Well that would be a pretty major tax loophole if you were allowed to do this, no?

You could have shoven all the high yielding stocks onto your son’s balance, over which you have PoA, let him pay the tax on dividends instead of you, the taxed to death parent. Oh wait but he’s a minor and doesn’t have any other income, doesn’t have to pay any taxes. Profit!

Reviving this thread, I am also looking for a place where I could contribute to an ETF for my niece and nephew. I have started a UBS account with the UBS 100 Index Fund (the only one resembling an index fund available at the time for this fund savings account), with a small amount of money for my 10-year old nephew a couple of years ago. The annual fees were much lower than for regular fund investing accounts, and money, even small amounts, could be added at any time. Nevertheless, the fund choices and the TER on it are not ideal. Now is the time to do the same for my niece. Is there a better/lower cost option available in Switzerland in the mean time? It would be important that small amounts, maybe CHF100 could be added at the time, so there should be ideally no cost for adding funds.

With a so small amount, there is no cheap solution.

I would simply invest this money in the brokerage account you use, and sell the share and wire the amount when your kids are 18 years old.

Yep invest in a brokerage account with low fees like Degiro. I find UBS extremely expensive as a broker, and the UBS 100 Index Fund has a high TER for what it does.

When you reach 500 CHF in cash, invest in a few shares from an ETF with a low TER like SCHD/SPHD if you target US market, CHDVD for CH market, TLT for US bonds, etc. Try to average down your mean price by adding more shares when the market is doing pullback, this is where low transaction costs are handy and UBS is definitely a no-go for this. If you are not interested in dividends, you’ll easily find an equivalent ETF that performs accumulation instead of distribution.

As you have a long horizon, you may be interested in investing in children/teenagers stocks like Disney, Nike, Starbucks and issuing some fake “stock” certificates with their names, such as this one for Disney.

Thanks for all the info above. We have a 3month old that I would like to start putting money aside for.

I was thinking of doing the following:

Postfinance eSavings account in his name for cash from friends/family

Buying VT ETF for him and keep it in my IB account (we are invested in VXUS and VTI so that would keep his funds nicely seperated from our investments). We would start him off with a lump sum and then add regular amounts.

We have the added complication that most of the family money will be in GBP but we will keep the UK cash and transfer the equivalent CHF into his postfinance. Has anyone done anything similar or would do something different from the above?

I personally treat my own total investments as my (early) retirement fund + estate for my son (if he’ll deserve it). I don’t exactly see the point of splitting these two.

To all those who have one family account to invest for their kids:

How do you keep track of what belongs to whom? Is there the possibility to have multiple portfolios? I’m imagining Porfolios: “Kid A”, “Kid B”, “Retirement”, … how do you solve this practically?

We transfer 200 CHF per kid per month to their own bank accounts and then invest it in June and Dec. i keep track of all purchases for the kids in xls (name of fund, # of shares added and buy price). Then i also enter that data into a Yahoo Finance portfolio for each child in order to track performance separately. I would be keen to know of any better online portfolio trackers as i’ve been using Yahoo Finance for years and probably something is better.

You should consider changing to Google Sheets together with the function googlefinance(VT) or similar.

You cud then prob ditch Excel and Yahoo.

There’s probably templates around, but it’s easy (and more flexible) to do one yourself.

Geez, all that nonsense for what? Barring bankruptcy case, for most practical purposes their wealth *is* your wealth until they’re 18 and gifts to kids are tax free in most of Switzerland. Ergo, maximizing your personal wealth is equivalent to maximizing what you leave them…

My parents did something similar (but they did not invest the money and instead put it on a bank account). Last year I cashed that in and put it into my IB portfolio. Now 15000EUR are nice but hardly life changing. So I will probably not do the same for my kids.

I think the best thing you can do for your kids financially is teach them the way of acquiring “marketable” skills and not let them study some random thing because they do not know what to do after school.

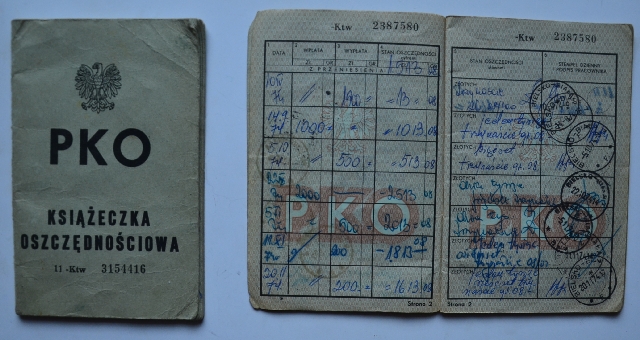

When I was born, my grandma opened a “savings booklet” at the bank, and then, annually, they put down the interest in this booklet. We had this hyperinflation in the early 90s and after many years, this money was worth something like 30 CHF. A lot of trouble for nothing It looked something like this:

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.