There was a 12-year long period between 2000 and 2012 where the s&p500 / dow jones didn’t increase

How does one prepare for such a crash happening again? If it’s the same as then, it means stock portfolio almost halving in value, and staying like that for 12 years (with a few ups and downs but not reaching the original value for that long)

How can one hedge against that, when trying to live purely off this portfolio, no additional income?

The ideal solution would be to increase your cash part now to be able to DCA into the weakness later. But you gotta live off of your portfolio. Hmm, tough situation, especially if your nest egg is small enough that a 50% market downturn could destroy your retirement cash plan.

a. How about finding a job that helps to pay for some of your cost of living during the market down-turn?

b. Using a lombard loan to leverage yourself out of the market crash would probably be too risky.

c. moving abroad to a place with lower cost of living expenses.

d. reducing your spend while living in Switzerland (e.g. going lean fire)

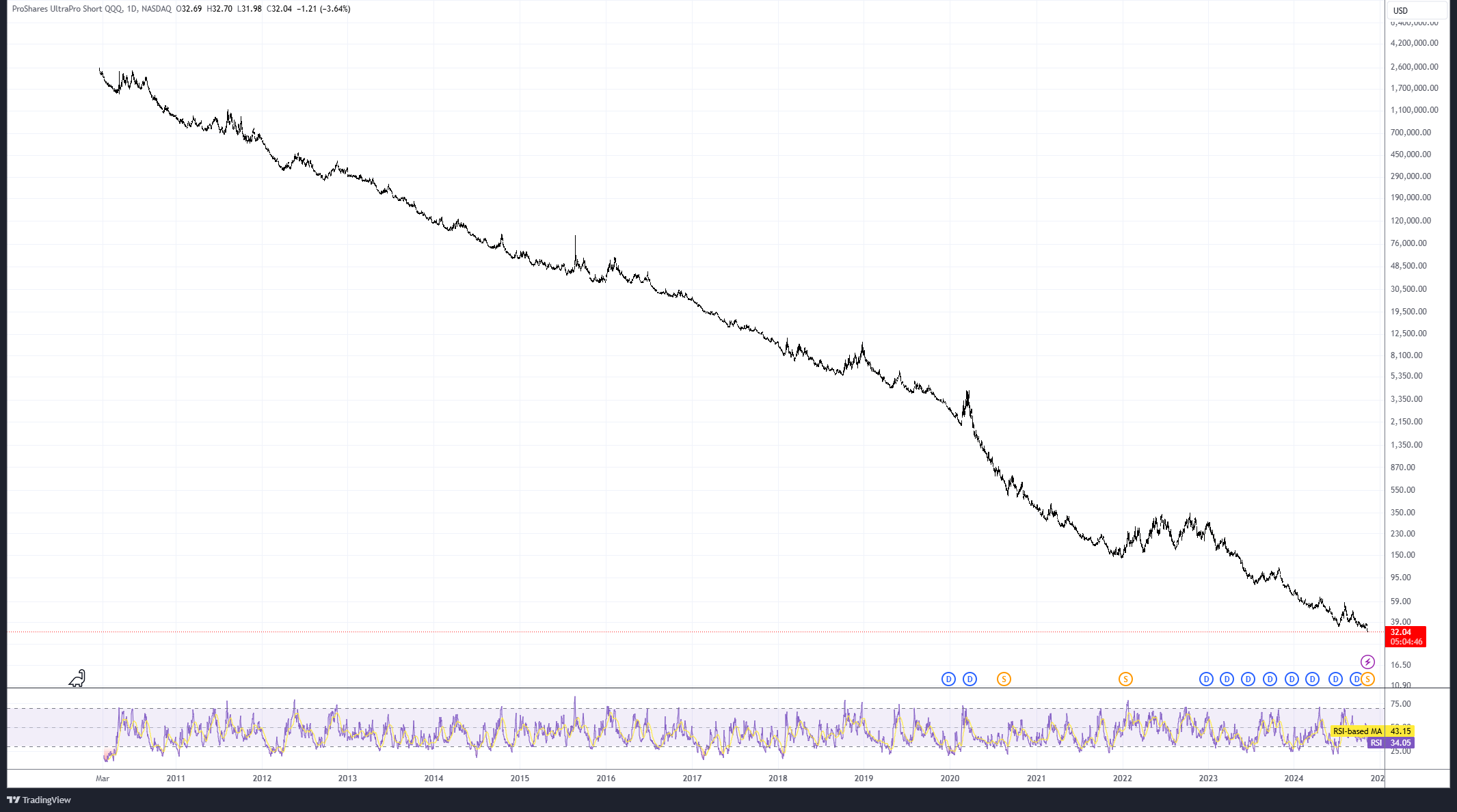

e. going short with an ETF (maybe even with a 3x lever) like SQQQ

Increase the fixed income allocation.

Add diversifiers like real estate, gold, bitcoin

Or use funds which create more income like with call option writing

That’s actually 13 years (or, well, 1812/3 years), since you’re nitpicking to evaluate performance from Jan 1 200(0 )to Dec 31 2012, but I believe the OP meant to ask how to survive a decade of declining index performance.

At any rate, I’ll stay with my previous recommendation, although I cannot deny the appeal of your own recommendation of keeping a low withdrawal rate.

Edit: a 24% return in USD between 2000 and 2012 equals a CAGR of about 1.7%.

I try to do both. My equities core holding is Fundsmith which is a Quality strategy: companies that have “already won” with high ROCE which means it avoids “speculative tech companies”, car makers, banks.

It doesn’t own Nvidia yet. Therefore I am missing out on some of the market upswing right now and Fundsmith is still below its Dec 2021 ATH in CHF terms. I am about to RE so the strategy makes sense for me since I think it takes some of the downside off the table for whenever the crash eventually hits

My point was that the S&P500 index doesn’t capture dividends. But I agree that even including dividends it was a crappy 12 or 13 years if you owned the index including Cisco and all the rest which had speculative valuations in 2000.

