Because volatility can hurt you. Let’s say you have a 1000k portfolio and you need 100k which you take out at the start of each year. For the sake of argument let’s look at scenarios where portfolio gets 100k of income (tax free) at 10% and a scenario where you get 10% as capital gains.

Let’s say at the start of the year, due to market volatility, the portfolio drop so 200k. In the capital gain scenario, you sell 100k are left with 100k, which at the end of the year grows by 10% to 110k.

In the dividend scenario, you get dividends of 100k and no growth so stock is worth 200k at the end of the year.

The next year the stock recovers by 500% and in the gains scenario you have 550k, in the dividend scenario you have 1000k still.

because it was worth 1000k, there was internal growth of 100k paid out as dividends and then the share price fell to 200k.

Typically companies keep paying dividends longer than they should do. Just look at MPW and INTC as recent examples. IMO, they should have cut dividends a long time ago to preserve cash.

Now if they eventually fall, then there’s no big difference, but it they recover, the dividends smooths the volatility.

Let’s say you bought share at 1000 CHF and it gives 100 CHF dividend once a year. If market dropped by 80% and now share is worth 200 CHF the dividend doesn’t come from somewhere else, the share price will fall to 100 CHF after paying dividend.

I guess you could look at the recent covid crash and run the numbers to see if in reality collecting dividends worked better than selling during the crash.

I am trying to explain this simple fact to many mooks on reddit who bleat the dividends are irrelevant claptrap without understanding what they are irrelevant to…which is valuation.

@Abs_max yes the share price drops by an equivalent value but that’s a) slight accounting gimmicry from the brokers, and the company continues business activity which will produce more cashflows. The idea of the share dropping, while true, doesn’t make sense outside a vacuum. Just like the dividend irrelevance theory.

I look at it like this: dividend-paying companies are chickens, dividends are eggs. Payment of a dividend leaves you with a chicken and an egg, not a chicken minus an egg. The company put effort to create cashflow to pass on to shareholders, same as the chicken ate food. Then you can either eat the eggs, store them, hatch them for more chickens etc, while selling is basically killing the chicken.

Edit: too much hallucinations from the hyper-optimizers and the penny-pinching tax averse misers, from the handful of people who I know to actually live off their investments (and not talking about real estate) they all have a sizeable allocation to dividend-paying investments +/- bonds. All looks good on paper to sell but reality could be very different. After all selling is an act of market timing, and could come at a terrible point.

I am not saying dividends are irrelevant . I am just saying they are equal when it comes to value creation

My understanding is following

Company makes money (cash flow)

It can either reinvest in itself or pay dividends

For example sake -: let’s say company distribute 100% of Cashflow. This means every year the company will only produce same cash flow. So NAV is 1000 and cash flow is 50. every year cash flow is 50 and NAV is 1000 if market continues to value at 20 times cash flow

But in other case when company reinvests in itself , the cash flow is growing every year because company is becoming bigger. So NAV and Cashflow is following

Year 0 -: 1000 , cash flow 50

Year 1 -: 1050, cash flow 52.5

And so on… 20 times cash flow

In your chicken example -: in dividend scenario, chicken is always same chicken. But in capital gains scenario chicken is growing and giving more eggs.

This is theory. In the end it comes down to companies being able to continue to grow cash flow at the rate they reinvest. And I think there is a particular metric for this. Not sure if it’s called Return on capital or something else

That’s the issue though, history tells us it’s not. There’re a lot of data showing that dividend payers and growers massively overperform. Ben Felix yields (pun intended) that this is because dividend payers capture a handful of Factors like Value, RoI, Quality. Being a bit of a zealot myself, just for dividends, no aggression intended.

There’s an important nuance here which is the payout ratio: how much of the revenue is distributed, it can go from healthy to very unhealthy (impacting growth potential), so it’s important to track.

What you are saying is that higher volatility portfolio have sequence of risk returns challenge.

That’s correct

But why should a dividend paying portfolio be less volatile than non-dividends paying portfolio.

That’s all I am not able to understand

If it’s because investors treat dividends stocks differently and thus they are less volatile, then it’s a different topic.

However this is not what the discussion above was focussed on. @PhilMongoose was saying dividend portfolio ends up with higher value in case of crash just because they pay dividend

Okay now we are aligned

If the main point is that dividend paying stocks are less volatile and perform better than market then it’s fine. At least data shows that

But again - I don’t think it’s because they pay dividends. Most likely they are great companies anyways. Like Hermes, JNJ, LVMH etc

I think paying dividends make companies disciplined and less rogue. Which eventually gets back into performance.

Because the type of companies which pay and grow dividends are in inherently less volatile sectors. The companies don’t have much use for their cash, so they distribute it.

That’s one part, another part why real world dividend portfolios may be less volatile/more successful is because their holders have a specific mindset. I can totally feel that the dripping of money which feels free to one’s account keeps them motivated and more likely to weather a storm, hence their portfolio may do better than someone’s who’s in all hyper trendy stocks that fluctuate +/-20% on a semi-daily basis.

P.S. Coca Cola is the archetypical dividend King: their product is the same (so no extra R&D costs), it’s everywhere (so no extra logistics costs), it’s known by everyone (so no

extra marketing costs), it’s cheap, people love it, prints money for decades, so what to do other than just return it to the shareholders.

Yeah, but then if you’re happy with your portfolio allocation wrt volatility, then it shouldn’t matter. You could reinvest the dividend automatically each time there’s a distribution, and sell some allocation neutral amount from your wealth to live off and you’d have the same result (besides some potential drag due to extra trading, but should be minimal).

