From my understanding, every month when it rebalances, i will be forced to pay redemption fees, because it might sell soms of my funds. You can see for EM the redemption fee is 0.3%, which is huge.

Is it even worth to use different funds or should i just use one single fund and nothing else, so i dont have to rebalance? If so, which one? Probably the World ex CH?

The redemption fee is only applicable on the buy/sell part.

Finpension is doing an internal rebalancing, so the cost will be lower.

For exemple, if customer 1 buys and customer 2 sells. Finpension will simply transfer the ownership between the two customers without any fees.

Finpension has like 100 appstore downloads, i doubt they have so many costumers to swap around with…

Do you really believe, that they will do a decent job rebalancing? Im just scared that they gonna be selling/buying EM all the time with that huge fee, when theyre rebalancing.

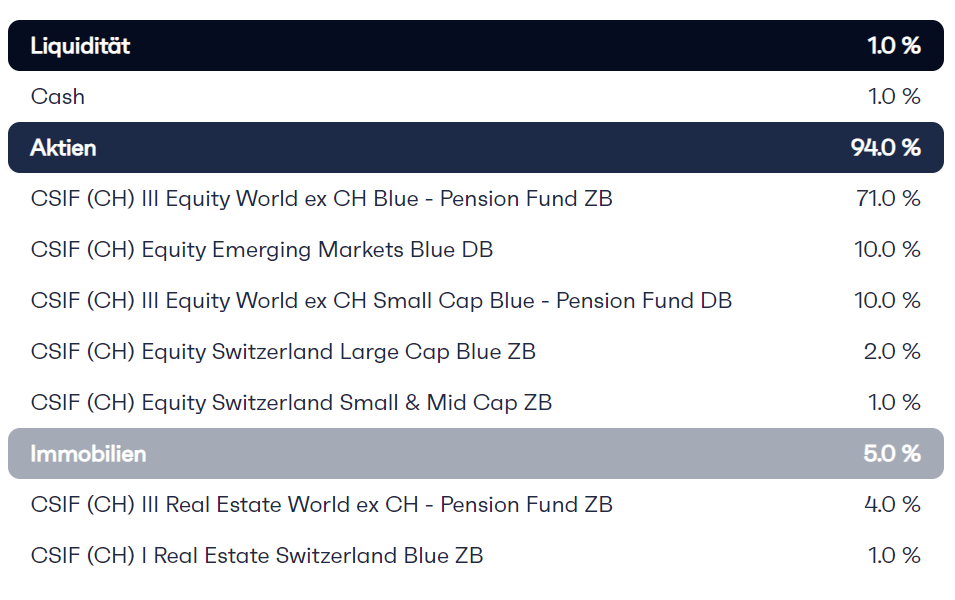

Whats your opinion on the portfolio i came up with?

Even without the internal rebalancing don‘t forget that it would only be charged on the rebalanced amount. Looking at Emerging Markets and All-World indices, the market cap of EM equities has hovered pretty constantly at around (slight above?) 10% - similarly to the US‘ share of around 55%.

So assume the share of EM in your portfolio fluctuates by about 1 percentage point each month:

That would incur costs of approximately 1/15 * 0.003 * 12 ≈ 0.24% per year.

One additional thought: In Pillar 3a, you often make continuous deposits. If you make monthly deposits, you may never need to sell any funds but just buy more or less of the individual positions. And in the unlikely event a sale is necessary, it will most likely be netted with other customers because they make more often deposits than withdrawals.

2% SMI is negligible. Won‘t make a meaningful difference.

I wouldn’t bother with anything less than 10 or at least 5 percent.

Otherwise, it‘s an All-world portfolio with a bit small caps and Emerging Markets mixed in.

Looks good, I‘d say, if you don’t want any Swiss exposure (you’re might already have it through real estate or your job)!?

If a home bias was desired, I‘d probably substitute the World small-cap fund with a Swiss mid-/small cap fund.*

World large-cap will be rather highly correlated to World small-cap.

Swiss large-cap will be rather highly correlated to World large-cap, due to globalization (that is, unless one of the big three messes up significantly).

Swiss small caps, less so.

finpension can buy fractions of funds, so I opted for an all world portfolio replicating the “Vanguard FTSE All-World” ETF (VWRL). E.g. after my first payment I own just 0.025 “CSIF (CH) Equity Emerging Markets Blue DB”.

As the Credit Suisse funds are special pension funds, they have low TER and are exempt from stamp duty as well as withholding tax. This should compensate for any eventual redemption fees.

1 Like

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.