Never ever buy covered call strategy etfs.

These are terrible investments.

And especially terrible in Switzerland, due to taxes.

They essentially turn tax free capital gain into taxable income.

Really really bad idea.

Never ever buy covered call strategy etfs.

These are terrible investments.

And especially terrible in Switzerland, due to taxes.

They essentially turn tax free capital gain into taxable income.

Really really bad idea.

I think the points you are trying to separate are in fact related, if not intertwined.

When the proverbial shit hits the fan, people tend to care more about actual cash flows, hence steady (and growing) dividend paying companies are valued more dearly and are thus less volatile?*

Also, as @oslasho states succinctly “prices are more volatile than earnings/payouts”.

Anyways, I go back to what I stated before: the textbooks try to mathematically explain the market, finance, and ecomonics, and why a dividend stock after ex dividend day is only worth the previous price minus the dividend.

However, economics, finance and the market aren’t hard science – the curriculums are listed under social sciences, and IMO fear and greed play a much greater role than the modern portfolio theory or the EMH.

To quote Warrent Buffet: “I’d be a bum on the street with a tin cup if the markets were always efficient.”

And to wrap it up again: come up with a plan that you can live with, stick to it.

I feel maybe i am giving an impression that somehow I do not like dividends. This is not what I am trying to do.

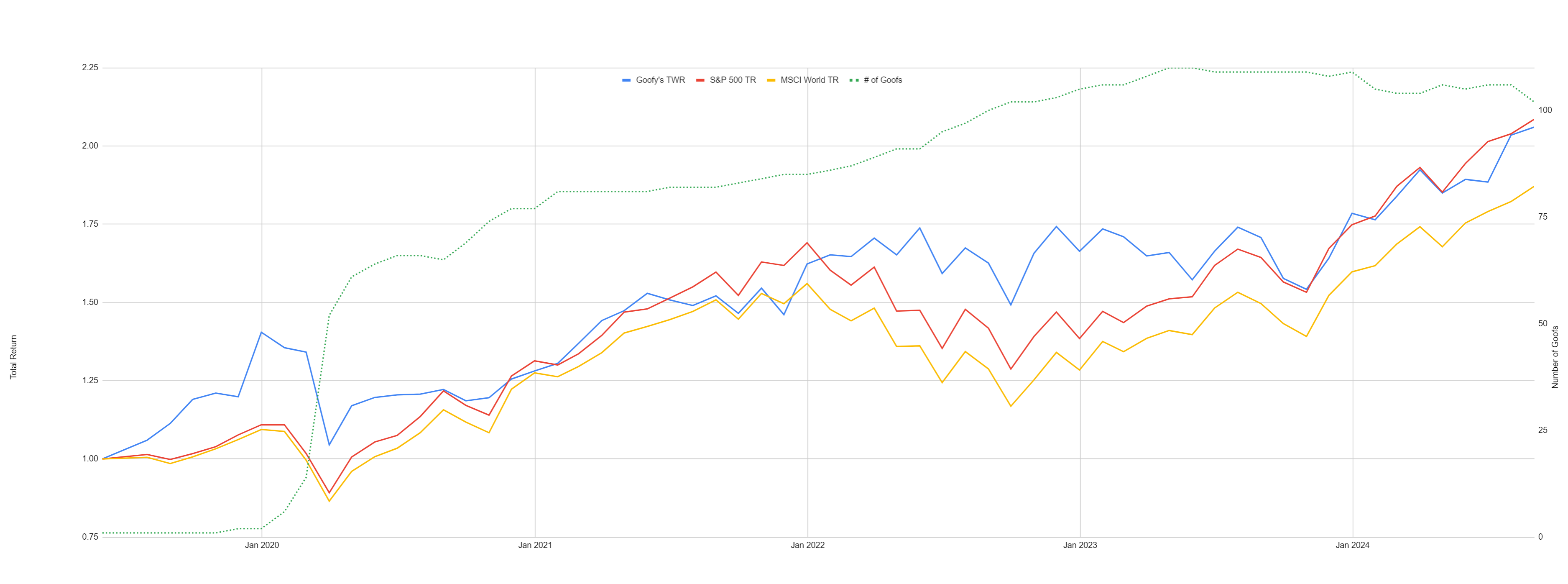

However, your portfolio is performing well with respect to volatility and returns because you spend so much time in doing analysis for the companies. Those FAST charts and long commentary is adding value to your stock picks. I understand that dividends is one of the criterion but you are doing a lot of other checks too (aka Goofy likes it). Is it not the case ?