So it’s more of a matter of knowing what portfolio/volatility you want instead of dividend vs. not.

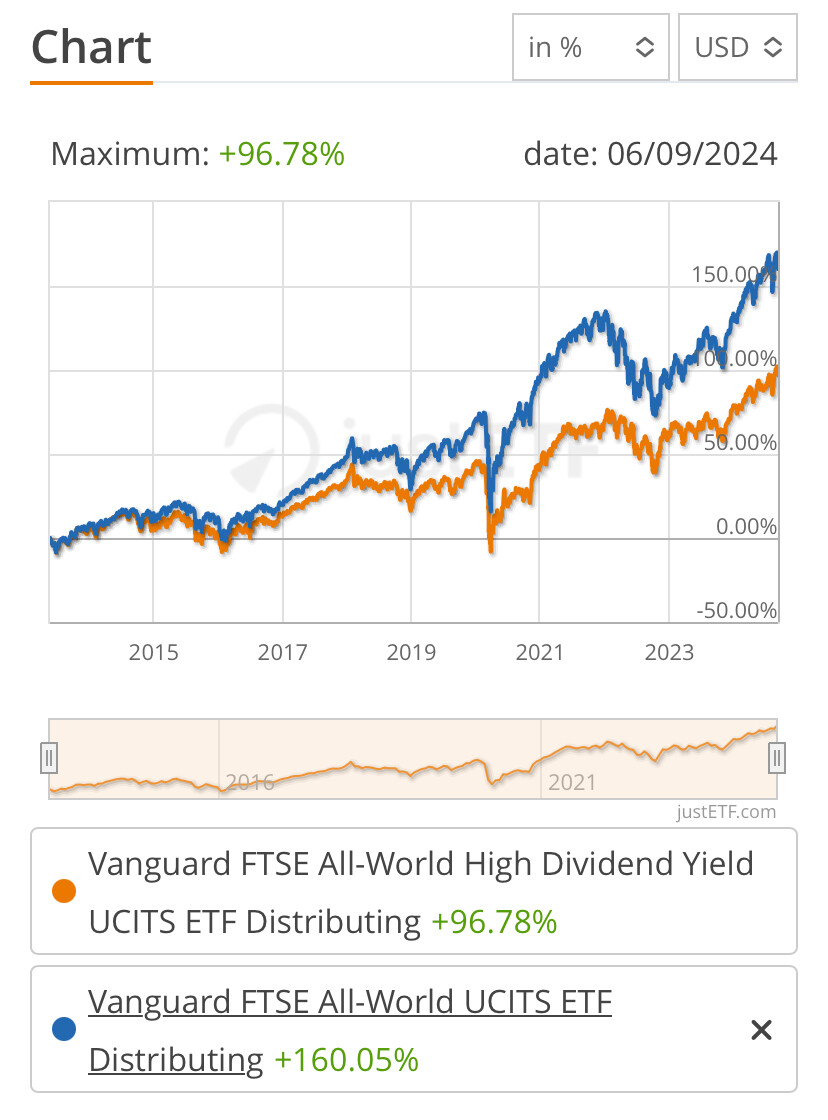

By the way, all my ETFs pay dividend. But I assume you are referring to high dividend ETFs. Which ticker are we talking about? Is it VHYL? Because that didn’t really outperform the world at least since both of the cousins exist ( VWRL and VHYL)

I just want to see some details and do research so that I can decide what to do when I am close to retirement

Yeah, there’s an important point here that you allude to: that getting to them needs one to become a stock picker, or buy ETFs which pick stocks, and that’s a mental hurdle I find very respectable.

There’re arguments for and against this point. Intuitively it makes sense to me, but not to everyone. Someone can say that stock buybacks (unless following Buffett’s rule!) are a gimmick to raise stock price and reward the C suite, and that forcing financial discipline via having to pay dividends cuts back on trips to Hawaii for staff.

The argument is that management needs to be very disciplined financially because dividend cutters are severely punished by the market, so one can argue whether the reason is good (to maintain stock price because Joe Schmoe wants their dividend), or whether one should care about the result (company remains disciplined).

I have FUSD and intend to grow it, captures primarily growth by focusing on Quality, and then filters for the highest dividend payers. It’s more of a growth fund than a dividend growth fund. If I was in the US I’d get SCHD which focuses specifically on dividend growth.

VHYL gives away a TON of performance for dividends, I wouldn’t have it now, but could have it much later in life.

Not a bad pick, but I feel this is not capturing what we were talking about here: This is nearly US only (~95%), very heavily concentrated with top three (Apple, Microsoft, Nvidia) accounting for >20% of the portfolio (which also explains its recent outperformance) and less than 100 stocks total. Ultimately, also offers only a 2.01% dividend yield, compared to 3.21% of VHYL and 1.64% of VWRL (all data from justetf.com).

I mention this because I would be very happy if anyone knows of a good alternative to VHYL. I am happy with VHYL, but I have an awful lot of money in it by now and am considering splitting it in two (similar) ETFs/portfolios.

You’re right on FUSD, I am buying it now to a) bump my US weighting and b) in the hope it will be raising dividends in time. And because I like the screening criteria.

VHYL just filters for dividend yield, I don’t know that there’s something much better if you’re after pure yield in Europe.

If JEPG has stood the test of time by the time I am to RE then I could consider going into it in a big way edit: @Tony1337 if the tax-free status on UCITS ETFs distributions (and capital gains) in Greece is still there when I retire It seems its big brother JEPI is not doing bad at all, and not losing NAV like the YieldMax stuff are. VEUR looks good too.

Otherwise purely from a screening perspective I think SCHD is among the best (though US-only).

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.