This is true is if you consider just the numbers for the mortgage and not the savings Rent vs Buy

Not sure if you watched the speech of Jerome Powell today. Everything during the last months points to high interest rates…if not something even worse…

In general is not fun, but the calculation of the bank is to sustain up to 5%

This is of course a speculation, but at the same time we are talking about the house where I’m planning to live in. Maybe it’s going to be profitable for the first decade and less profitable (or a loss the next decade). Speculate in four-story building (having the money), in my opinion is a completely different story.

Not sure if it makes sense for everyone, but I would not pay 2500-2700/month for a flat, that gives me an higher quality of life, but 700/month sounds more affordable.

What if the stock market crashes and real estate stays stable? What if both are going to crash? What if BTC will go to 100k? What if US is going to start a war because there is no solution to the mess they created to world wide economy?

If you have a spare 100M you can buy farms like Micheal Burry did

so just to check the numbers. You borrowed 850k, and your net worth is 850k. You also invested 1’200k in real estate. That would mean you’re 140% invested in real estate.

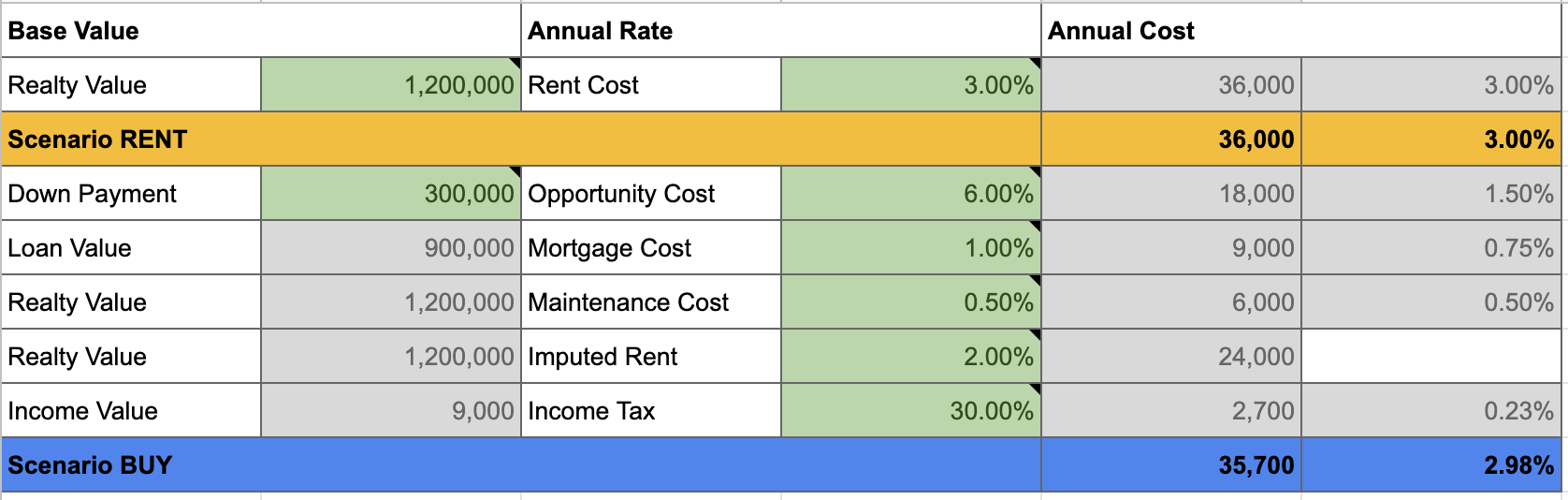

By the way, I made a simplistic buy vs rent calculator. You could plug in your numbers and see what comes out.

For example, for the following numbers, it’s a breakeven scenario:

Is your mortgage variable or fixed interest? Did you protect yourself against this scenario? I guess you can always switch from variable to fixed, right? In this case you would get a double hit. Not only would the interest cost more, but also the value of your house would drop significantly.

One scenario I heard of, is that the heavily indebted countries (like USA) may want to cause high inflation in order to devalue their fixed-rate debt. We could also see the state wanting to have higher control over the real estate market, in essence becoming the largest landlord in the country. I guess this has already happened in USA during the last crisis. All it takes is that the central bank raises the interest rate high enough. People can’t pay their interest, commercial banks have liquidity problems, so the central bank or the government steps in and buys out these flats/houses for a fraction of the price and makes a deal with the former owners that from now on they will become a tenant and pay rent to the state.

It’s uncomfortable to live with the sense that the central bank can change the interest rate any time, at will.

Hey thanks for that! I played around with the numbers.

As we discussed previously, the biggest concern is the value of the house in 10-20 years.

In addition, the values that can change quite a lot the results are: the interest rate, the maintenance cost (I agree with you that 0.5% is fair) and the return from the downpayment (6% I think is fine, unless we consider only 10 years and/or we are going towards a recession).

I tried to simulate also buy a house in 2011 when the interest rate was roughly 3% (10 years), but without the other numbers, it’s hard. For sure the value of the house (depending on the canton) is more than 20%, and that’s a huge difference.

