No, but I want to have an overview and do my day-dreaming calculations with my own numbers. When I got some coins on behalf of new-borns, I also started their own piggy bank instead of putting it in my purse. Why would I mix it up?

Well, the piggy bank was actually handed over and is starting to have educational value for the oldest. Maybe the accounts will have in some 10 years or more, as well, but I’d rather not involve them too early.

But the learning part is a different topic. To educate a teenager, I’d likely start something new, maybe similar to what Your_Full_Name describes.

beginning of the year i opened 2 viac invest portfolios for my 2 kids (5 & 8 years old) )where i plan to pay in quarterly until they are 20. (in the end i will have paid in around 8k CHF per child)

I want to do a year end review with both of them every year so they learn about “their” investments.

The portfolios are in my name.

I did not yet disclose to the kids when they will get full control over the portfolio.

I think there are a couple of issues with having investment in Kids names:

You can’t really access them when needed. I know of cases where parent wanted to use it for child’s education but couldn’t

Parents don’t want kids to have access to it at 18 when maybe they are still too immature not to blow it all on a motorbike

Personally, I’d like to wait until my kids have worked a few years and demonstrated some financial maturity and discipline before giving them money.

I’ve seen a case what giving young adults too much money too early can do and what bailing them financially can do. It ended up being very bad for them. Worse than had they been given no money at all.

The disadvantage of an account in the child’s name is that the money belongs to them when they turn 18, even if they are not yet ready for it. I can’t imagine anything worse than having to give my child power of attorney over his account at the age of 18 if he is addicted to drugs or has other problems. But that’s a worst-case scenario. On the other hand, I can understand why your parents want that. That way, they can be sure that the money will be used by your children.

Otherwise, TrueWealth makes a solid impression on me.

A way around it is opening the accounts for kids, get power of attorney for yourself, and transfer everything to you after the French leg of the gifting process is concluded. You may want to make sure you can gift your children the amount/stocks taxfree in a few years.

I once safeguarded a substantial stock gift from grandparents for my son until I felt he is mature enough for it (exactly @markus654 rationale). Tax canton ZH didn’t even want to see any gift declaration to child and IB transferred stock from my account to his account based on my verbal declaration without any issues (change of beneficial owner usually triggers money laundering warnings).

I’m pretty sure that this should not be possible without the bank’s negligence? The whole point of having assets in child’s name is indeed the fact that banks and courts should enforce the fact that the parent/guardian spends the money only in the interest of the child and not their own. Allowing to simply transfer funds from child’s account to parent’s one would obviously defeat this purpose as it loses all control over how they are spent.

On top of feasibility sounds highly unethical FWIW. If the grandparents insist on having the money donated to children directly - then it should be like that. But of course it might be worth to just try to convince them to donate the money to OP directly, then it solves a bunch of issues

Agreed. If I remember correctly, it was the “notaire” who advised about the proper way of opening accounts. I assumed that a legal(ese) reason was the basis for this and not ethical considerations.

Yes indeed, it was up to us (the grand parents do not care), it would be under IBKR sub accounts.

Anyway, I think TrueWealth is for now the best option as it will be legally under their name, but still possible to invest the monney better than the 0.XX% interests on any bank savings accounts.

Thanks for your help !

Far to be an expert. For my kids, we use Finpension with a long-term investment strategy. Both my wife and myself have an individual accounts: we both have a portfolio we dedicate for kids. Altough my wife currently does not work, the 2 accounts are in parity: whenever I put something, it goes equal into both savings. Same costs to operate, bit more of safe for kids as the accounts are under our names.

As often, I completely overanalyze topics like this and spend countless hours on it.

Having read everything with the eye on setting something up for our upcoming firstborn, I concluded tentatively on the following set up.

Open an IBKR account (I personally bank at UBS) in my name but 100% dedicated for our child. It’s low cost, we can invest in ETF’s, and purpose is to have any relatively large gifts (>25 CHF) go here. My wife and I retain control over it so we can decide whether 18 is the right age to transfer it or not. Intention would be to be transparent with our child that we’re investing for him and include him in the process of decisions once he’s at a good age.

Additionally, open a postfinance childrens account in the childs name for smaller gifts (<25chf) and keep that cash there to build a pot which the child can use for pocket money, buying stuff, etc. - i.e. retail banking. Again, low cost.

Both my wife and I intend to make a sizeable donation to the IBKR account every month (not sure what that amount would be, I’ll just make something up - e.g. 250 CHF by each of us each month). I suspect the childs grandparents will typically make smaller gifts but I could imagine during the first 12 years or so moving any sum in postfinance >500 CHF to the IBKR account to add investments.

Does this make sense by addressing both objectives and mitigating key concerns or is this overengineered?

One account in the kids name is (speaking just for me) to teach ownership (budget management) and provide a retail banking service which everybody needs eventually

One account in parents name (focused on investing) is to teach delayed gratification / compounding… lessons also valuable in other parts of life (education, sports, etc.)

