Tldr: how much does a CHF based investor need to account for CHF strength in the future wrt the SWR rate (sorry if this is a repeat question, in which case I much appreciate a quick faq/link).

IIUC the original Trinity Study has been done based on assets in the US, so US stocks and US bonds - as well as it took the inflation rates in the US. And the result of which is the well known Safe-Withdrawal-Rate of 4% (or any other, safer, figure you prefer).

My question now is, how does this famous 4% rule translate to other currencies.

Let’s take CHF as an example:

CHF has historically been a very strong currency - along side low inflation

a “CHF-based” investor has to multiply the performance of VT with USDCHF to get the CHF performance (and let’s leave hedging out of the picture, ie assume we do not hedge stock currencies)

if the performance of USDCHF matches the US-CH inflation difference, we’re all good. But I doubt it’s that simple and assume there’s a “premium” based on currency

Currencies fluctuate not only based on inflation differentials but on strengths of economies, function of the currency (eg safe haven), speculation, rate differentials (which are a result of various other factors including inflation difference) etc. Overall, I assume a currency can, mid-/long-term, divert from pure inflation (PPP) difference.

In which case this would have to be factored into the SWR.

The difficulty with the CHF is that its “very strong currency” status is mostly due to the fact that people around the world think it is a very strong currency. At least 90% of the SNB Central Money have just been “printed under the desk” in the last ten years and sold to people scared by their own currencies. Up to now it hasn’t been a problem inflation-wise because the new CHF’s are not circulating and sleeping on accounts or stored as 1000 CHF notes in safes. However, the day the buying pressure reverses, things could become complicated…

Why would you want to early retire in Switzerland and live like some poor person here in a tiny apartment or something? It’s nice for work, about the 2nd best salaries in the world, but for living you get much better bang for your buck elsewhere, e.g. in Portugal or Thailand

That’s the thing. When I talk to old Swiss guys in their late 50s who are still in IT and ask them why they didn’t emigrate, they say that kids and family and friends are here. I guess if you want to make it work with retirement in a different country, you need to do it fast, before it’s too complicated for the kids. And I guess it’s easier to do it for an expat: you just come back to your country of origin.

I would prefer to retire in Switzerland before 65. If the cost is a few more years of work, fine, that’s my choice. I am not sure to get your point. Do you mean that if one cannot retire as fast as possible he should just give up ER and work till 65 ?

As a Swiss working in an international organization, I generally give the following advises to new comers if they want to know Swiss people and maybe become friend with them : 1. learn the language (dialect is better, but plain German/Italian is fine) and 2. get involved in a club (music, gardening, church, dance, you name it). Getting into a club as an expat is not more difficult than for a Swiss, just fill in the form. Then take part and have fun !

Of course, your attitude might also help or hinder your efforts (if any) to get to know Swiss people…

Sorry to disturb the party, but it looks like this thread has diverged entirely from my original point. Which was about how to account for the influence of a currency on the save withdrawal rate. Esp, but not limited to, the CHF. Any input or thoughts on that front? I understand the reason why CHF is a strong currency, and that might change in the future, but given a strong currency my question is, how does that influence the SWR.

What ever is the result of this analysis, not a lot can be done:

-Invest only in Switzerland is a bad idea, stock markets are highly corrolated and the biggest companies in Switzerland are doing the majority of the income outside Switzerland

-Buy hedged ETF ( like iShares MSCI World CHF Hedged UCITS ETF) is a bad idea, more TER and the hedging is on a monthly basis. The hedging will have little influence on the long term.

-Invest in gov or corporate Swiss bonds is a bad idea the returns are really low.

-Invest in real estate, maybe. On the long term real estate has lower returns, so I have doubt that it would be better than full stocks.

So, at the end, either you reduce the SWR or you go to an other country.

For more info:

This paper analyses SWR in multiple countries.

In the case a Swiss invests only in Switzerland: the SWR is 3.59% (page 14)

You can play with this chart by selecting Germany and entering 100 under TSM/WLD

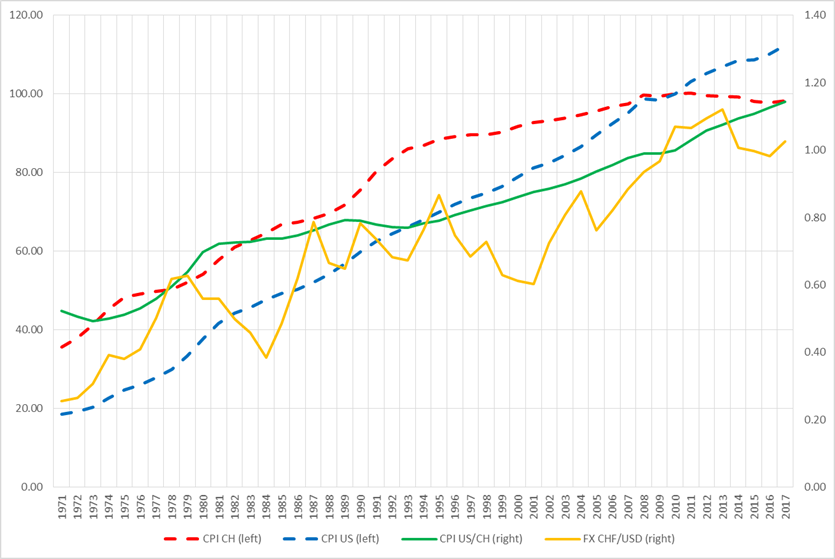

inflation difference between US and CH between 2007 and 2017 was 17.3% - while USDCHF lost 14% in the same period

inflation difference between US and CH between 1998 and 2017 was 37% and USDCHF lost 29% in the same period

So with some huge (currency) fluctuations, which can easily be in the 30% range, in the very long term it indeed shouldn’t matter (from a SWR point of view) in which currency==country you will spend money since the currency should adjust for inflation.

The problem is, however, that a currency can be stronger or weaker than what inflation implies for years (perhaps 5-8 years, in swan events who knows probably longer). That might influence the withdrawal strategy/timing

There so many possibilities that it hard to define a specific number.

it would also depend if you are ready to work again, if you work part-time or on some project, if you have income from the government, if you start your retirement in a bear or a bull market…

There is also this paper witch is interesting on the topic:

“Resolving the Paradox – Is the Safe Withdrawal Rate Sometimes Too Safe?”

Personnally, i thinks the CAPE approach is the best:

So it looks like in the long term, the FX rate really does follow inflation. And currently, it seems that the FX rate between CHF and USD is in equillibrium.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.