Fixed, unless I can create some realistic projections where Saron makes more sense.

In general I don’t think low interest rate will last forever. You can always switch from Saron to fixed, but then the question is when (it can spike and then go down again), and at the time you decide the fixed one, it can make the entire deal worthless.

If I’ll spend the time to research and invest money, most probably it would be more effective than constantly watch (and decide) what to do with the mortgage.

Some people in the forum think that the best choice is Saron…let’s see in 5 years.

2008 was terrible in US

Sad but true

If you read something by Noam Chomsky, you will get depressed instantly.

The FED is creating just pure chaos. They are close to a stage where they want, but they can’t raise the interest rates, and usually this kind of situation brings to a war.

If the house market, stock market or whatever related to the economy goes -50%, probably we will get bigger problems than comparing buy vs rent

I did a quick calculation and if, after 8 years, the interest rate is going to be 1.70%, it will cost the same as 10 years Fixed 0.98% (that’s my present offer)

IMO the SNB won’t rise interest rates in our lifetime again.

There is so much debt that interest payments alone make up 10% of the US government earnings, expected to make up 20% by 2028. Japan is already paying 210 billion $ in interest every year, on 530 billion tax earnings…

There is simply no way to finance that with higher interest rates.

It depends on inflation, if inflation picks up meaningfully I’d be surprised if rates don’t follow. I don’t think a central bank would abdicate that easily on their stated mission.

I missed that part, I guess all the headlines are about the war they’re moving out of. What’s the new country where they’re deploying troops? Taiwan? (if so we might see WW3 indeed).

The FED cannot raise interests and at the same time inflation is going high…to me it’s sounds suspicious that you hear in the news about Taliban just right now

Yes, the FED and ECB have pretty much cornered themselves with low interest rates. Now, at unsustainable government debt levels, all roads likely lead to Rome pain.

Luckily there’s still hope for the Swiss Franc, but obviously our economy is heavily affected by other economies. My hope is that the SNB would fight inflation if it starts to become significant, contrary to what the FED / ECB is doing. Those central banks are just moving goalposts at this point (inflation ceilings become “targets” or floors or targeted averages over a unspecified amount of time). Our currency has a much longer history than the USD and I’m still confident that the SNB would have the foresight to prioritize our currency over (possibly) short-term economic interests (e.g. avoiding a market crash or GDP slowdown due to disruptions in exports because of a strengthening currency).

However, that would mean that the SNB does in fact raise interest rates in our lifetimes.

Maybe there will be more efficient ways of inflation control than interest rates. How about controlling when money can be spend and giving it an expiration date? You could do this with a digital currency.

Sounds crazy now, but China is already testing this out.

To me that just sounds like putting gasoline on a fire. I would treat any currency unit like a hot potato and I can’t imagine I’d be the only one - that’s basically what hyperinflation looks like. I don’t think that would work, especially not after inflation picked up so that it’s in people’s mind already (not the case with CHF right now).

This stuff is too complex for most people to predict (myself included). It depends on external factors, black swan events. I agree that it might continue like this for years. But if something bad should happen, it could be on a really large scale.

By the way, I wonder who is buying these expensive houses/flats and how. I have really good income and I save a lot of money, but I have no chance to buy any attractive property within 20 min S-Bahn ride from HB. My parents bought land and built a house with their own money (no mortgage) in 2000. This is unimaginable today in Switzerland.

If you think it as an individual, you need to have an extraordinary income to afford 2m chf.

But if you are a couple you need 350k combined gross income and 400k deposit, half of which can come from 2nd / 3r pillar.

I am following the real estate mkt in Zurich. What i see is that houses / flat up to 2.5/2.7m chf go super fast. This means there are few couples with combined salaries close to 500k or less but keen to put down more equity (if people have been working in ch for more than 10-15y should have a nice 2nd / 3rd pillar)

Close to 3mil chf is starts to dry up and this is where you see most properties advertised as price on request. The posters do not want to create a price history and traceable price reduction in case they don’t sell timely

But this has to be an extremely rare case? I work as a freelancer in IT, and it would take a couple where both earn more than me. Then they would have to decide that they will leverage their entire wealth 3-4x in order to buy a house. This does not seem like a sound economic decision.

But indeed, any decent property around Zurich goes for 2-3m and is gone fast. Whatever stays for longer is crap. You have to act fast and have no comfort when making the biggest financial decision of your life. Meanwhile in Thurgau or Aargau you can find houses for 1m.

A friend bought a nice flat at Zürisee for 1.5m. He applied directly after the offer appeared online. Then he took part in a blind auction. An old woman has deceased and left the flat, the family decided to sell. He submitted the highest bid and won. To me that seems too much like a battle for scarce resources.

Investment banking / hedge funds. Pharma and IT may pay even more. Advisory services even more.

In terms of fight for scarce resources. That’s true and almost anything above 2 million becomes an emotional decision rather than financial decision. I ran numbers many times and there is no way it makes financial sense above 2.5 million but still many do.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.