Wow, every newborn gets an account with $1’000 worth of SP500. Parents or any other person or company can pay in $5’000 every year and deduct it from tax.

The compounding income is free of tax until the age of 18 when it can be paid out or left to continue. I think this compounds to the first million with 26 years of age.

Now that is what I call a retirement plan, FIRE for everybody at 26! A whole generation of millionaires that can only laugh at the attempts of some countries to state pension provisions… at age of 65-70.

Great, more free money rolling in the S&P500, it’s really not that much money going in, all things considered, though.

Estimated ~3.5mn new-borns/year in the US, taking 1000+(5000/year) and compounding for 18 years with 7% CAGR results in 173,000 (3,300 if nothing is added above the 1000, not even enough for a good gaming PC!). Really not bad at all, that’s more than most people have, anywhere, at any time. If it’s then not raided it’d be great for them.

Hadn’t we done similar hypotheses here about the good it’d make if every country did that, and ended up feeling it’s a bit meh, despite sounding great?

The initial money is only 3.6 billion per year. The total in 18 years would be 324 billion. Compared to 52.831 billion market cap of the SP500 that is not that much.

But it is distributed evenly. There will be business models because everybody can deduct the money from tax. And every company can.

The CAGR of SP500 since 2012 (when I started recording) was 12.55%, since 2020 which I use for comparison to my own strategies it is 12.62%. Both numbers per market close yesterday. And both without dividends which have to be added and are tax free until 18 in this account.

Addendum: 324 billion paid in of course, the compounding would be much bigger than that.

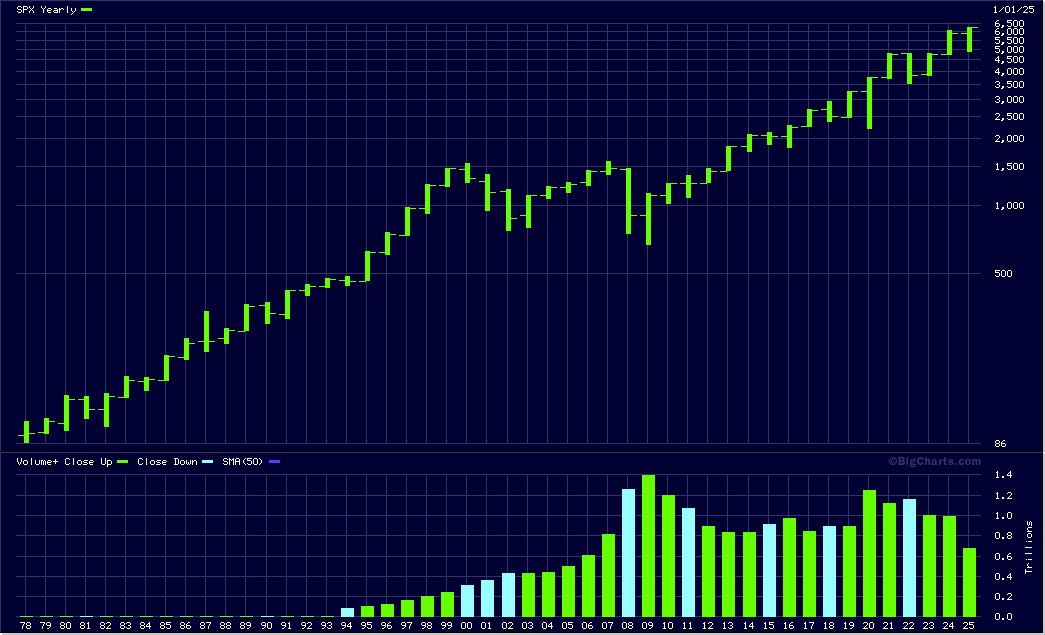

I hear that all the time, but we had a lot of losing years since 2012, 3 in total. Also the log chart does not look like a bull run bigger than the past:

Silberschmidt (national council member) proposed to open pillar 3a for children (Link). His (simplified) calculation is CHF3 a day leads to 1mio in 65 years with 6.5% annual return assumption. True power of compounding!

