I recently moved to Switzerland. 32M, family of 4 with 2 kids at the private kita.

I can save max 1K per month for investments right now.

I have a Degiro portfolio mainly focused on VWCE. I have been converting CHF to EUR to invest there every month over the past 8y while been cross-boarder worker.

The conversation fee using WISE has been around 0.25% (I.e. less than 5 CHF for a 2K CHf to EUR conversion).

I am now looking into IBKR and VT as many Swiss investors do.

My Degiro fees are (base fiat is EUR in my Degiro):

2.5€ per year for connectivity fee

0.3% autoFX per month to convert CHF salary to EUR for investment

1€ transaction fee with Degiro

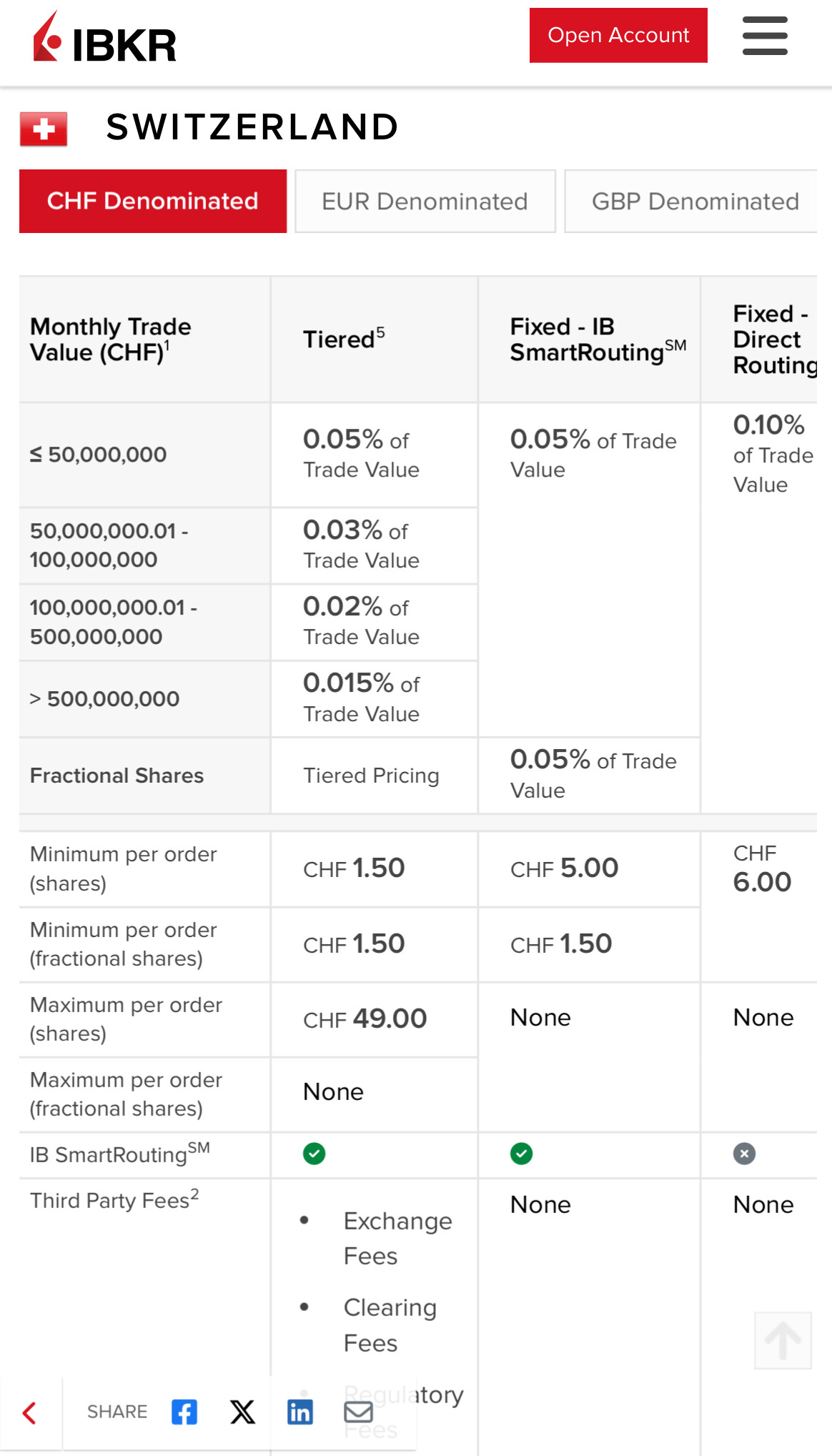

With IBKR I would be at 0.03% autoFX and then with VT 0.07% TER. Also the transaction fee will be below 1 CHF for a 1-2K investment.

My questions:

would it make sense to let my Degiro account as it is now and start investing from now on with IBKR and VT?

for the DA-1 form and the tax credit for the withheld tax on dividends from US, this is 15% right? Will IBKR be keeping automatically 15% and then I will be getting 85% of the VT dividend?

DA-1: what is the probability of not getting the full 100% refund of the withheld dividend tax?

Any other advice is appreciated. Just moved to Geneva after 10y investing while being in Europe

Probably, but there is an issue. You don’t get a DA-1 refund if the amount of taxes withheld is less than 100 CHF. So if you hold less than, say, 35k CHF in VT, you are not eligible for a DA-1 refund. So you might need to liquidate Degiro holdings and add these funds to your VT stash.

Looks like you have no mortgage, which is good. Your tax rate is decreased due to having children, which is “bad”. But taxes in Geneva are high, which is “good”. Some people were trying to figure out the formula, but I am not sure how reliable results are.

You can run the tax software with your typical numbers and see what is your average tax rate is, for a start.

P.S. there are now rather good other options with European ETFs, so you might also consider them.

I do have a mortgage of less than 80k in France though. Don’t know how this impacts things.

What do you mean when you say “better UCITS ETFs”? Like other UCITS with lower TER than VWCE?

I am really confused about whether I should continue investing in Degiro but maybe with a new Swiss Degiro account so that my fiat currency is CHF and then only invest into UCITS in CHF currency to avoid converting CHF to EUR.

Swiss brokers have to charge Swiss stamp duties, foreign brokers do not. So It’s a matter of paying stamp duties or not paying stamp duties, rather than higher or lower.

1 Like

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.