Good evening everyone,

I’ve been told you’re a smart bunch of people so I’m kindly asking for advice ![]() Me and my wife would like to know whether our 2nd pillar plan is the best option for us or should we switch providers. Also, if we should buy the missing years or not. Hopefully some of you can help us understand our situation, your input will be most appreciated even if you’re not an official tax/financial advisor

Me and my wife would like to know whether our 2nd pillar plan is the best option for us or should we switch providers. Also, if we should buy the missing years or not. Hopefully some of you can help us understand our situation, your input will be most appreciated even if you’re not an official tax/financial advisor ![]()

When we moved to Switzerland five years ago during Covid we didn’t put much thought into choosing the best provider for us. We just wanted to start a business as soon as possible and found our company where we are currently both employed. Since we are employed at our company, we can freely choose the 2nd pillar provider. We are the only two employees at our company btw.

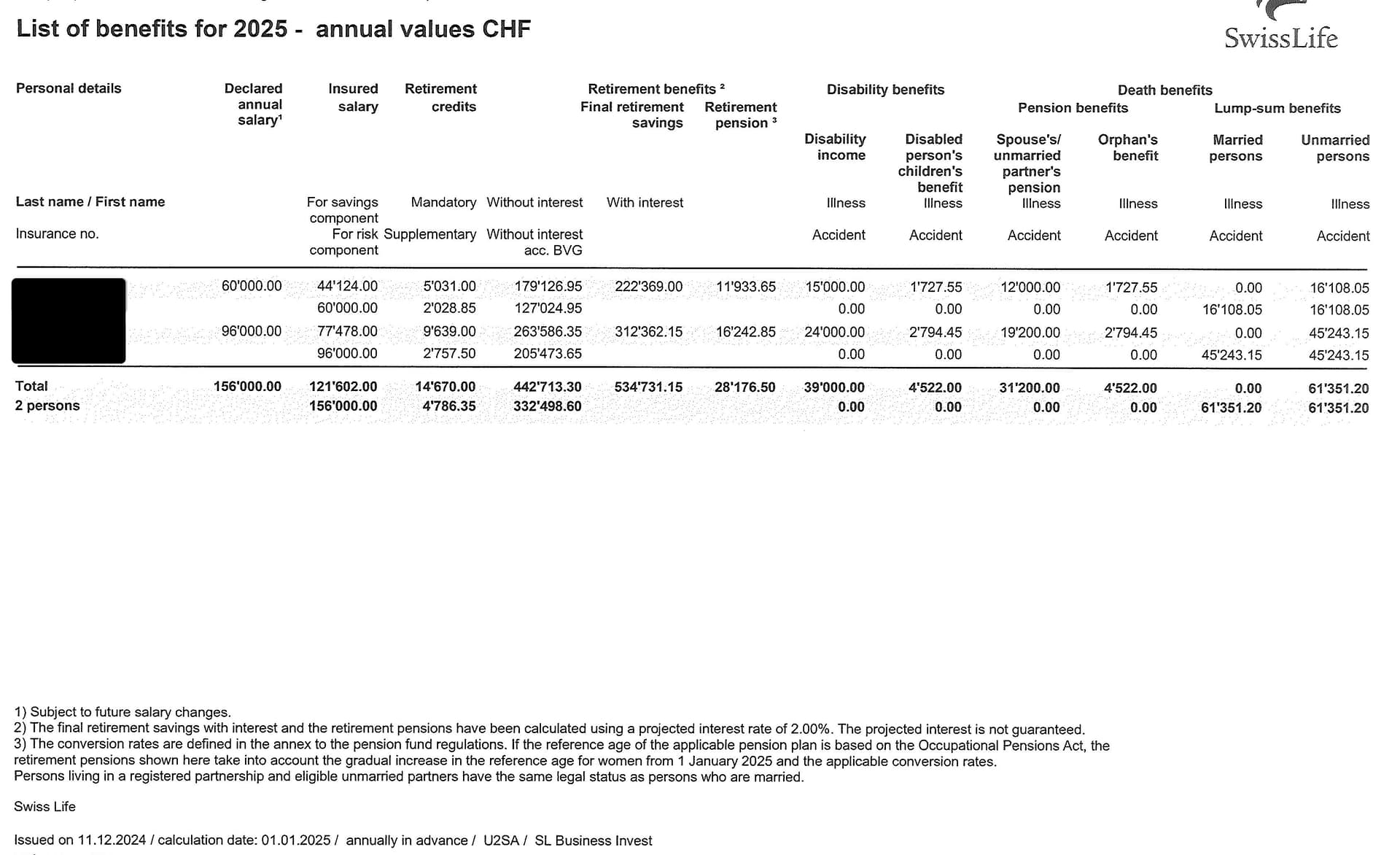

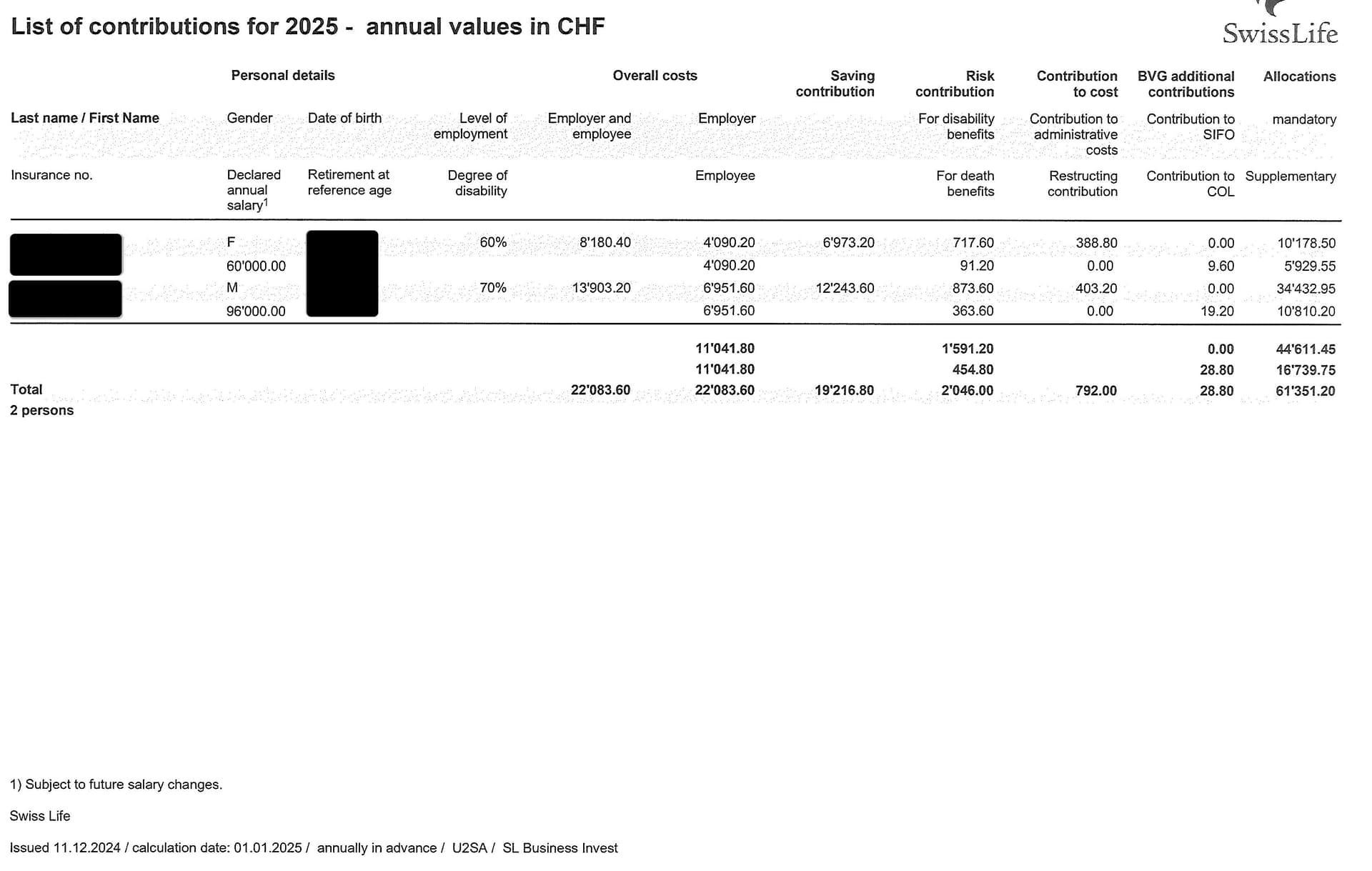

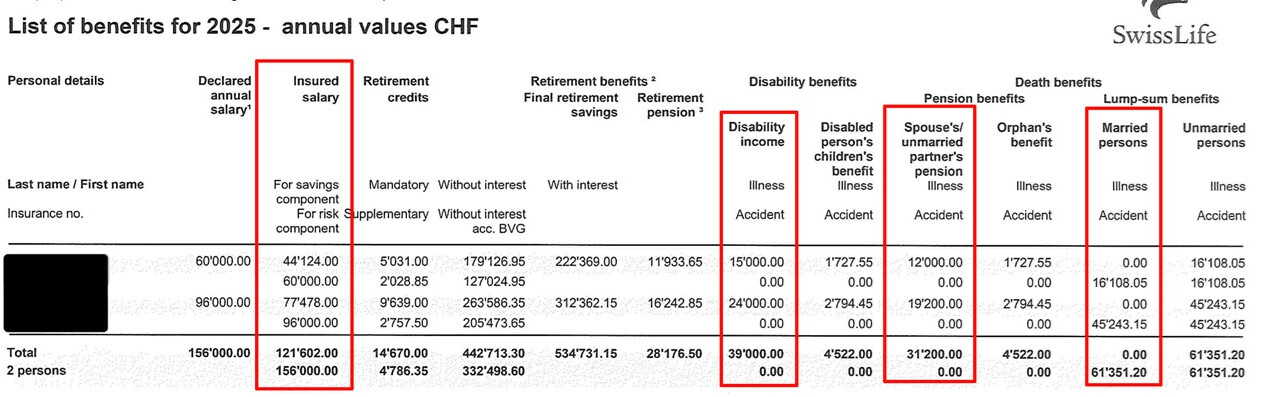

We chose Swiss Life Business Invest plan then. We have been paying little over mandatory amount but we don’t know if this is smart or we should rather put that extra money in a global index fund with better returns. I’ve attached out 2nd pillar certificates.

We are not risk averse and can stomach a stock market crash or recession for years. We both started 3rd pillars at Finpension when we moved to Switzerland and pay in fully each year.

