I’ve been reading and watching lots of videos about the current stock market situation and many experts are warning that there might be a large crash ahead:

I suggest that we discuss here the ideas how to prepare and to profit from this crash in the best possible way.

The author suggests a system of buying stocks up to 100% of your portfolio in the market drops 50% (the deepest point it has done so far). But I wonder in what do you relate these 50%. If the market is overpriced, then you only get back to “normal”, right? And what is normal price level and what is cheap? How do you determine this? Is CAPE ratio the best indicator for this?

One lazy guy answer is: you don’t. I’m currently 100% invested in stocks.

If you want to get 100% into stocks when the crash happens, then you would have to stay under 100% all the time, anticipating the next crash. And when it happens, at what point do you sell some stocks in order not be be invested 100% anymore?

You shouldn’t really expect to be able to reliably time the market successfully unless you have some sort of hedge, which you are unlikely to get by reading that kind of books. In an efficient market, if there was some known reliable way to beat the market, there would be enough people doing that it would cease to exist quickly.

If you believe the long term trend is upwards, stop worrying about the crash and just keep investing on a regular predetermined schedule. If you are in to gamble, that’s a different story.

I’m not so experienced in this, that’s why I’m asking. In the book I mentioned the author suggests that you buy stocks just once a year only if the stock market went down at least 7% compared to the last year. Otherwise you just hold them. In my understanding it’s not timing the market in the sense of predicting something, but adapting to the given situation compared to the past. I’ve listened to many videos from this investing program https://wealthtrack.com and the common theme of all these professional investors is to buy what’s cheap and when it’s cheap and then sell more expensive later. I cannot see how buying now makes sense as everything is so expensive: https://www.starcapital.de/en/research/stock-market-valuation/

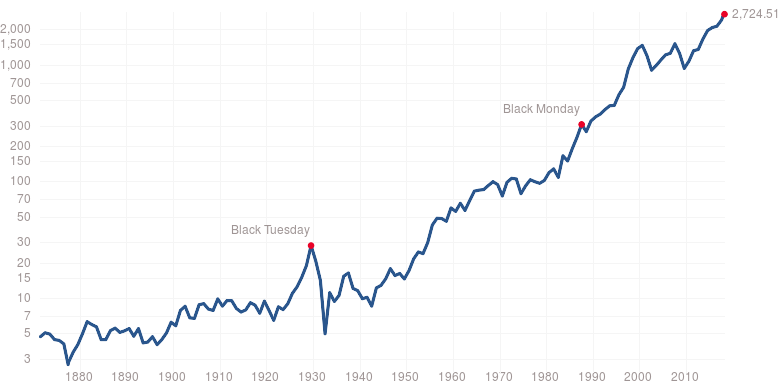

And here is a S&P 500 Total Return from Yahoo Finance. Total Return means it accumulates dividends. The chart is also on a logarithmic scale (like the one above), so a steady 7% growth would look like a straight line on that chart.

Why 7%? Why only once a year? On what day? What do you do if the stocks drop 10% in February and recover by July but your buying day is in January? These sorts of rules just don’t make any sense.

This applies more when you’re buying individual stocks, not so much when you’re buying world market ETFs.

Simplify: just decide how much money you’re going to put in the market per unit of time. Follow your plan, regardless of what the market does. Fight the impulse to be better than the average, you’ll probably end up losing anyway.

I beg to differ : in most implementations I see, passive investing is the belief that the american economy (given its weight in the world market) will continue to grow as it has done in the past, at least during your lifetime, and will not become, let’s say … Japan.

If the Us economy did not keep going up, I don’t think there would be that much passive investing.

One may argue that if US would go down, another country would takes its place, but that would be betting as well that the transition would be smooth.

And I am not denying the benefits of passive investing (it works very very well), but if you have been buying in the three last months, please don’t say that passive investing is buying cheap. From a value point of view (i.e, compared to the underlying economy earnings), the US stock market as a whole is the dearest it has ever been.

I think what to do depends on each investor’s investment horizon, size of the portfolio and willingness to take risks knowing there might be a reversion to the mean at some point.

If your investment horizon is 1Y before you start living from your portfolio is not the same as 20Y of full time work ahead of you.

Another perspective, if you already have 5 millions you can take more risks (but probably don’t need) and afford to live off 2.5M whereas if you have less than 1M, you may have to resume full time work.

in my case the accumulation phase should be shorter than anticipated (4-8y instead of 8-12y) thanks to good savings that bring +20% per year to my portfolio.

There isn’t much benefit to risk minus 30<->50% returns that could take 10-20y to recover so I have shifted some of my stocks to short term USD bonds and CHF cash to avoid big swings.

I am betting on a reversion to the mean for stocks returns in the next 4-8y.

If there is a big plunge (-20<->30% over a year or if CAPE goes low compared to the last 10/15y) I would consider moving back to 100% stocks. If nothing happens, well that would be an opportunity loss and I can live with it.

