In my opinion you should overthink your decision of using SwissQuote.

I personally (as many here on the forum) use InteractiveBrokers. I was also hesitant about trusting most of my money to a non-swiss broker, but do your research.

Sorry but I’m not really following. The Federal Stamp will be applied due to the CH broker (SwissQuote, CornerTrader, etc). The Stamp Duty on foreign shares (non swiss ISIN) is 0.015%.

175’000 x 0.0015 = 262.5 CHF. This is supposed to be the same for VWRL and VWRA (both are Irish ETFs, ISIN IE…).

On top of that you have SQ fee (9.85 CHF) and the stock exchange fee.

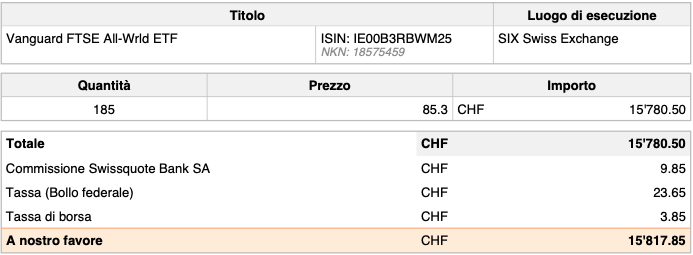

See below a screenshot of a real VWRL buy on SQ (in italian, sorry).

yes, this is correct, you pay 1% spread on currency conversion, therefore you will put this money on the table if you buy VWRA (in USD on LSE) while by buying VWRL you will only have to pay 1% currency conversion markup if you convert your dividends (in USD) back to CHF to buy additional VWRL.

Sorry for being unclear.

Yes you have three “virtual accounts” (balances) but if there is a currency conversion the 1% markup will always be there.

I think this would probably be the more interesting approach in order to minimize losses.

If I am understanding correctly here, the difference in fees for a 175k investment is a mere 200 CHF - so just 0.1%? That’s (considerably) less than the daily movement in price. So totally negligible in my eyes.

True. But honestly, I think it’s overcomplicating things.

Shouldn’t he/she be able to do the currency conversion externally? TransferWise for example should cost less than 0.5%.

I’ll now be heading to bed and bracing for the Vanguard fanboys.

(If I go compare it to VWRL on JustETF, the SPDR funnily seems to have outperformed VWRL over the last five years, though it does reverse slightly for other periods of time)

Is it? I mean, let’s say I stay with SwissQuote, my options are limited, so if I go with VWRL, what should I do with dividends?

A) Get dividends in my USD virtual account in SQ, transfer them back to my USD bank account, convert them somehow (Revolut I guess, but limits are not that big), and put them back into SQ as CHF

B) Get dividends in my USD virtual account in SQ, buy VWRA.

To me, as a total novice, option B seems more straightforward right? Having some VWRL and some VWRA doesn’t seem like a big deal right? Or am I missing something?

That is what I thought as well, I should be able to transfer out the USD dividends and then convert them as I want outside of SwissQuote, right? Do you mean that the transfer cost from SQ to an outside bank account in 0.5% in fees? That seems high

That looks like what I was looking for, no? It would solve the dividend currency conversion issue. I have no experience with ETF and Vanguard, so I have no clue what are the downsides in going no Vanguard but another ETF. on JustETF it looks like a nice ETF (same returns, 1billion+ fund size), it just has a higher TER from what I see, above 0.40% compared to the 0.22% of VWRL, does that mean that each year, I would pay in fees for VWRL around 400 CHF (0.22% of 175k), and with SPDR almost double that amount? Is that how TER works?

I’m so torn…I don’t really know why, but somehow knowing the money (all my money) is with a Swiss company makes me so much more confortable…

At the end, just to get a rapid overview, let’s say John Doe invests 250k in VWRA (in USD, on the LTE) on SwissQuote, and then invests another 250k in VWRA on InteractiveBrokers, after 5 years, what would be the real difference in fees?

I ask this because I keep reading that IB is MUCH cheaper and so on, so I want to put a price on my peace of mind, and actually see real numbers on how much cheaper it is.

For example, if it would cost 0.1% of the total investment more than IB, that would be still fine (250 CHF more expensive per year, I can pay that for sleeping better), but let’s say 1% more expensive? Then I would start thinking about changing.

Side tracking the discussion, but there’s probably much higher difference than SQ vs. IB by avoiding tax leakage and switching from VWRA/VWRL to VT (which afaik is available on swissquote) and filing DA-1.

Sorry but I’m a novice, could you explain a little bit easier what do you mean? Tax leakage? DA-1? and what is VT? I searched it in SwissQuote trading platform but I get a lot of results for VT

Sorry that’s the next level of optimization, maybe don’t worry about it, start with SQ + VWRL, and revisit in a year when you’re more comfortable.

I don’t think that’d be a bad decision, the biggest cost is more likely to keep delaying entering the market.

