New to the forum, let me know if I’m doing something wrong with the post.

I have some cash sitting on my IBKR account. Am I wrong to understand that if I convert it to USD I get like triple the interest? Anything against this?

After depreciation should be roughly same return and more tax paid so generally not a good idea. If you do that and truly don’t care about currency risk, at least find a more tax efficient way (something like BOXX but do your own research).

My understanding of interest rate parity theory is that if financial institutions see an arbitrage opportunity, they would borrow in CHF at low rates and convert to USD at higher rates. USDCHF FX rate and interest rates will thus move until they reach a new equilibrium and the opportunity no longer exists.

So in theory it should not make a difference which currency you hold, because USDCHF is expected to decline to offset the higher interest rate. You can search “USDCHF futures” to see market prediction for exchange rates. In addition as a swiss resident you would pay additional tax on the higher USD interest rate. Risk is also a factor although I understand the amounts here are small

But in the end predicting FX rates is fool’s game…

For my curiosity, what’s the point of keeping cash in IBKR?

Sorry to jump in, but I find myself in a similar situation.

I will receive around 50k EUR and I already decided the following:

50% of it lump sum (25k EUR)

the remaining 50% DCA during the year (around 2k per month for 12 months)

Now, I already know I will buy VT in USD from IBKR. But:

if I exchange the currency with Wise / a bank I will pay substantial fees

if I convert it with IBKR I will pay little fees:

2A. from EUR to USD I will then already have USD ready to buy VT. Problem: high tax on 4% interest on USD

2B. do EUR → CHF (enjoy the 1% interest, low taxes) → USD (when I buy VT)

Is it better 2A or 2B?

In the end, everything will be converted in USD. But I will have to pay higher taxes if I do it early.

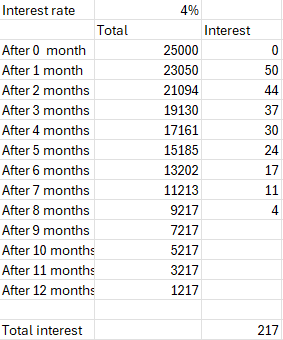

Probably the best option is to convert everything in CHF, and each month convert the 2k (+ my usual part of salary I save) to USD and buy VT.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.