Yesterday I spoke to colleague about inflation and I was surprised: In the last 10 years my fixed costs of living in ZH have been reduced by about 500 CHF a month by a deflationary environment and low interest rates: the reductions in rent and TV/phone/Internet have outweighted increases in health care and public transportation expenses by a lot. But what happens when the interest rate for rents (Referenzzinsatz) increases from 1,25% to 7%?

The current Referenzzinsatz:

And how to calculate the changes in rent (it only goes up to 4%):

That’s a nightmare. How can i protect against that? Are there any financial instruments?

As @nabalzbhf said as long as you’re employed you should be fine.

Otherwise owning your primary residence should be pretty effective as a hedge against rent risk, but depending on your situation and life plan it can also have a lot of drawbacks (there’re a lot of discussions about this in the forum).

Now that I think about it, I wonder if investing in real estate funds could also be considered a form of hedging against rent fluctuations…I guess for this to work they have to own residential property in your region. But maybe I’m missing something…

Thanks for your replies. I agree, as an employee salaries should increase with inflation. But look at the table “Überwälzungssätze”, if we get to interest rates of 4% (assumption 3% inflation, which is not much), rents increase by about 33%. My salary is certainly not going to increase by that much. My assumption is that politics would intervene, but still I am looking for an inflation hedge.

I don’t think anyone is expecting that anytime soon. 2% is a typical target for central banks.

(also housing prices would likely crash if that happens, which should also influence market rates)

As @nabalzbhf puts it, an interest rates increase is likely to be spread on several years. It would potentially affect homeowners (mortgages, price of house), lenders (rent increase) and pension funds (price of house). The SNB would be careful with that.

As for inflation edges, stocks are usually considered a good one. Gold can be considered, as well as real assets like real estate. That one will react differently to inflation and interest rates raises so its usefulness would depend on what scenario you are trying to ward off.

If rent is your real worry, owning your own home without too high of a mortgage (and ideally no mortgage at all) would be the perfect solution. It’s probably not the most financially efficient one but it would ward you against that specific risk.

Actually it’s usually one of the main reason why owning a home for retirement (when out of workforce) can make sense (and why some government encourage home ownership as a result)

I agree that owning a home can help, but I am not really into real estate as an investment. I think Switzerland is unique in its interest rate risk (rents are linked to interest rates (what other country has that?), the general indebtedness of population, etc.) There has to be a financial instrument to protect against that. Stocks are not too bad.

If the purpose is to protect you from rent fluctuations you shouldn’t look at it just as an investment, it would be an hedge against rent increase.

Home ownership is the ideal solution, the closest financial instruments are real estate funds: most of their earnings should come from interest-rate-linked rents as well.

So in the (unlikely) event of skyrocketing interest rates I suppose that the earnings of the funds should increase with them and you should be able to use their dividends to pay off your own rent increase.

I would say in an environment of rising interest rates real estate values will go down. If you own a property and rent it out, you in all likelihood will be able to raise the rent in line with inflation, but the value of the property will go down. It’s not easy to find a hedge against inflation and rising interest rates, but for us in Switzerland it’s really important. There have to be financial products for that.

On the inflation side, afaik the Swiss government doesn’t emit inflation-linked bonds (why would they? they can easily issue debt with negative interests) so there are no easy solutions.

There’re some funds which try to synthetycally recreate inflation-linked Swiss bonds, but they’re not very good at it (see example from credit suisse )

Gold and probably commodities. Maybe cryptocurrencies but they’re too volatile to really allow to plan on their ability to maintain value in a given scenario.

In such a scenario, goods become more expensive, so you want to own goods. Real estate is kind of its own beast, being negatively affected by raising interest rates but productive land and maybe commercial real estate could have an edge.

Raising interest rates make debt more expensive and raise bonds attractiveness, potentially at the expense of stocks and gold. There again, real assets should have an edge provided they’re not subject to high leverage (hence only a low mortgage, if any, on the real estate).

Basically, at that point, I’d want to invest in the real economy. Owning a successful business venture would be the real money printer in that scenario if you ask me.

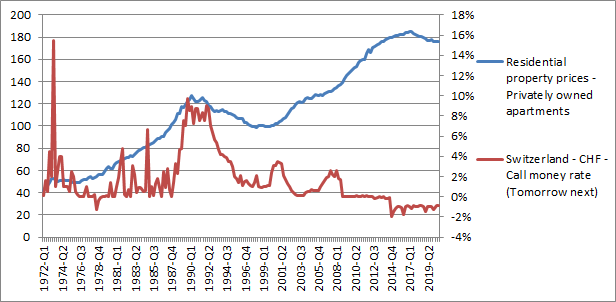

The real estate drop in the 90s started with stable interest rates (at almost 8% )

Now real estate has stopped growing again while the interest rates are well below zero…go figure

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.