Emotionally

If you have not lived through a crash before you might worry that you will freak out and sell at a really low point and miss out. Maybe you can find an older friend or a mentor with the same investment strategy as you, e.g. buy and hold for the long term? that person’s experience could maybe help you keep calm, and invested? Another way is to have a portfolio with many different asset classes: commodities, property, bonds (I know, I know) etc. and hence the volatility will not look/be so radical as if you were invested 100% in stocks…

Financially

I would keep it simple, just stick to the plan. Buy every X months, stay invested over the long term. Re-balance once a year. Look up the statistics on outperforming the index. If you want some excitement of trying to time the market, the only thing I would do is to build up a little extra cash savings (from extra side-gigs, gifts, unexpected income etc. not from your regular savings) and keep it until what you think is the “lowest” point, then buy some extra posts.

My difficulty is to know whom you can really believe. I get the feeling that in finance someone is always trying to get advantage of you.

All the ETF community is saying that you shouldn’t trust financial advisors, who cost a lot and offer you expensive products. On the other hand you listen to John Bogle and he says you should never sell and just keep buying more. In my understanding he also wants people to keep money in his company. Active fund managers say that prices matter a lot and that buying at high prices leads you to losses or long waiting times till you start earning something. This guy Kiyosaki says Etfs are for losers and you just need gold (what is his intention anyway?)

I am confused by these contradictory messages and by not really knowing what are the intentions of people that give all these different advice.

It’s a belief in efficient market hypothesis. It has its flaws and there’s evidence to the contrary, but long term it’s not entirely unreasonable and saves you a lot of time and stress from not having to worry about your investments. And why shouldn’t US deserve a higher weight? Most of the world’s greatest companies are there, look at the top - most are household names far beyond the borders of US, about half of earnings are from abroad, and show healthy returns on capital, unlike what you can see in a typical non US market.

If you don’t accept EMH and want to buy cheap, I think you’d have to go picking individual stocks, not countries

It’s just a nature of this discipline, there’s a lot of uncertainty and no single “right answer”. The professionals don’t have all the answers either, they get around by managing the risks. You should examine the evidence for different strategies yourself and make up your own mind about it. Use historical data and backtesting for analysis, it’s imperfect tool in many ways but unfortunately the best we have. There are some sites like Quantopian where you can easily play with some data around without having to do a lot of dirty and expensive work to get it yourself.

Well, none of us here are fund managers (AFAIK) and we’re not asking for your money, so at least you know we’re not trying to take advantage of you. We might be totally wrong, though.

I don’t want to be paranoid about it, but the interviewed guy seems very convincing to me in saying that through such low interest rate as we have now, there are many companies out there that should long be bankrupt. Politicians are simply not acting in a decisive way and they keep shifting the problems to the future.

What in you opinion is the right way to act in case the bubble really bursts or before it happens? In my simple minded understanding one should do the following:

Have enough cash to survive the possible job loss as many companies could go bankrupt.

Buy as many ETFs as you can afford as the go on sale.

Possible buy some precious metals and maybe commodities now as they are not so correlated with stocks and may rise in price when the crash happens.

2+3 is basically “pick an asset allocation you are comfortable with and rebalance as appropriate”, which I think is sensible and doesn’t depend on whether you are expecting an imminent crash or many more years of bull market. Whether the inversely-correlated-with-stocks asset should be gold, commodities, bonds, cash, bitcoins, shovels, or a mix thereof is up for debate but AFAICT traditionally people have been recommending bonds.

First line of damage will be the Contingent Convertible (CoCo) Bonds investors. They are here to take the shock and they are well paid for it.

Pay your debts! You will then have free cash flow once the collapse comes and in collective you reduce today the debt present in the economy (anti cyclic measure).

You always find people telling the system will collapse. Maybe the positive to keep in mind is that bonds are not really safe assets as they are highly exposed to currency risk.

So there is this Polish website where the guy makes bold predictions on the future of the market. Recently he posted another article, which I am linking below. If you have time to read it, I would be interested to hear your opinion.

He says that US stock market is extremely overpriced and that he expects a decade without growth.

It is not really a secret that US stocks are very overpriced. Indeed if you look at simple measures like Shiller P/E ratio, which is currently around 30, it means that you should expect average annual returns of around 3% for the next decade if the market converge to the underlying economy.

So yes, I would be very surprised if we do not have a major crash in the two following years.

Having acknowledged that, there are two school of thoughts on the forum :

People that are there for the very long term, and who do not plan to retire in the next 5-7 years. In this situation, since the market will at some point reach new highs afterward anyway, there is no need to think too much about it. See for instance Nugget’s posts above.

People planning to FIRE in the short-middle term (5-7 years or less). In this case you cannot really be sure that the market will have time to recover after the crash. In accounting there is a saying that you have to match your asset maturities with your liability maturities . In this case your major liability is that you have to finance yourself at FIRE date. Then buying overpriced stocks (or overpriced indexes of stocks) is not the best idea because you might need the money before the market recovers.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.