Now for the (somewhat simplified) details (but really feel free to ignore it):

US is >50% of global market cap

US has a withholding tax on dividend, in practice that means for an Irish ETF holding US stock, you lose 15% of US dividends. A rough approximation would 2% dividend rate * 50% US stock * 15% = 0.15% per year

if instead of using irish domiciled ETF, you have a US domiciled one (e.g. VT), besides having lower TER usually, those 15% will be charged directly to you, instead of to the fund.

with the DA-1 form, you can declare those direct withholding to the tax authorities and they give you the money back

So in practice the difference between VWRL vs. VT is TER difference and those ~0.15% you’re losing in taxes.

(it’s actually more complicated, I simplified somewhat, there’s also estate tax which would add paperwork to your heirs, etc.)

In principle you are right but if he decides to stick with a swiss broker he should also try to minimize the number of transactions as for each buy/sell he’s going to “donate” the federal stamp tax amount…

Yes, in my opinion you’re overcomplicating.

I prepared to write a somewhat lengthy reply addressing your individual point, but I won’t.

Take a look at your initial posting. It set out quite clearly what you wanted: An accumulating All-World ETF that you could buy through Swissquote (a Swiss broker). I am going to assume it’s a long-term investment, since you said you’d then continue to contribute and invest 2000 CHF monthly. I am going to repeat it in bullet points for emphasis:

accumulating

All-World ETF

Swiss Broker (Swissquote)

That’s as simple as it can get - and IMO a very reasonable approach to long-term investment.

So why don’t you keep it simple - instead of questioning yourself (and us ) over the course of this thread, and coming up with complicated loops and jumping through hoops, just to eke out a fraction of a percentage in savings?

The currency conversion on purchase of accumulating ETF shares is a small one-time cost. Maybe it’s percent at Swissquote, vs. a fraction of a percent less at other brokers. You can think of it as a price you pay for your peace of mind of having your assets at a Swiss broker.

But here’s the thing: small, one-off costs do not matter over the long run. They won’t substantially affect your outcome after several years of being invested.

What you may rather want to focus on is minimising recurring costs. With your choice of broker, you’ve surely made a non-cost-optimal choice - but you’ve clearly stated your reason and motivation to do so. Fine. Moving on…

As such, my advice might be to keep it simple: Invest in an accumulating All-World ETF - which is what you wanted in the first place, mind you - and just suck it up (suck up the negligibly higher one-off cost due of converting from CHF to USD, that is).

PS (splitting off the last point from the previous post):

Even when you convert CHF to USD each month to invest your 2000 CHF monthly contribution, it’s not a recurring cost of your (overall) investment - but a one-time on the amount converted.

Revisiting the idea of minimising recurring costs though, maybe, just maybe you indeed want to consider a US-domiciled ETF (as long as they are available to Swiss investors). There’s already lots of information on them on the forum.

Currency exchange costs alone are 1% at Swissquote (vs. 0.00xx% at IB). Times 2 when you convert it back = 2%.

Stamp duty is 0.3% = 0.15%*2 (buy+sell)

Tax leakage as someone mentioned above is another 0.15% (to 0.3% for 100% US), recurring per year.

And we haven’t even gotten to transaction costs, which are very expensive like everything in CH just because it’s swiss = carte blanche to charge loaded swiss customers whatever they want. They might not be as greedy as the big banks, but still very expensive compared to foreign brokers

As I hinted at previously and again above, I don’t believe comparing TER gives a full picture. That said, I’d probably choose VWRA myself out of the two.

I see your point. If there’s no minimum fee for currency conversion, makes sense to buy the distributing ETF.

Guys, I cannot thank you enough! I’m really overwhelmed with the amount of informations and support I’m getting, I learned so much in so little time thanks to you, I really appreciate it!

Now I have a pretty good picture about SwissQuote and what ETF are available there and what are the pros and cons.

One thing that is not fully clear, why shouldnt I choose ACWI over VWRA as it is on SIX, it is in CHF, for “only” 0.18% higher TER, while the other is in USD and on the LTE?

Is that just about preference with Vanguard for most people?

Finally, I’m seriously looking into Interactive Brokers as well,

first question would be, what is the right link for it? when I google it, I see IB europe, IB.com and IB.ch?

Finally, as San_Francisco pointed with his bullet points, what I am looking as first investment, is an All-World ETF that is possibly accumulating, so for SQ my options are clear, but for IB, what would be the best choice with those parameters? An US-Domiciled ETF?

So when I understand what are the options there, I will go and make some calculations and check for myself in a 5 year scenario, what would be the real cost difference and see if it is worth for my peace of mind or not!

8400 stocks, covering 99% of the worlds market capitalization with a 0.08% TER. 15% of the dividends that usually get lost with IE-domiciled funds are recoverable with the DA-1 form. So that increases (apart from the lower TER) your expected return by 0.3%/year.

Can’t resist repeating myself until it’s been hammered into everyone’s head…

The 15% lost figure is true for U.S. dividends (from U.S. corporations) “only”.

Whereas U.S. should only make up about half of VT/VWRL/VWRA.

So it’s probably more like a 7-8% figure on basis of the whole fund - notwithstanding that the Irish fund could be more tax-efficient on other countries’ dividends.

Of course, with a 55+ percent share U.S. securities in an All-world ETF, the taxation of U.S. dividends should effectively decisive factor in determining the most tax-efficient fund domicile.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.