So I was just reading around in a different forum and I saw a few posts regarding this. If I understood correctly, there is a tiered interest rate when it’s just deposited in IBKR? I have a tiny sum kind of just sitting in my bank savings account and I was exploring options. I have a monthly investment in VT, so one option was to just add more to VT.

But what about the option of keeping some money on IBKR? Would it be fine to keep money as a cash balance there? What about keeping an emergency fund there? At my level, it’s about 1%.

Or do you have other recommendations? I saw the Fixed options thread but there I got lost in the information and had no idea which to prioritize learning.

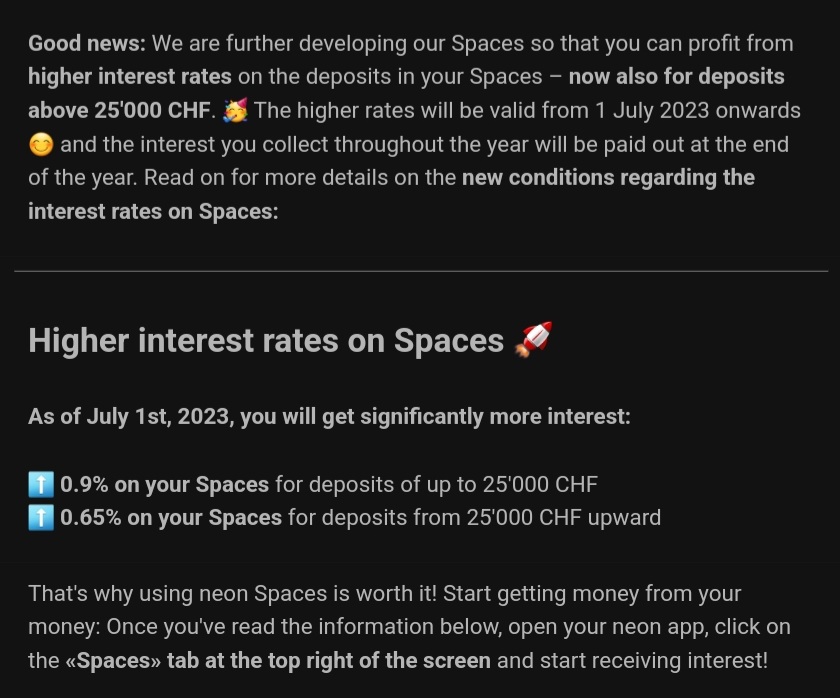

It depends on the amount but it doesn’t look like a particularly interesting option to me. E.g., if you park CHF 20k at IBKR, you currently get 0.38% p.a. in interest. There are various bank accounts where you get more than that. E.g., at Yuh you get 0.75% p.a. and you can directly use the account for payments (when you actually need the emergency fund), which is not possible with IBKR as it isn’t a bank.

For higher amounts IBKR may be better than most Swiss bank accounts. However, if it’s a larger investment (not just an emergency fund), I’d rather go for a short-term bond fund or maybe a money market fund.

Or are you considering exchanging it for USD where you get a higher interest rate? This wouldn’t make sense to me at all for an emergency fund of a Swiss resident, unless you have significant future expenses in USD. And as an investment, US treasuries might be a better option (if you want to bet on USD).

I am also interested in parking around 100k which would give me around 4% interest. I wonder if this is a good idea compared to my other option which was going all VT.

However, if i stick to just parking, is this interest taxable or it just goes into regular wealth?

Thank you in advance.

It’s fully taxable. I.e., your net interest will likely be below 3% p.a., while the current market expectation is for USD to weaken 4.2% p.a. against CHF.

Thank you. It seems I will never find a path to make my already small amount of money to grow… just when I get somewhat excited about something.

My original plan was VT and that is why i opened an account, but I am just worried that it will stagnate for years… I would be perfectly happy with 4 to 4,5%.

It could actually drop significantly right after you invest and take more than a decade to break even. I’d focus on my career to generate reliable income. Treat an equity index fund investment as a smart long-term savings account, not a way to get rich.

It’s a bit more complicated than that. I am looking for income outside my job with this cash for helping with a sabbatical year. I guess real estate rental would be better but I haven’t had good feeling about the opportunities I have found this far. I could get by with a few hundred dollars a month just so I don’t feel like money is only going out.

Possibly. But there’s decades of evidence to the contrary (when you’re looking at the mid to long term). What you should rather worry, I believe (and as has been said above) is short term losses.

Well, you alread found not only pillar 3 but also Bitcoin, Ethereum, Ada and real estate. That suggests you won’t be running out of paths to grow your money.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.