I am working in finances for the state and hense my pension fund is Publica.

Today i calculated the average interest rate from the money people had in Publica since 2000 until 2022.

Using the formula " I = (Vf/Vi)^1/y - 1" the result is 3.26%

I = average interest rate over the period y

y = period in years

Vf = final value

Vi = initial value

3,26% is lame, but hey it’s a pension fund. Since i’m only 30 y/o I’m wondering how I can optimise that. I know that onces you have 20k there you can take it for your own home.

Could I buy a small flat for myself and live there for one year or so then rent it or sell it again ?

or could I buy a studio to live there and put it on airbnb so when it’s rented I go to my parents or girlfriends place ? (I’m at the moment back to my parents this is where I live) ?

What if I genuiely think about investing it into my main home but then I have another opportunity that makes me go abroad and sell / rent the place ?

Is there any other conditions required for me to get that money ?

Are there any other options you would think about ? Is there a way I can boost my interest rate of the money that is put into publica or I don’t have any word to say ?

I never dug deep into the pension fund so I don’t know what you can / can’t do with it so any clues are welcome.

3% might be ok, given how safe this is. Is this even a large amount of your personal wealth? (If it is, you might want to work on increasing salary and/or savings rate¸and if it isn’t it might not be worth optimizing for).

I avoided putting money into the Pillar 2 since the return was poor: around 2% a year during times when stock markets were racing ahead by double digits.

However, now that I am closer to retirement and stock valuations look very toppy, I’m filling the pension pot with a view to being able to invest it at higher returns post-employment within a vested benefits fund.

Well it is to me a non negligeable amount. Of course I have more invested with different brokers but it’s painfull to see this money stacking up and working at only 3.26%.

This is why I ask for some financials tricks to improve it’s yield. I know you can cash it out to buy an appartment / house but only if you plan to live there.

Do you know if there’s a way around it ? Can you live there and rent half of it by buying a small appartment building ? Can you buy an appartment and then decide to moove due to personal reasons (other job further away, mooving in with your partner, going abroad) ? Or will they ask for the money back ?

Yes for a young adult an average of 2% (3.2 in my case) isn’t worth injecting money. I know that when you turn 50 you can inject some funds to hit new yields but it’s still does not makes me salivate … I’m more looking to a way to cash it out and buy an asset out of it not a liability.

Yes. Finpension have some good knowledge articles.

I looked at this idea several times. The problem is net yields on property in Switzerland after repairs, maintenance and tax on hypothetical rent are too low for it to make sense as an investment. See separate thread about the swiss property market.

Note it might be more meaningful to look at the pension fund return in the past 2 years. 3.26% might be back weighted. Market conditions were very different 20 years ago

Thank you ! O.k. I will go a read on finpension … still I see net yield in property isn’t really worth it … maybe buy old stuff renovate it live in there a few years and flip it …