If you are only doing withdrawals on a portfolio with no additional income. In this case you would want to be well diversified in uncorrelated assets (Basically don’t allocate 100% to stocks)

See here for some discussion on Ray Dalio’s All-Weather / All-Season Portfolio. These types of portfolios are really not good if you are still in the accumulation phase (where you actually should be welcoming stock crashes).

FYI - This would be a terrible hedge. Especially during a long duration market crash. This is a derivative product, it’s meant as a trading vehicle for very short term trading. You would lose money even if the market went down (slowly). Take a look at the long term chart of it and you’ll see that even if the COVID drop propped the price 100% in that period, you are still worse off for having held it through even a small number of years.

The timing would be at the center of these suggested two options, no?

When do you change your asset allocation in order to hedge?

You would have to hedge before things turn south, i.e. sometime before the dot-com bubble pops, maybe 1999, earlier, a little later? … giving up those juicy returns in the last year or two or three or even just a couple of months before the market hits the top.

Hard to time, at least in my book, before that lost decade or so starts …

… unless your asset allocation is already such that you don’t hold the market – which kind of by definition benefits from the bubble until it pops – in the span of years to days before said bubble pops.

So, yeah, hedge you must, if you want to avoid the OP’s dilemma, but how and especially when is still everyone’s best guess (you’ve offered a general suggestion on how, I’ll give you that).

My answer on when: ideally at any point in time.*

My answer on how: you guessed it, I’ll refer to my previous answer.

* I was going to add the qualifier that maybe you can avoid hedging if everyone’s outlook looks super rosy, but then again there are exonogous events and even non-exonogous events (like the pricing of sub-prime mortgages in the GFC) that can royally screw up your and your best macro friends’ forecasts.

So maybe, just always be prepared? It’s what I aim to be pursuing, while still aspiring to capture something similar to a market return.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.