Dear Mustachians, would you consider buying “baurecht” / leasehold properties? I just found a really good one on the silver coast, about 400k cheaper than the next viable alternative, but it’s in a leasehold so the only thing you buy is a depreciating asset (and a forever-pay-interest scheme - the current contract runs into 2098).

I know in general it’s not the best idea in terms of a real estate investment, but again - still cheaper to live, enough place for a family, tax benefits, etc…

I would stay away from it, as you correctly noted you would only be buying the depreciating part of the property (with all the costs that come with it, i.e., renovations). If you can’t/do not want to afford buying, then you’d be better renting instead IMVHO. But I am open to change my mind :).

Re: all, I keep getting back to needing to buy an own place (house, flat, you name it). Must be an intrinsic drive deeply rooted in my Eastern-Europeanness…

We happen to live in a very nice but unfortunate area, where everything belongs to financial institutions (mostly pension-based), so they’re never going to sell. It’s a bit itchy though to spend almost 40k a year on rental costs…

So I am coming back to the vicious circle of “let’s move to where I can afford something”! That’s apparently only in Aargau for the property we’d be happy to live in, but mostly in small villages in the middle of nothing or very far away from Zürich (~Sempachersee area). Not gonna live there and miss my Zürich city life and all the amenities around us. At least not for now, I guess.

So option 2 is buying something to rent out (buy-to-let). For this, the message is echoing in my ear that a real estate investment is not a very good one in terms of rental income and liquidity vs the stock market.

How do I get rid of the real estate bug from my ear?

For those of you that did buy property with a sole reason to rent it out, how’s it going so far (vs. VTI/VWRL)?

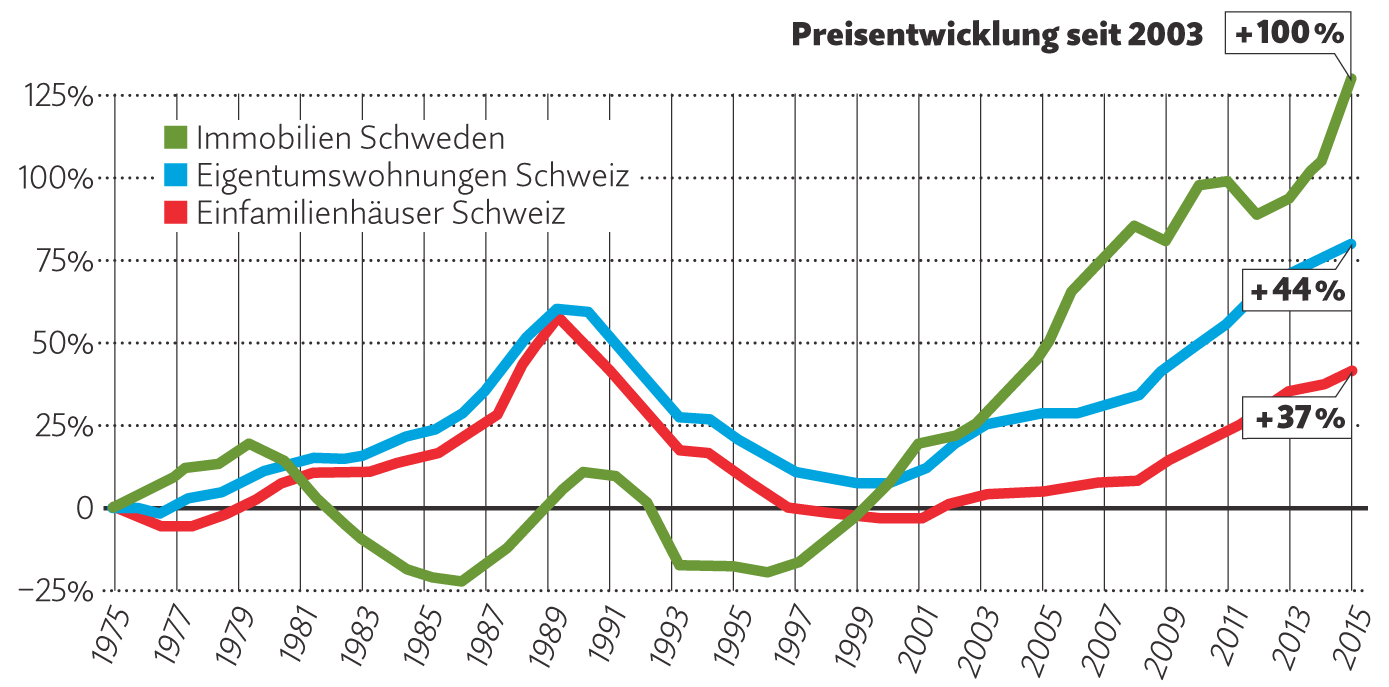

in a nutshell: your rental yield will probably not exceed 5% after income tax (I suggest you roughly run the numbers based on a property of your interest). So the only way to beat the VT’s is to count on the future appreciation of the property when you will sell it (attention Grundstückgewinnsteuer!), which is, as someone rightly said here, a matter of things “turning out well” (or not).

success factors in our case:

20% down payment (seems to be 35% nowadays, certainly negotiable)

buying at a good m2 price

reasonable Nebenkosten

challenges we faced:

(racist) neighbours complaining at the Verwaltung for every detail and sometimes you need to massage them even if they are wrong, in order to avoid bigger/other issues

replacing/repairing household appliances may offset your annual yield

our reco:

Level of the Erneuerungsfonds → if there is not much in it, investigate. The stinginess of the co-ownership can leads to issues when things need to be fixed and no one / majority does not want to pay

check future required renovations like roof, pipes, fassade etc as these are killing your yield and might require cash if the Erneuerungsfonds is not high enough

direct amortization level: again, might offset your yield

manage the rental yourself vs. outsourcing, but then be ready to be reactive when a repair needs to be done etc

a good Verwaltung (call them before you buy)

Please note that these elements are coming from our own experience and from what we have witnessed from friends, for condos. Might be different if we talk about apartment buildings.

