I put 1k play money on IBKR, but haven’t played with it because it turns out I’m not a playa ![]() it’s just sitting in VTI and done well like everything else, will probably get it out at the end of the year.

it’s just sitting in VTI and done well like everything else, will probably get it out at the end of the year.

In the end everyone has their own opinion on security. Security can mean different things for everyone

Account security -: availability of 2FA etc

Investor security -: (in case of brokerage bankruptcy)

Psychological security-: Brick and mortar / personal vs. Online only

Geopolitical security -: Swiss broker vs International

If you can rank IB, SQ, Swiss banks, Swiss Fintech, Saxo and Cornertrader on all of the above , everyone will come to different conclusion. Only a real finance + cybersecurity professional might be able to an objective comparison

What I have realized over the years is that it’s very easy to go down the rabbit hole and find issues with everything. What normally helps is data to differentiate between Anecdotes and larger picture.

Bottom line is following

- Swiss banks (UBS, ZKB, etc) have very high AUM , so if you are with them, you are going to be fine

- IB is one of the largest brokers , you will also be fine

- SQ is one of the best Swiss brokers , I don’t think you will have problems

- Saxo is one of the top European brokers with Swiss license , it is also going to work out fine

- same might be true for others too

There is always a cost to get added level of „security „ and comfort level changes with growth in wealth. When someone is new, 200 CHF per year custody looks ridiculous, but when someone has 5 million, maybe they will also be fine with 0.3% custody fees.

I just think we should always be objective in our information sharing because it can put someone else down the rabbit hole of over analyis. I also think I need to be careful myself.

What might help is diversification of brokerages and banks. In the end it’s all about money. So if someone has spread their money across 4-5 companies (including brokerage + banks+ deposits) , it is more than enough.

11 Likes

Great post.

Part of my switching from UBS to PF was exactly to go from %-based fees, as they will always go up, to flat fees. Then again I don’t have 5mn, or 1mn, or close to that, I bet it changes one’s perspective.

The rest is getting into diminishing returns territory for me, but totally understand people who want to optimise to the nth degree when the tools are easily accessible.

2 Likes

How do you do that? Pardon my ignorance but I don’t remember how it works for IBKR since it’s automatic.

What do you mean? It’s the standard process for swiss broker with supplemental US withholding.

