Hi, this is an amazing forum, so much information. I have been browsing, albeit I have to say I don’t understand so much, so thought I would just ask my questions and see where that takes me: I am 60 and living in canton Zurich and I’m about to retire (basically getting pushed out at his stage). I have a pot of CHF3m (mainly pillar 2). I would like to take the capital, and invest it and try and live off the income and leave the capital to my kids. I have some questions:

• If I take the capital rather than a pension, is there a large withdrawal tax (I heard so, seems so from reading the posts here, but I don’t really understand it all)

• What do people typically invest in – I would need a swiss income so am thinking swiss dividend paying stocks, I assume through an ETF (I have no clue about this stuff other than what I read here, but guess I can do some study…). What type of return does something like this offer?

• Is it possible to leverage something like this up a little to try and leverage my returns

• What about property, is that a realistic option…I was thinking with CHF3m I could probably leverage that up if I invested in a few apartments.

• I would like to keep it simple as I don’t fancy myself being able to get too into this subject.

• I can take some volatility, especially as I would like to leave this for my kids (who are totally financially illiterate!), as they will have a very long term horizon. I assume that there is less volatility in dividend paying stocks in there is diversification in the mix.

Anyway, I’m just wondering if I’m missing something, maybe there are some off the shelf solutions as I can’t be the only one retiring!

Buddy, honestly, you’re a little late in seeking advice. Nevertheless …

Given your portfolio size, seek out a professional independant advisor. Google them, DM me for a suggestion.

Definitely withdraw the capital (instead of a pension), but educate yourself on how to best invest (see point 1). If you can’t educate yourself on how to best invest, just withdraw the pension.

No further advice given your description of things.

Dividends aren’t magic or result in higher income from a portfolio. There is a misconception, especially in Switzerland where dividends are the only thing that get taxed in a stock portfolio.

As your investing experience and knowledge is rather limited and you wrote that “don’t fancy myself being able to get too into this subject” I would strongly advise you to seek help from an independent financial advisor that solely works fee-based (so not working for a bank).

As suggested by the others, I would seek independent professional advice to help plan your retirement.

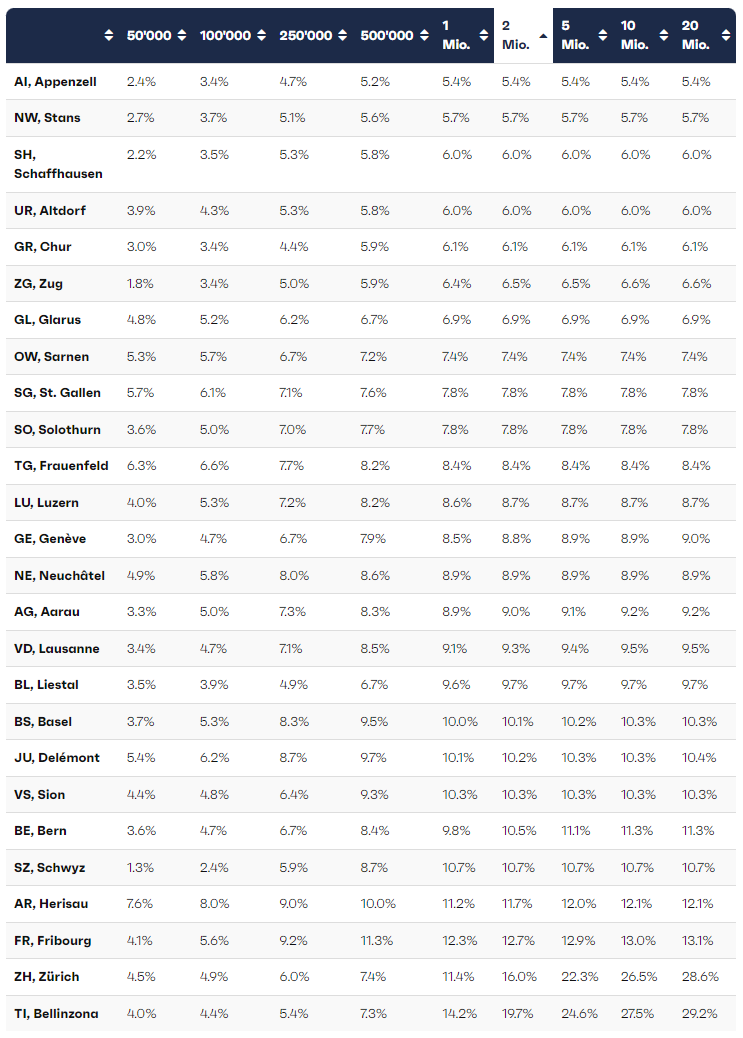

As an example, withdrawing a 3M pillar 2 in Zürich would generate something like 500K+ taxes. There are options to reduce that. One of them is to take part of it as a pension as suggested by @PhilMongoose, a good advisor may help you further.

I would then come back here to double-check your plan before enacting it. As is, I think more personalized advice, taking into account your personal situation, would bring more value than what we can bring here.

Edit: the off the shelf solution is to take the entire pillar 2 as a pension. It was probably not designed with a focus on people with your amount of assets, hence why a slightly less off the shelf solution might be preferable in your situation.