If someone wants to build an active portfolio after fundamental analysis and have preference for companies that pay dividends, then it is fine. But I think we cannot conclude that just because company pay dividends, they become less volatile or provide higher returns. They still need to check the boxes for earnings growth, balance sheets, managements etc.

Having said that, I am going to try to find some research to decide if there is an equivalent ETF to VWRL with similar expected returns and lower volatility and higher dividends. Not to prove anything but just to be aware of the options when time comes.

The reality is that share price doesn’t truly reflect value or assets. You can see this in the volatility each day. The price might move by 50%, but the assets haven’t changed, nor the earnings.

Mostly* complete agreement!

Sorry if I came across with a different message.

Hmm.

So i am concluding as follows

A lower volatility portfolio would fare better in crashes. And one way to achieve lower volatility could be to a tilt towards dividends stocks as investor behavior in past represents a liking for these kind of stocks during bad times (still fundamental analysis need to hold though while picking those stocks)

Btw, I found something that might be of interest. MSCI World high dividend index does have lower volatility vs. MSCI world. It also was reasonably close in performance to MSCI world until covid and then it diverged which is funny because Covid was the biggest crash in recent history. However i think the divergence is linked to overvaluation of growth stocks Link Unfortunately i could not find an ETF for this index.

The main aspect is to avoid selling low. If you take dividends, you don’t have to crystallize losses or sell when prices are low.

If you take the strategy of selling to generate income, then you by definition are subject to SoR risk.

That’s the part I really don’t understand.

If you have the same ETF accumulating vs. distributing, if you sell to generate income vs. use the dividends (and reinvest the left over) it seems equivalent, right? If it’s not, what’s the difference?

To me the difference is really about the portfolio having lower volatility/different behavior in downturn, not the dividends vs selling part.

Yes there is an inherent assumption here that the two portfolios are not really the same and hence display different behavior in terms of volatility

If we are talking about VWRL vs VWCE, I am not sure why they would act differently.

The difference is exactly my example above: Investing for pessimists - #22 by PhilMongoose

To take an extreme example. Take 2 identical ETFs: one distributing, one accumulating.

You have 100 in the ETF comprising 10 shares. one distributes 10. other doesn’t distribute but you get an extra share.

so you have 10 shares distributing plus 10 of divi. worth 100+10. And 11 shares of distributing worth 110.

if the share price falls to 1.

you now have 10 worth in distributing (plus 10 of divi received) and 11 in accumulating.

you now sell 10 shares to get your 10 of ‘income’ and have 1 share left. oh no, you had to sell at the crash!

if price recovers to 100, the one holding distributing fund has 1000 again, but the one who sold accumulating only has 100.

A dividend heavy portfolio is exactly as much subject to SoR, than a non-dividend one where you have to sell.

Dividends are irrelevant and just part of total return.

Not reinvesting the dividends during a market crash (when all stocks are down and also if dividends are not cut during that time) is the exact same thing as cristallizing losses. @PhilMongoose

There is no difference.

Articles from ERN

Hmm, this sounds like a DCA vs. lump sum situation where picking a “bad” time can work against you. In practice if you sell let’s say every month/quarter, what are the odds of encountering some kind of adverse selection? This also doesn’t take into account the impact of rebalancing (if I sell during a 20% flash crash that might be almost all low vol/bond/etc positions and might even end up buying equity to rebalance).

Yes, it is a timing SoR risk. And it can work the other way. Imagine you sold NVDA at the recent peaks and crystallized those super gains.

For me, a decent dividend yield is simply for peace of mind, because I know I have no active maintenance in general and no need to sell in (nearly) any scenario. Hence, my argumentation is based on psychology, not market theory.

Market theory is quite clear: If you sell regularly in RE, dividends are irrelevant to your portfolio. However, the nature of the composition of an all-world portfolio vs a dividend focused portfolio is certainly different, with the later weathering a storm probably better* (a heavy growth stock valued on potential future prospect might not survive a bubble bursting, your energy utility provider most certainly will). If you retire during a highly elevated asset bubble phase this may matter to you, certainly does to me. Of course this is market timing and goes against theory, but then again, this is for peace of mind.

*Edit: But of course at the cost of also lower expected returns.