We are in our late 40’s, no children and still have around 15 years until retirement. Exact time of (early?) retirement depends on whether we will muster the energy to work until the official retirement age or not. We’d rather not to be honest. We don’t plan to leave Switzerland before retirement and we don’t plan to use 2nd pillar money early to buy RE or similar. We currently have no plan to buy any real estate any time soon (we might rent forever). Based on our family history we do not expect to live past 75-80 so dying with zero is an attractive proposition.

Our combined gross income is currently 150k which is little less than our company yearly revenue. We don’t have any other wealth except 2nd and 3rd pillars accumulated in the last 5 years and around 15k in stocks. Obviously when time comes of our parents’ passing, we will inherit their modest houses back home with our siblings which we’ll sell right away and invest the money into a global ETF. We plan to live/spend a lot of time in a cheaper (sunnier ![]() ) country after retirement.

) country after retirement.

We’ve been employed for 15-20 years in our home country (EU) before leaving for Switzerland. This will give us a combined pension back home of around 300 eur monthly by today’s calculation when we reach their retirement age.

We don’t know if we can/should buy the missing years some people talk about? To be honest, I don’t even know what “missing” means in our case ![]() We don’t have any private money lying around but we have a low six figure amount in our company’s business account which is currently deposited in the bank at 3 % interest rate. Could we use this money to buy the “missing” years? Would it be a better idea to invest this money in a global ETF (which is then subject to capital gains tax)? Or pay ourselves dividends/increase our salaries and invest the money as private persons to avoid the capital gains tax but then we have to pay the income tax?

We don’t have any private money lying around but we have a low six figure amount in our company’s business account which is currently deposited in the bank at 3 % interest rate. Could we use this money to buy the “missing” years? Would it be a better idea to invest this money in a global ETF (which is then subject to capital gains tax)? Or pay ourselves dividends/increase our salaries and invest the money as private persons to avoid the capital gains tax but then we have to pay the income tax?

To quickly summarize, these are our main questions:

- Should we keep the same pension plan or switch? We heard Profond has more aggressive 2nd pillar options with up to 50 % invested in the stock market hence the higher returns? Is it worth the hassle? I like the idea of higher returns in the long run.

- Should we continue paying more than mandatory amount or keep it at a minimum and invest the extra money privately in the global ETF?

- Should we buy in the missing 1st/2nd pillar years (whatever this means)?

- How/should we use the company money which is currently doing only 3 % per year?

Thanks for all the valuable insight. I know it’s a lot to unpack and these questions are best directed to a tax/financial advisor but don’t be afraid to give your opinion, just imagine we’re discussing life choices and mistakes over a beer in a pub ![]() Unless of course you work as a tax/financial advisor in which case feel free to contact me for consultation.

Unless of course you work as a tax/financial advisor in which case feel free to contact me for consultation.