We found the deals on Homegate and we define ourselves rather as “mom and pop” investors.

I have the feeling that the levels are so high now, that the good deals (within our means) are gone, and we do not have connections/network. But happy to be proved wrong

My last recommendation would be that you need to LIKE managing real estate as it is necessarily coming with a bunch of issues. We faced some pretty heavy ones, but we still do like it and look for further opportunities, now rather in our home country

with floor heating and a heatpump and a modern kitchen

selling for 730k

with a current tenant who pays 2300 gross a month (which seems to be a fair market price)

That’d give me a net yield on capital of 5.1% with the Swiss ROI calculator and considering a 0.7% mortgate interest for 10 years. The next renovations should come in around 10 yrs. (ofc I still need to have this analyzed with a property pro).

Worst come to the worst, we could(?) get rid of the tenant and move in and pay just 500 or so francs worth of interest instead of paying 3k a month in rent here.

I see it as a good investment oppty, but please prove me wrong.

0.7% mortgage for 10 years seems low to me (would say rather 0.90-1.00%)

direct amortization required by the bank?

2300 CHF gross rent → you need the net rent for the yield calculation (excluding Nebenkosten)

Nebenkosten including Erneuerungsfond: how much?

if the apt was build in 2007, you may have to replace some home appliances soon (been there, done that )

if you move in you can terminate the rental agreement with your tenant. I recommend to give him/her more time than the agreed termination period/find an arrangement. Please note that tenants can still screw around and it might take years + lawyers in worst case scenarios (almost been there, done that…)

I’ve run the numbers with (my own) conservative assumptions (including a high marginal tax rate) and looks like the yield would be around 4%

It’s better to start with the “operational” yield first (not including leverage), which is 3.78% gross (then, somewhat less net - we don’t know how much). That’s not a lot…

Then make a few scenarios with different mortgage rates, including 5%. You never know how much rates will be in 10 years.

that’s unrealistic, the whole country would default with a 5% rate (probably around 2-2.5% already).

and in 10 years I’d be happy to repay them 500k cash if needed if the rates would hike significantly.

The best I could say about it would be as potential diversification

You are buying an underlying asset that returns 3.78% gross before purchase taxes and costs. The rest - mortgage- is financial engineering. This could be applied to other investments too (margin loan - although clearly there are different risks and complexity in borrowing to buy shares vs property)

Out of 3.78% you need to budget for repairs and maintenance - banks advise 1% but I would budget more, depending on the flat and building including heating system, roof, exterior

2.78% gives a P/E of 36. According to google the 1 year prospective P/E of all world share index is about 18 (earnings 5.5% of price). Earnings of companies will grow supporting a higher P/E whilst I assume it is unlikely the rent on the property will be able to be increased considering rent controls in CH

The challenge with investing in residential real estate is that it is not only an economic asset, for someone else it is an emotional need, your own place etc . If you try to buy an investment property in the current boom market you are bidding against people who are willing to pay excess asking prices, viewed from a purely economical perspective

So then you are left with potential price appreciation - will homeowners continue to pay higher % of their salaries on real estate, perhaps wage inflation will arrive ? Or perhaps interest rates will change up or down which will impact how much people are prepared to borrow and prices? Migration? Political interference? I can’t control or easily predict any of the above and would not buy a property on that basis, personally speaking

Good point on PE ratios. However, budgeting 1% for maintenance does not decrease your income by 1% (does it?).

Here you elegantly neglect the systemic risk of a stock market downturm, which is very much not zero at this time (look at the lost decade with net 0% returns), plus discard the idea that raising interest rates will also raise rent (as far as the market can bear it), as the reference rate will hike.

I’d say that apart from an empty apartment (which indeed converts your asset to a huge money sink), which is usually budgeted with 1%, you can pretty well estimate the costs and revenues of a property into the next 10 years, whereas the stock market can crash next year or crash in 9 years.

It’s a totally different risk/volatility profile with a not-so-much-different return profile (8.5 vs 6.6% in this case).

You make a good point that in general rental return from property should be more predictable than stocks. Before leverage the return you calculated is about 2%, is that worth it?

I talked to Raiffeisen they would only advance a 75% loan if rent would cover interest rate at 5% and (if I recall correctly) 1 % for maintenance

Only you can answer if it is a good deal for you. I have rentals and personally my min rental yield would be 5% to be sure I can cover interest and that I don’t have to rely on price appreciation to make a return

It went down 33% from 1990 to 2000. You probably need to go back to the great depression to get a decade that bad for equities. But at least equities are not leveraged.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.

)

)