We could freeze all other retirement plans and safe a lot of money. But then, in 26 years, the not-yet-born would laugh their ass off about the people having to work until 65-70 and get less then they with 26…

99% of people have lower self-control than my now sadly gone and beloved dog, they’d piss it away instantly. These sort of initiatives should be tied like a trust, that something productive should be done with the money, most likely education-related.

I think the main point is that every baby will learn what investment in stocks and compounding really is. Personal experience that is not taught, cannot be taught in school.

Of course many will piss it away with 18. I had exactly zero Dollars at 18, wonder what I’ve done with the more or less 400’000 bucks at this age. But then I would have seen what compounding and investment in stocks really are able to do. I have found out, but a bit later and time is of essence here.

And then, what good does the money when you can have one whiskey a week and move in a wheelchair? With 18 you can piss it away with much more fun! The important thing is the decision is yours and not of some politicians!

And what is wrong with that? Better than waste it!

That is the nice thing… it is not. But hardly any youngster investing in an index fund today knows that. But if you have a head-start of 18 years you will know that, you will feel the pain of bear markets.

I was thinking they can do that with the money they earn themselves…then again when I was a student I did it with mom and dad bank money too

Ben the man Felix tells us all-stocks-all-the-time-for-everyone (with Direxion/small cap value tilt, of course, and no dividends, of course) is the best of the bigliest bestest.

Besides…nobody not personally investing has no clue what any of it means. I was an adult and remember the Greek stock market crash (both of them in fact), Enron and the .com crash, the 2008 crash and I remember thinking “ah nice, these c*nts in shinny suits eating at Dorsia are getting it” during all three.

That said, I am building a position in BRK.B for a couple of years now, 1-2 shares at a time, intended for my kids. However I also intend to be a total schwanzkopf about it, like the parents I used to hate hearing about: I mean to ask them to research BRK and present to me why it is a good investment, calculate the CAGR, explain compounding etc before I transfer them the positions. They will also need to colab about it. Hated hearing about these parents, now think it’s worth it! Edit: I recall that when I was a kid I wanted my dad to get me a bag of plastic soldiers to play war with my cousin. He asked me to estimate how much each of the soldiers cost. I thought he was a complete arschloch at the time, appreciate it now as it made me think!

Nah, nobody knows the future. But the past gives hints. Check the long time chart I did show earlier. 50 lost years until 1932. But anyhow, newborn in the USA will have a 18 years head start to all the youngsters investing in index funds today.

I did lose 50% of my investments several times in my life. I would not even sleep bad losing 80%. It is volatility that pays for performance, the earlier you learn that the better.

I don’t care too much, was born with nothing, will leave with nothing. Inbetween I have some fun…

I have a theory that the S&P500 (or other broad equities index) will become the new saving account for the masses, becoming the main store of value. As this happens, the risk reward ratio of investing in these ETF will go down and relying on them for retiring (early) will be insufficient.

I don’t think that will ever be an issue. The masses panic and sell, they buy high and sell low. Always. Just look at margin rates.

Not long ago I lost almost 50% of my money, many years of salary for hard work. It was the COVID crisis. I bought a lot on margin near the low, doing exactly the reverse the masses did (margin loans are always lowest in bear markets just before they turn and highest in bull markets just before they turn).

Thanks to the added leverage I even closed that year 2022 with a gain. SP500 lost 19.44% (temporary over 30%), but my volatility was bigger. Volatility is the currency you pay with for performance.

Now all the newborn in USA will have an 18 years head start. They will probably feel the pain volatility causes and see that it pays for performance. Some of them will take out the money and party, others will keep investing, others will start a business or whatever. But it is a clear advantage, 18 years of experience in the stock market. An advantage we did not have.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.