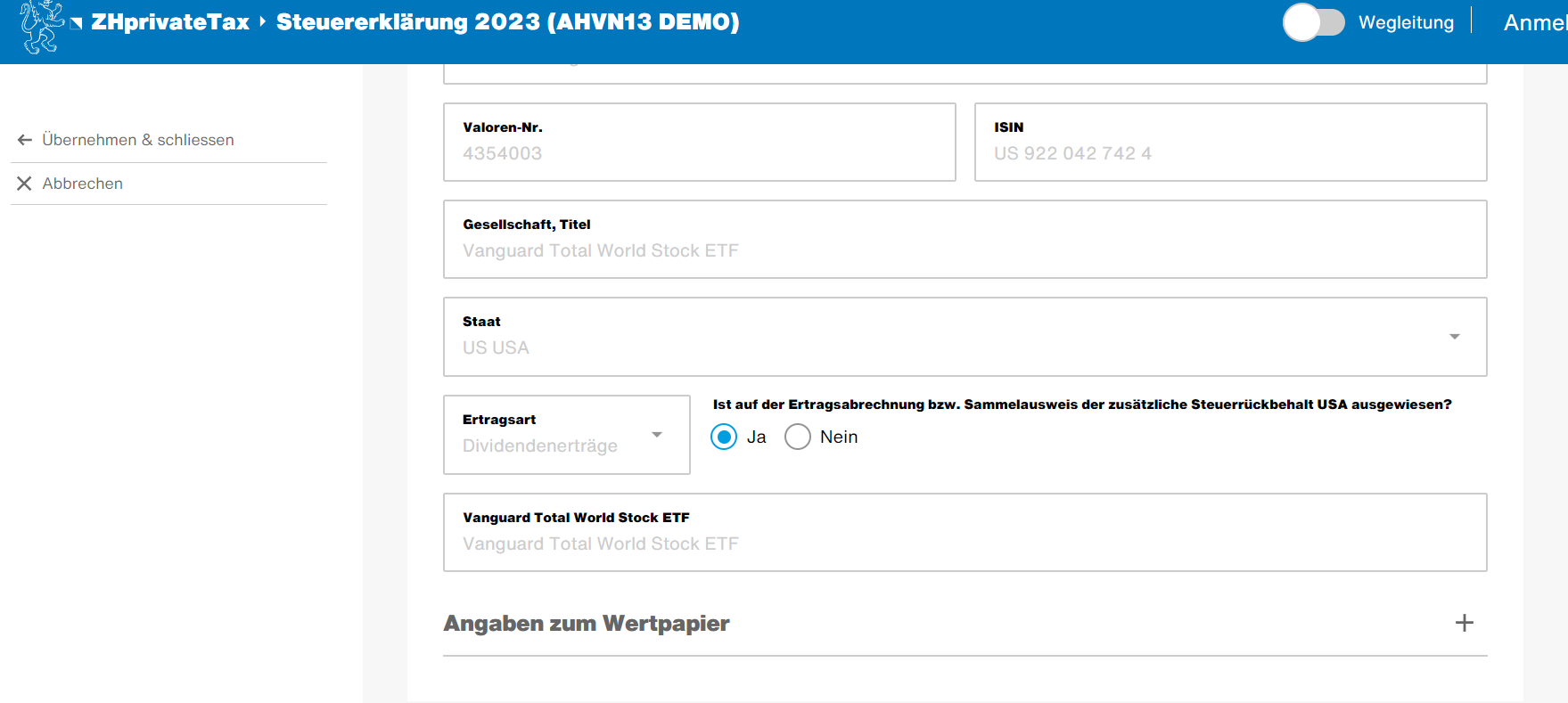

Replying to myself. I see on the DA-1 That the column for US is empty on my IBKR Tax declaration.

If I had them at SQ/PF I’d have to find out how to fill it.

My comment is going to be theoretical because so far i have not claimed that kind of credit. I mean i dont have US ETFs in SQ yet.

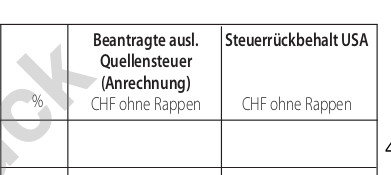

Lets say you hold ETF worth 25000 USD and dividend income is 500 USD

How it works is following

- You will fill a W8BEN form at SQ and this means your US ETFs will have 15% WHT (=75 USD). Important point is that not all swiss brokers can do this step as they need to be Qualified intermediary.I do not know who else can but it’s always good to check first. Thus it is critical that you only hold US ETFs at Swiss brokers if they have Qualified intermediary status. Or else there will be problem in recovering money

- On top, SQ will deduct additional 15% (=75 USD)

- When you file your tax return, you will use the DA-1 form and claim back both. You need to check the box as shown below which will automatically capture 75 + 75 = 150 USD.

- Of course you need to show proof that SQ actually did deduct these taxes

4 Likes

By the way, the latest broker that almost went belly-up was a Swiss bank called Credit Suisse (anyone remember?). It paid Swiss salaries and it was regulated by … FINMA.

Just sayin’ …

![]()

10 Likes

Decided to read up on the previous replies in this topic after dropping my Credit Suisse turd above … now I have a few more comments:

TL;DR: pick a pure, global broker instead of a bank/broker, Swiss or not does not matter at all.

In more detail:

-

Myth: “you’re fine with Swiss banks with large AUM”*

Well, you see, I already mentioned the Credit Suisse near-miss catastrophic accident - I get it, it’s already over a year ago when this cluster- … ahem, little pile-up was elegantly averted, thanks to a couple of governments chiming in - but for those of us stubborn enough willing to look back even further than 13 months: going back in time the previous last time a Swiss broker almost went belly up was in 2008, when the other large Swiss bank, UBS, needed a bail-out from the Swiss government.

Both banks are/were Swiss, both have/had gigantic amounts of AUM.

Did I already mention that both are/were FINMA regulated?

In my book, this puts to bed the idea all three triplets at the same time:

- Swissness

- large AUM

- FINMA

Sleep well and tight, little triplets! Let me tuck you in.

If you still think the Swiss finishing touch guarantees a better outcome, I commend you to it and I wish you good luck!

-

Myth: “Cyber security is better at (Swiss) bank X versus (international) bank Y”.

Maybe. Maybe not.

I can’t really speak in much detail here, but when I last worked at one of those two major global Swiss banks (one remains), actual cyber security measures depended on the knowledge of the team or department head (read: a person so far removed from technical judgement that they would only be reminded of their lack of knowledge in the case of an actual breach).

Maybe it’s better now? The sheer size of the remaining organization make me doubt it.

-

Myth: “Brokerages go belly-up all the time, hence I need to distribute my eggs amongst many (brokerage) baskets”

This one intuitavely resonates most with me. I don’t want to lose or at best be stuck with my assets for extended periods of time when my favorite broker goes out of business.

However, let’s look at the brokerages that actually went belly-up in recent times.

- Lehman Brothers in 2008.

- MF Global in 2011.

- Peregrine Financial Group in 2012.

Were these scary moments in time? No doubt.

Was retail investors’ money lost in any of these? I don’t know. I doubt that investments in custody accounts went missing.

Does picking your particular slice of brokerage providers protect you from these events? Hopefully.Good luck.