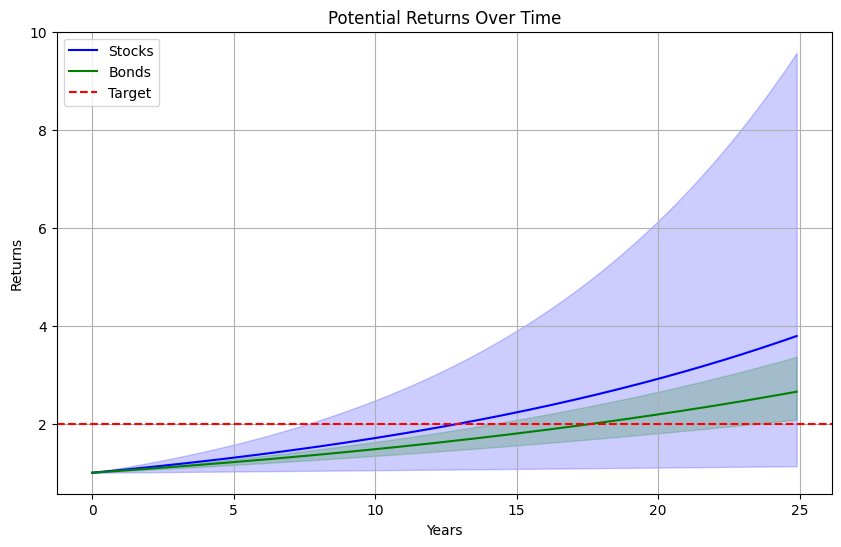

If you need to hit your target, it can be better to have lower expected returns with less volatility versus much higher expected returns, but where volatility means you can miss your target 20% of the the time:

| DISTRIBUTING | ACC | ||||

|---|---|---|---|---|---|

| NAV | Shares | NAV | Shares | ||

| Begin | Shares | 10 | 10 | 10 | 10 |

| Yr 1 end | Shares | 10 | 10 | 11 | 10 |

| Crash | Shares | 1 | 10 | 1.1 | 10 |

I tried to tabulate what you said. I think you are missing one point. How does dividend ETF actually pay the dividends ? Both ETFs have same money in pot. So the NAV cannot drop below cash value.

I am going to assume some dates to show the calculation is a bit different.

DIVD - Dividend paying ETF.

ACC - Accumulating ETF

Jan 1 2024 -: 100 CHF is invested in both , so investment in both is worth 100 CHF

Over the period of 12 months, both ETF collected 10 CHF dividends from underlying companies but one distributes and other does not.

31 Dec 2024 -: Both ETF are having NAV of 110 CHF.

Dividend is paid

1 Jan 2025 -; DIVD is worth 100 CHF and ACC is worth 110 CHF

Now next 12 months, same thing happens and both collected 10 CHF more.

30 Dec 2025 -: MARKET CRASHED 90%

NAV of ETFs drop but they also have cash collected, so value would be DIVD 20 CHF (10 CHF cash + 10 CHF value of underlying stocks ) and ACC will be worth 21 CHF (10 CHF cash + 11 CHF value of underlying stocks)

Now after 10 CHF dividend is paid, DIVD drops to 10 CHF

After selling 0.5 shares of ACC, investment in ACC falls to 10.5 CHF

Market recover 1000%

DIVD goes to 100 CHF

ACC goes to 105 CHF

How does dividend ETF actually pay the dividends?

Pays before the crash.

The NAV cannot drop below cash value.

I’m talking share price not NAV, share price can fall below NAV. When you sell, you sell at the share price not the NAV.

After selling 0.5 shares of ACC

You need to sell 4.76 shares of ACC to get 10 CHF.

Market recover 1000%

DIVD goes to 100 CHF

ACC goes to 105 CHF

You now have 10 x 100 = 1000 of DIVD

You now have (5.24-0.9*) x 210** = 911 of ACC

*You had to also sell 0.9 on 1 January 2025 to manufacture the dividend.

** I think ACC value should be 210 not 105

I understand your logic but there is no way ETF value goes below the cash it holds. It’s just not possible because 10 CHF is worth minimum 10 CHF at any given point of time

Sure, but even taking your numbers, ACC investment ends up with 55% value of DIVD investment.

In my calculation ACC ends up higher then DIVD. I was assuming 1 share of each ETF. So I said one needs to sell 0.5 share to get 10 CHF.