One late addition, though you definitely need a financial advisor to make sure things check out from a tax authorities view:

Quit before reaching the official retirement age, split your pillar 2 probably equal sized into two Freizügigkeitsdepots, remain unemployed, withdraw one Freizügigkeitsdepot when you can, and the other one in a different year.

There’s limits around how you can do this, and the tax authority will notice and will add the two withdrawals into one with the progressive tax applied if you’re not within the limits.

You might get even sufficient advice about it from your bank financial advisor (their job is ususally to sell you the bank’s awesome financial investment products, especially for your phase in life … ), but perhaps you hit someone knowledgable?

Personally, I’d spend high three to low four figures to get solid advice on whether this can still done in your case to get waterproof advice for potentially saving six figures in taxes.

Majority of 3M in Pension means that you earn 200k plus. Minimal savings beyond Pension means that you both have cost of living in the range of 150k plus, that you didn’t yet learn how to save yet nor how to invest.

So you want to draw 150k from 3M and you dont know how to manage money. Dont do it as you don‘t want to end up as a financial burden to your kids.

Well invested 3M will generate you safe 120k p.a. You would first lose a few 100k in taxes - and you will then lose more as you need to first learn how to invest. Conclusion: you will run out of money; probably in 15-20 years max.

Assuming your pension had a conversion rate of 4.5%; you would make about 135k. That may still be a stretch but the fact that you don‘t get more pension will allow you to learn how to safe. Don‘t take the cash.

And as others said, take advice to a professional in order to make your mind. A lot of member recommend VZ for instance. Once you can figure out what you want and need, it will be easier.

My father asks me if it was better to take the capital or the pension. I said that if I was him with my knowledge I would take the capital. But as he doesn’t have any education in investment and only manage to save some money in his saving account, I advise him to take the pension for peace of mind and use his saving if needed (spoiler he doesn’t need it and he still manage to save money with his pension, what a true Mustachian he is without knowing it ).

can mean anywhere from “relative” to “absolute” majority w.r.t. other assets.

(Even 50-60% could not be too bad/surprising with a longer career and generous fund / buy-ins)

So making such bold assumptions might be a bit rushed.

Let’s wait for more details (although the OP has been silent until now).

Correct @dbu we lack critical information. If he has a fully paid-off house, the situation looks different. On the pension vs. Capital decision - the principle is quite simple: in case of doubt, take the pension. What I see doesnt make much sense (3M, majority in Pension). Hence I strongly advice for the pension - unless the situation becomes more clear.

Should OP eventually decide to go this way, here is a really good blog post on staggered withdrawals. Read the comments too

Wealth tax and AVS are payable on advance withdrawals that can add up ~1% p.a. depending on the canton, this partially off-sets any withdrawal tax saved

Hi, thanks very much everyone, great advice. My takeaway: I need to go see a financial advisor!

To fill in some gaps: -

Yes, my salary has been about CHF 200k pa.

In addition I had a bonus of about 50k, which I always put into my pillar 2. That’s basically where my pot came from.

Priority for me is to preserve my capital for my kids.

Thus, I would like to live of the earnings I can generate on the CHF3m. If I got CHF 120k (4% pa) that would be plenty for me. If I can generate more, reasonable safely, even better.

Happy to answer any questions/fill in any gaps. If anyone can recommend an independent financial advisor to me, that would be nice.

To me, that means making sure that your expenses are covered (so that your capital doesn’t get depleted by it and your kids won’t have to step in to potentially support you financially), then that the rest of the capital is invested according to your kids’ circumstances.

Relying on the 4% rule for capital preservation is risky: success in that framework is considered as not running out of money after 30 years of drawing the funds out. 1 remaining cent qualifies as success (on the other side of the coin, most scenarios would allow for a very big accretion, the variability of the final amounts after 30 years is pretty wild).

I would see two viable scenarios:

covering your income needs with:

1.1. OASI

1.2. pension from your 2nd pillar

1.3. dividends and interest from your remaining invested capital

moving to another place with lower taxation, quit your job, set 2 vested benefit accounts, and withdraw all of the 2nd pillar in a staggered way. Tax offices have discretion with regards to considering that tax avoidance or not, and to allow for the lower taxations or to tax it all as a single withdrawal, potentially at the Zürich rates. Consulting a tax and retirement planning specialist is highly recommended before trying to do any of this.@anon17469660 volunteered to provide a recommendation if reached by PM, I would take him on on this.

In order to better understand your situation for option 1), could you tell us:

that your target expense number is 100k CHF/year, after tax (or if not, correct that number).

if you are expecting to get OASI as a married couple or as a single individual and if you expect to get the max pension (44 years of contribution, 3’880’800 CHF cumulated eligible salary during that time (mean of 88’200.-/year)?

what the conversion rate of your 2nd pillar is (converting capital into pension)?

reiterating Barto’s question, how much of the 3m pot is in pillar 2?

But withdrawing 100k from a 3M portfolio would generate around 17.5k income+wealth tax in Zürich, so only 82.5K could be actually spent. You’d need an income of around 120k to get 100k after tax, and since the 2nd pillar would be taxed when withdrawn, not the whole 3M would be available to generate returns.

The situation would be better in another, lower tax canton/town but even then, taxation can’t be brushed away with those numbers.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.