So lets say you are on holiday abroad and to keep it simple the currency of the holiday country is EUR.

How do you do purchases on shops or lets say pay in restaurants and hotels with cards?

How do you withdraw money from ATMs ?

The idea is to have minimum fees maximum convenience.

Currently i have a normal CS account just opened a CSX(the free one) , waiting for my cards from swisscard (the cashback ones AMEX,Mastercard) and i was about to open revolut and/or Tranferwise

I have an account & Visa Pay (debit card) & Credit Card in Euros, from DKB (German Internet Bank). It’s free, and no card transaction fees in EUR-countries.

I exchange/transfer Euros from my CHF’s at a Swiss bank via Transferwise.

I have a Euro Privatkonto at Migrosbank & withdraw my Euros cash at a Migrosbank ATM. I exchange/transfer Euros from my CHF’s at a Swiss bank via Transferwise.

I try to pay everything with Revolut with pre-exchanged money (e.g. a few k USD when going to US). When possible I avoid cash otherwise I withdraw from ATM with the Revolut card too.

I pay everything with my neon card and avoid cash as much as possible. I think that 99% of time you don’t need cash to pay for something, especially with the pandemic situation

With your CSX account you have the MasterCard FX for abroad’ purchases (like neon).

Hi All many thanks for all your responses!

It gave me a great insight.

Also i tried to figure out the costs incurred of my transactions this summer in Euro and its horrifying.

500 euro plus, i was completely oblivious to it.

Which one could say its ok it happened once now you learned… nope this is the 13th summer in a row that i didnt know about it…

I will update this with my final approach that fits better my style my needs my convenience and my limitations (dont want to have a non-english service)

ok so have been trying all sorts of things in the background. first semi expensive lesson for me. →

I have created a post finance account(s) CHF,EUR,USD and trasferwise the same

So i tried yesterday the whole process i wanted USD, so i transfered CHF from post to Wise then converted in wise from CHF to USD and then transfered back to my USD postfinance account.

The result

I started with 500 CHF converted to 538.91 USD and ended up with 494.66 USD or 457 CHF ! ahaha ridiculous

I called postfinance and they hadn’t added any fees on top, Wise had quoted me a transparent 4 USD fee on the transfer and then the magic happened…

what i hadnt read and was correctly pointed out from a Wise support person was :

Your bank or other banks the money passes through on the way may also charge you a fee, so your recipient might get less. These fees tend to be around 25–50 USD, but there’s no way for us to know what they’ll be in advance.

Is it fair to assume that this transaction based and not amount based? So even if i transfered 10.000 usd i would end up with around the same fees after the money left TransferWise and before they landed in PostFinance ?

How would you guys have done it/ would do it better?

Well, I am using only EUR and CHF. EUR transfers are free in Europe. I avoid doing USD transfers exactly for this reason - you never know how much you are going to be charged.

If I would travel outside of Europe, I would rather load CHF/EUR into Revolut, convert money there to a local currency and use a credit card/withdraw cash at the destination.

Before I was also withdrawing local cash with Postfinance card, with their premium account you don’t pay a fixed fee, just their spread, whatever it is.

Hi Nik, I’m not sure if the following method might help you overcome your issue, but I do the following and it might also work for you if Postfinance allows:

Make purchases abroad using US credit card, then to pay bill:

Send CHF to Interactive Brokers account

Convert CHF to USD

Wait 3 days until I’m allowed to withdraw

Withdraw to USD account

I found this is significantly cheaper than Transferwise, since the forex is at least as good as they provide, and the fee is nominal ($1-2)

thanks Dr. Pi after this experience i was revaluating my approach to USD.

