pro Kundenbeziehung bis zu CHF 100‘000.-- gedeckt.”

that, in these uncertain times, “Die Kassenobligationen der Cembra Money Bank AG sind durch die Schweizer Einlagensicherung pro Kundenbeziehung bis zu CHF 100‘000.-- gedeckt.”

Actually it means that couples can open 2 individual accounts and get 200k CHF state insurance… without being accused of cheating ![]() .

.

Small question: if I leave the country and move abroad, there is no way to recover the withholding tax, right ?

Nope, already had that issue…

But depending on the DTA, you can declare it in your residency country (kind of like the DA-1 in Switzerland)

One downside is that the compounding doesn’t work here, because they pay the interest out yearly. ![]()

But that might be the case with all mid term notes, never tried any before.

And this still gets taxed as income, right?

posted at wrong place

Splendid duration, too bad my german sucks. I guess the next best deal would be 4 years @ cembra.

I have question, I you move abroad and i.e have 10 obligations with cembra, they will ask you to close accounts? Thanks!