My over-analyzing follows very similar patterns, with similar outcomes:

A IBKR account (sub-account of my own) receives a standing order from both of us, and will get converted into VT whenever there is > CHF 600 or so, just to make sure the minimum fees (commissions ~0.5 USD, fx conversion ~2.5 USD) don’t exceed 0.5% or so, could be adjusted.

we found that monthly CHF 200 should convert into something like 70k by the age of 18 which should be a solid base for whatever little nugget would want to do with it. studying, traveling, opening some shop, continue saving,…

account is in my name, i have full control, and also plan to use it for educational purpose

checkings account is not yet planned for, but will probably look similar

I’d say no, it’s more like the expected result for the problem statement at hand

Sleeping over it, I’ve taken a step back and decided to simplify this further:

Still, set up a basic account on Postfinance for the kids retail banking and to receive any $ gifts (incl. from me and my wife)

But rather than setting up an IBKR account, just create an investment portfolio (under my name) with Finpension where I already have my Freizugigkeitskonto. This means one less business I need to work with and I’ve come to like the simplicity of Finpension.

Until the kid is in his teens and with higher spending ‘needs’, the approach will be to transfer anything above 500 CHF on the retail account to the Finpension investment account. Given the long time horizon (18+ years), I’ll be taking a bit more of an aggressive growth allocation of ETF’s - haven’t concluded on what exactly yet but e.g.

5% Bitcoin

25% Nasdaq

25% S&P500

25% broad Europe

25% Swiss (CHF denominated)

Given he’ll inherit all of my wife and my assets long term anyway (e.g. house, almost entirely paid off by then), he’ll not have any material needs anyway but still we believe it’s good if he has an amount when he’s around 20 to either invest in education or do a world trip or as downpayment for a house. Also, it’ll be good for him to see there the benefit of investing / compounding beyond just consuming. Wish I’d have gotten a bit (read: a lot) more of that education when I was younger instead of having to figure all that out just by myself.

A friend of mine has dedicated assets (mostly CH dividend stocks) for his three primary school kids. Sharing with them is his way of teaching them about money and dividends.

I think if you feel comfortable in this topic, there is nothing good or bad about teaching your kids at an early age. Since they are your own kids, you most likely also have a good feeling about how to do it age and kids appropriate.

I can’t find the link, but I think I"ve already said it here.

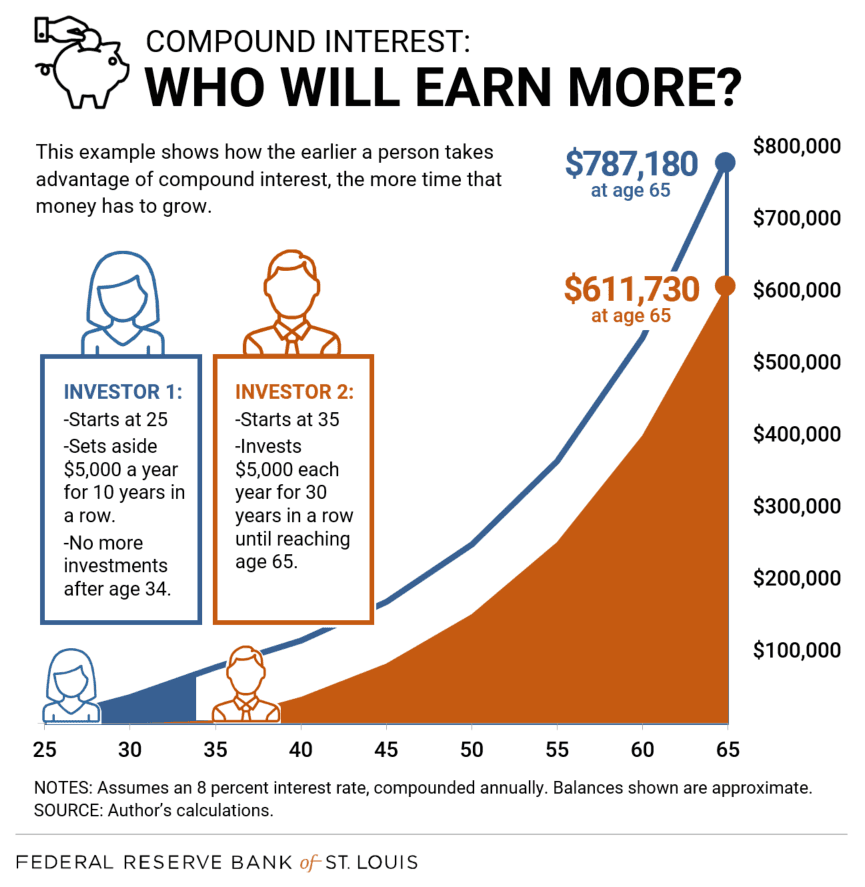

If you invest 12k at the age of 0, when he/she will be 65, there will be a very nice pension of 800k-1m chf. So maybe it’s a good idea to start with a big amount a make tiny additions? But then again this is for the pension and not for anything else.

This was eye-opening for me, not for the final numbers (though those do count too) but for how much more work does investor 2 do than investor 1, to ultimately get a worse result. Still I am unclear in myself about whether it’s better to have a separate account out of my reach for my children vs just doing the best I can for me now, knowing that eventually they’ll inherit it.

Still coming back to Phil’s point earlier in the thread, that getting a big lump sum when your life is already well set up doesn’t do a lot for you, while it could do much earlier - if you (or the child) are knowledgeable enough not to piss it away in a year.

That said, while I wish I’d been taught about investing and compounding much earlier, and not finding out about it myself in age of 35+, I also have a reservation about leading my kids to be super focused on money as I don’t want them to develop an unhealthy relationship with it and miss out on life for the benefit of a number on a screen.

There is a free iOS app called "compound interest calculator " i installed just to explain and show to my son the power of compounding. You can play with interest rate, duration, starting capital, etc and see the graphs change.

He got it immediately and became curious about investing. My objective was achieved

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.