@bert Your timing is amasing ! i was actually doing this test last night comparing the two options Tranferwise Vs Interactive brokers so from last nights calculations rates

500 CHF to USD

plus fees of :

Wise

540.85

1.94

Interactive Brokers

541.5

1

Google

541.35

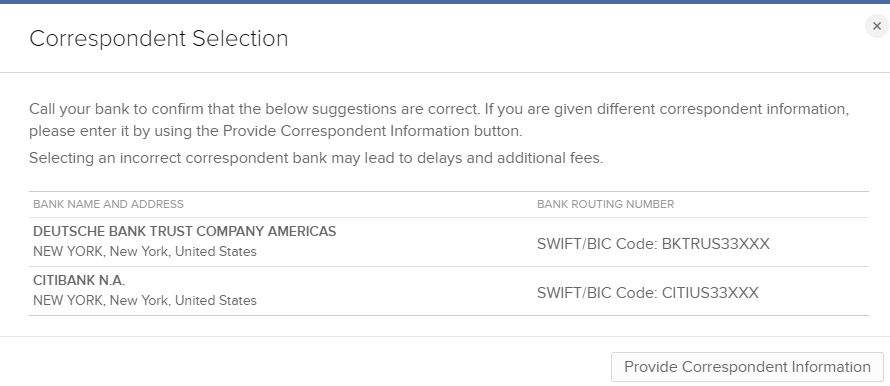

I stopped the withdrawal from IB last night because a) i didnt know how to continue i got a message asking for a correspondent bank and i had no idea what this was i had just entered my IBAN from my USD postfinance account b) i wanted to see if i get any nasty surprises from my Wise tranfer (which i did)

so if someone knows what to enter on the correspontant bank field when transfering USD to your USD postfinanace account i would be greatfull.

I called postfinance they had no clue .

I don’t recall ever doing that, maybe because I withdraw USD to a bank located in the US (also, no IBAN, SWIFT etc). Perhaps Postfinance use an intermediary to process USD-denominated transfers?

Forget about a USD account in Switzerland.

Unless the amounts you intend to transfer/hold are so large that the transaction costs (bank transfer) don’t matter.

While I don’t know if and how IBKR allows USD withdrawals to non-US bank accounts, you should realise this:

If anything, Interactive Brokers will do the same type of SWIFT transfer as (Transfer)Wise. Thus you could be charged the similar fees. Maybe a bit more, maybe a bit less, depending on banks and intermediaries involved.

Why is bert doing it so cheaply?

Exactly. IBKR sends it as a cheap (US) domestic USD payment.

A USD account PostFinance will likely not be reachable through this.

i ended up asking more as a back up plan for IB because i love plan b c d and e since my experience last night guided me towards your knowledge, the postfinance USD account isnt to be used too much by me.

So what i did when the market opened in the us i put those USD that i had ready to transfer to MS stock : )

I will stick to EUR at the moment just wanted USD for some crypto stuff.

Alrighty as i progress here i will post my choices and my mistakes for others to see and laugh or learn or both

I keep an account (actually two) in Euro for transactions in the EU. I top them of once a year or so from CH. I also keep an account in the US for $ transactions, and generally better international credit card fees.

The US account is actually free, the EU accounts cost me less than transactions fees & unfavorable exchange rates would cost me otherwise.

If your US bank offers a cash-back credit card, you might be better off using that for purchases in the EU also. I get 1.5% cash back from my US bank on every purchase. For purchases in euros, the forex spread eats up approx 0.6% of that, but there are no transaction fees, so in the end, by using the US card I actually get 0.9% cash back even on euro purchases.

Of course, this strategy depends on the bank’s Ts&Cs. For now, my bank doesn’t object to me getting hundreds of dollars a year from them in cash-back while offering them only the measly EU interchange fees and forex spread in return.

I see a lot of talk about USD and EUR but I’m going to Bulgaria this summer and they don’t use EUR.

I’m going to pay as much as possible with a credit card. For this purpose I was wondering which one would be best? I was anyway planning on opening an account with neon which seem to be pretty good on fees? I’m not sure if it is worth it to bother with Revolut and their weird week-end thing?

For cash withdrawal I think I’ll have to use my maestro, at UBS it’s 5CHF per withdrawal. Are there cheaper alternatives?

Less expensive than virtually any credit card.

But keep in mind that Neon’s cards isn’t a credit card but a prepaid/debit, when renting something (rental car, hotel room) or making payments “off the grid” (offline, without internet access).

Neon probably.

Neon charges only 1.5% for foreign withdrawals.

That’s probably better than 5 CHF + foreign currency/transaction surcharge + your bank’s actually FX rate (spread) on the Maestro card.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.