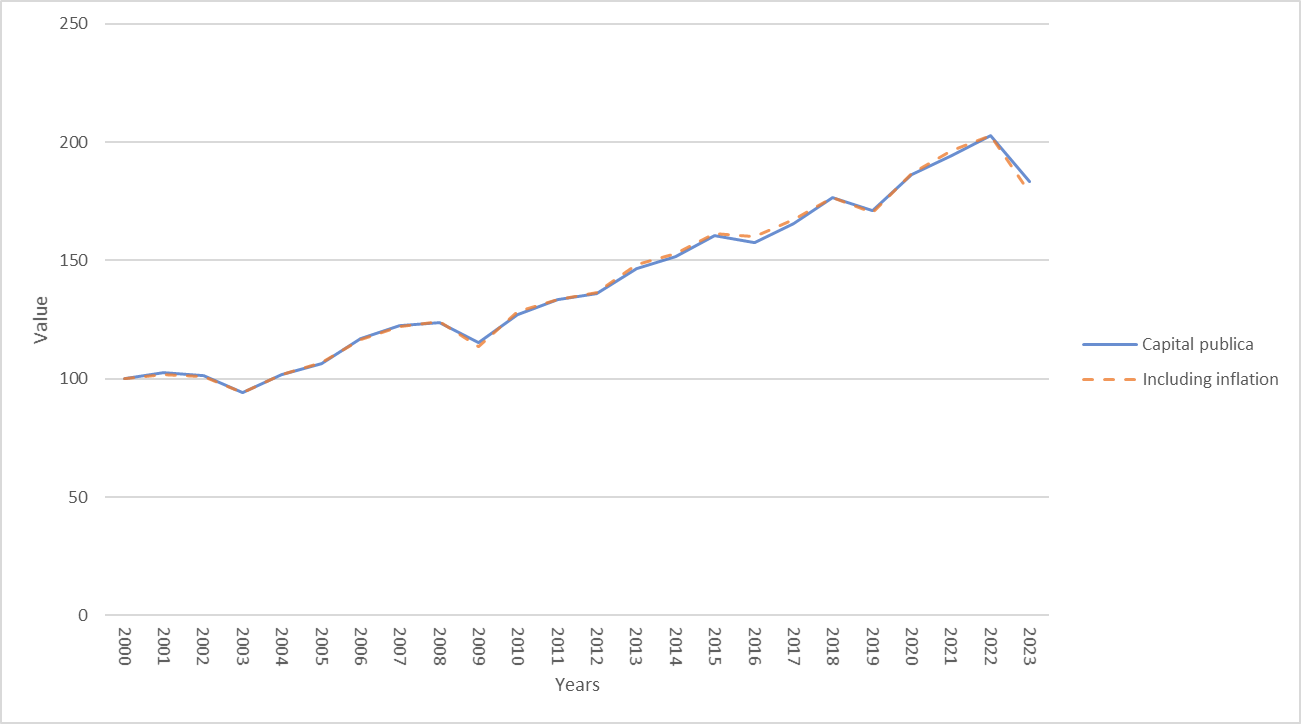

As for the yields I was a little optimistic here are some results with different time spans :

Note that 2022 was a bad year -9.63% for publica so if you was retired in 2023 well … sorry it would’ve been better to retire in 2022.

It would be interesting to consider inflation over the same period to see how much your net yield is…

I’ll do it and share in a next edit

EDIT : Plot edited with inflation in the orange curve. Inflation data found : Switzerland Inflation Rate 1960-2024 | MacroTrends

Anyways thank you all for your help and suggestions, keep them coming !

I’m also with Publica and yes the pension fund isn’t terrific, but it’s not the worse one. I think it is on the average and would be more interesting if we were 45+ years old than young

Also, it depends on your salary class for the state. If you are in the 24+ class, it’s a bit more interesting, although, only if you are 45+ years old.

It’s for sure one of the worst ones based on the Deckungsgrad (the pension fund’s state of health)…

On the other hand the employer contributions are above average.

This isn’t quite correct. While the returns and interest of a pf will most likely be lower than the market in the long run, it offers some safety, particularly relevant for people retiring soon and who choose to take their pension as a lump sum or if a prolonged period (e.g. 5+ years) of financial market slump takes place.

If you’re 64 and the market crashes for example 30%, you’re private investments will be worth 30% less. Your capital tied in the pf (assuming the pf health is ok) on the other hand is unchanged. The pf might lower their interest for the pf, but your capital is still intact. Of course if you’re young this safety doesn’t really matter, but unfortunately the pf consists of young & older people.

There are definitely some pf that have a better performance than others. But focusing on performance isn’t everything. For example UBS was in the news recently because its pf paid above average interest for the last two years. But interestingly their conversion rate (Umwandlungssatz) decreased significantly, from something like 5.5% to 4.5%, which probably explains their higher interest.

