Yes I did and it is currently active (I did it to save taxes and also have some safer investments).

Exactly, there is no insurance so there is about CHF 1’000 fees during the first year (opening contract, etc) and pretty low during the next years.

The investment is following the portfolio of the Rentes Genevoises, which yields about 8% per year on average, they told me.

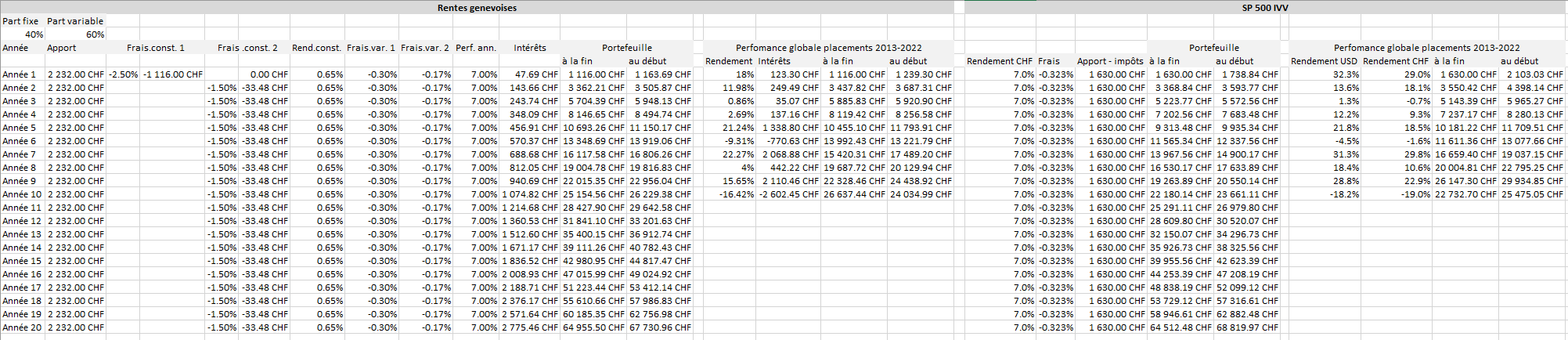

The return on the equity portfolio is shown on the Rentes Genevoises website between 2011 and 2022. After calculation, we obtain an average of 7%/year over this period.

I wanted to know if this was an interesting solution. To do so, I compared it to the SP500 (IVV). During this period, the CHF return was 11.7%/year.

My variables and assumptions :

Fixed portion: 60%; variable portion: 40%.

Contribution of CHF 2’232/year over 20 years

Constant Rentes Genevoises fees as indicated in my previous message.

SP500 fee of 0.323%, including TER and non-recoverable dividends (value calculated in another post)

Additional fixed taxes of CHF 600/year for the SP500 solution

Annualized performance of 7% for both solutions (Rentes Genevoises and SP500)

Conclusion: the results are roughly the same. With these assumptions, I’d say that the Rentes Genevoises solution is slightly better than investing in the SP500, as volatility is lower.

But :

If you move outside the canton of Geneva: more deductions and high exit fees (I don’t know how much).

It’s not impossible in the medium term that there will be a change in tax policy and that in future we won’t be able to deduct 3b in Geneva.

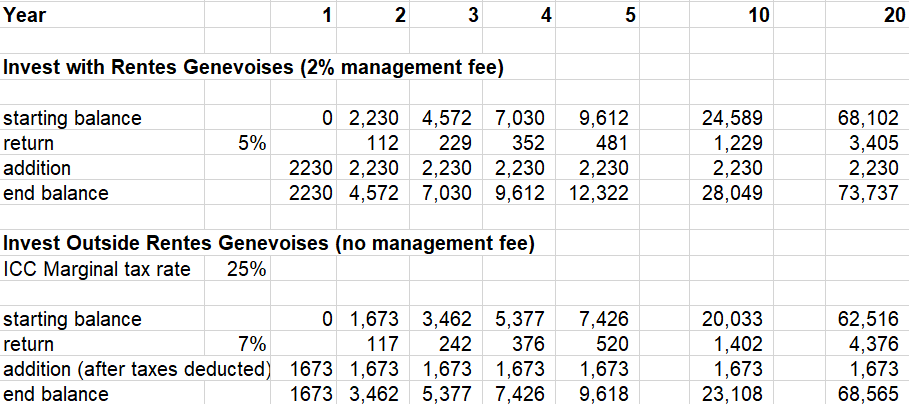

Below a quick and dirty calculation. Assumptions: 20 years contribution, 2% management fee and 25% marginal tax rate (excluding Federal taxes)

There could be a small benefit but not worth pursuing in my case. Especially since I expect to stop full time work so my marginal tax rate will decrease, it may not even pay out at all.

I think it’s before fees (it’s on their product sheet), but there’s no indication.

We can also do another calculation: assuming that the returns between the years 2013-2022 are before fees, I get a correlation coefficient of 0.95. The Rentes Genevoises equity portfolio and the SP500 are therefore highly correlated.

With 10-year historical performance and taking into account all the fees mentioned above, the SP500 is much better. Keeping the same performance ratio of 11.7% / 7%, the SP500 would have to fall below an average yield of 4.4% for the Rentes Genevoises solution to become attractive (without considering the volatility and various risks mentioned above).

You can change the assumptions as much as you like. In my case, I’d feel more comfortable without a new long-term contract.

If I understand well, interest income from savings accounts and bonds can be claimed under the same deductible as for life assurance.

We didn’t have any interest income for a few years so I didn’t pay attention until preparing our 2023 declaration yesterday

If my understanding is correct, it would be another argument for many people that counts against signing a lengthy life assurance contract (if your primary goal of taking the life assurance was the tax reduction)

The guidance says market value so pick something reasonable. Max wealth tax for the wealthy is ~0.8% so it is unlikely to be challenged unless you own a luxury car.

Anyone found an easy way to declare securities? Both GeTAX 2024 online and Windows version fails to find so basic tickers such as MSFT (they are in ICTax). Also I find it ridiculous that I need to manually enter ~90 tickers and ~200 trades (dollar cost averaging…). We have two IBKR accounts, so we have pretty nice exports of our activity plus I have programming skills. Tax advisor is not an option, as I do not trust any human doing it with proper diligance. Is Geneva really in the stone age in terms of computing?!

Yes you can declare one line for the brokerage account.

Just declare the total amount invested, dividend value in chf and wht in chf.

You do not need to declare each securities individually.

You can also deduct the annual brokerage fee up to 0,3%.

You can also import the .tax file of 2023 to speed up the declaration.

Thank you! In this case can I send a DA-1 form individually for each country and not for each asset? This is my first declaration and I did not find any programatic way I can import into GeTax 2024 or edit the .tax file

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.