If indeed I would join some of the permabears and doom-mongers - none are on this forum, of course, just mentioning for completeness that there are people with such a mindset on the Interwebs - then my recommendation as a retail client would be as follows:

-

Pick a (mostly) pure broker instead of a bank!

Avoid brokers which are just part of a bank (or any other financial business like payment service providers - hi, Postfinance!) instead of just using a pure broker (like IBKR).

Let me explain.

Essentially, a bank’s entire business is to take risk to make profit.

Let me repeat: “a bank’s business model is to take risk in order to take profits”. Insert Charlie Munger’s quote of “show me incentives, I’ll show you outcome”, and you’ll inevitabily see people taking too much risk for seemingly outsized profits. It’s just human behaviour.

Most banks do this prudentially, some not (see above, and below).

When a brokerage is tied to a bank, and the bank takes a hit because it took too much risk, well, guess what, the bank goes down and it takes the brokerage along with it. You’ll get whole, as a participant of their brokerage, eventually, but it might take some time.

Conclusion: pick a broker! Or a bank with its main business being a brokerage.

* Paraphrasing some of the suggestions above.

** Including the Swiss banks mentions before - UBS and CS - , but feel free to throw in Julius Baer as the third largest Swiss bank)

14 Likes

Even in a bankruptcy instead of a bailout, people wouldn’t have lost their assets held in brokerage accounts, nobody else could have laid a claim on those.

(I even think that all the depositors would have been made whole as well, tho there could have been some period of account freeze above 100k while they reshuffle things)

edit: I see you touch that point below, for me it just doesn’t matter, I don’t really worry about assets disappearing on any reputable broker/bank.

3 Likes

Fully agreed, though the turbulance endured during the time endured would have been epic?

Took a few days for Lehman Brothers to transfer the retail brokerage accounts: Customer and Employee Losses in Lehman’s Bankruptcy - Liberty Street Economics

That sounds pretty quick.

1 Like

Maybe my phrasing might have been misleading: I completely support your message.

I meant to address those on this topic who feel that a broker like IBKR wouldn’t live up to their promise of keeping their assets safe.

1 Like

Thanks for your extensive explanation.

-

Banks. I fully agree that banks are inherently risky. But the history shows, that large, systematically important banks are rescued in case of trouble. In 2008 Abn Amro was nationalized, ING was helped, Swiss banks (though i am not much informed about Switzerland) were also helped. Lesson: some large banks are too important to let bankrupt.

-

Brokers. They also rake risks. The risks are different, but any business may go belly up. Fintech brokers like DeGiro constantly search for the boundaries. Specifically DeGiro had a serious issue with separation of own and client assets. It is not widely known beyond the Netherlands, but there was a mingling of customer assets and DeGiro’s.

-

IBKR. Looks very good, I am with them. But IBIE has two serious drawbacks. They explicitly refuse in their ToR to compensate if you are hacked. You must rely on thei system, while they give you no guarantees. Second, it is a sprawling broker, spanning lots of jurisdictions. It may be very difficult to prove your point in case of trouble.

Lokal banks have an advantage. You can raise a scandal in local press, if they screw you up, for instance. With IBKR it might be much more difficlut.

Anyway, if a bank/broker goes bankrupt, your assets should be nominally safe, except for fraud. The biggest remaining risk is cyber security and functionning of their systems.

11 Likes

What if they were wrongly spirited out of the brokerage accounts before the collapse, then you’d still be holding losses. In bankruptcy and collapse a lot of things that can happen that are not ‘by the book’.

3 Likes

If you have a large-ish 7 figure account at a Swiss Private bank, if your MFA is compromised even if due to your own carelessness I think it is reasonable to assume your client advisor would contact you if strange transactions start happening.

At the very least, you would be able to talk to your client advisor in advance and say that you would like this to happen

2 Likes

Let’s hope that the attacker who tricked you into giving them access to your account didn’t change your contact details on the ebanking site.

Client Advisor: “Hello, Mr. Barto …?”

Attacker: “Yes …?”

Client Advisor: “I wanted to call you about a transaction that was initiated on our ebanking system.”

Attacker: “Yes?”

Client Advisor: “It’s about that international bank transfer of x’xxx’xxx CHF to Sberbank Switzerland AG.”

Attacker: “Ah, yes, I indeed want to make this transfer. But thank you for checking in with me first - really appreciate it!”

Client Advisor: “No worries! Your transfer is now approved and should go through later today. Is there anything else I can help you with today?”

Attacker: “Not at this time, thank you. Have a nice day!”

![]()

1 Like

I know all of us trying to be rational and logical. But I think we should not trivialise the concerns people have or the comfort they have with certain type of establishments versus others.

5 Likes

Agreed … though in the same vein, we should also not over-dramatize?

1 Like

Agreed.