I see your challenges - I have a different situation but how I do it is basically that I don’t pay off the mortgage for our primary home but invest the amount into the PF. With the following benefits for me:

peace of mind in terms of safety in case I need to pay back the mortgage due to whatever reason (guaranteed 1%)

reasonable interest rates over the last 15 years (around 4% on average - therefore more than the mortgage interest rates)

short term incentive: tax deduction

Yes you could think that I would get a better return in the long run investing the money into the stock market but having a 1 Mio+ mortgage is a risk in case you lose your job or anything else happens (during a potential markets crash I don’t want to sell my ETFs with a 30% loss to pay off the mortgage)…

Pension funds have got to be the scam of the century. Not only have their built a ton of overpriced real estate to squeeze money out of the Swiss middle class via rents, they’re also using what is supposed to be “your money’” to cross-subsidize the current retirees, all while having intransparent af fees and delivering sub-inflation rates of return. You’re quite literally better off in a savings account or festgeld.

My recommendation: move abroad temporarily and get your money out of there. Invest it yourself and enjoy 2-3 times the returns for 1/10th the fees.

Well… that is a very shortsighted view. Just compare the last couple of years with the zero interest / negative interest rates. Finding a savings account or festgeld option paying 1% was impossible… and during that time my PF provided between 6 and 10% of interest…

So you got lucky and happen to have a PK like UBS. Which is another point I forgot, PK are private institutions that are supposedly in competition, only with the small caveat that the customer has no say in the matter and cannot freely choose the best one.

Fully agree - and there is huge differences between all those institutions… and if one changes a job the PF is something that only a few check… but I’m convinced it is quite an important aspect of the overall compensation. There is so many differences in contributions by the employer, the insured salary, the rules for withdrawal, the way how the money is invested… it is basically not possible for someone not knowledgeable to really make a comparison of the PFs…

That’s on the employer side though, as the PF doesn’t decide those parameters. But I agree that the differences are huge.

Something that hasn’t been mentionned yet is the amount of retirees compared to the amount of contributors in a PF. The more they need to pay out, the less risk they can take with their asset allocation.

I think your statement is a bit harsh. Looking at new large property developments, often, pf are involved. Considering there is a lack of available flats in CH, I don’t really see anyone else trying to build more to somewhat address this problem (still not enough construction going on). Every pf should have an income statement where you can see what expenses are incurred, so fees are usually transparent. Average returns have also been far higher than inflation. UBS (for its pf clients) reports returns of between 60 to 75% (depending on size) from 2006 onwards, Swisscanto reports an average return of 3.6% over the last 10 years. While there is no indication how high the interest was on employees pf assets, the past performance would suggest that interest was easily over the minimum interest, most likely significantly higher. I don’t think you would have achieved anything even remotely similar with savings account and festgeld over a similar period.

Fees are usually not problems of a pf, they are usually quite low (<0.5%). Of course you could manage your pension yourself, but frankly, most of the population don’t know how to invest. Imagine 50% of people keeping their pf in a savings account. Therefore, it makes sense to pool and invest on behalf of the employees. Furthermore, moving abroad might mean significant taxes on your pension. Additionally, if the market happens to crash and / or stay down for longer, you have much less safety managing on your own compared to a pf.

You can get elected to the employees representative board. Unlikely that you can change the whole investment strategy, but you can definitely voice your opinion & can talk to the decision makers of the pf.

Definitely. I would always inquire about the pf of a company when applying for a new job. If it would look extremely bad (returns, interest, health), it would be a reason to decline the position IMO. A promising sign of a pf is when contributors > retirees = cashflow is positive.

Maybe that would be a great reform. Have pension funds be just asset managers and you keep your own pot of money and allocate that money to different PFs to manage.

To handle the redistribution function, you could just had a ‘tax’ and redistribute function on top.

I don’t have any real estate now but I know that you can use the same strategy you use paying the mortgae on your PF but on a pillar 3, am I correct ?

It’s called “indirect amoritzation” and it allows you to pay only interest while the payoff is invested but put in guarentee … another advantage is that your dept keeps being high so you can deduce it from taxes.

But of course, pf may be even safer than real estate and it’s great to have yield, even if it’s 2% on a mortgage payoff.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.