Example: TransferWise and Smartbroker:

About 6 CHF/month to invest a 1000 CHF each month VWRA, from the first 1000 francs.

That’s obviously comparing Apples to Oranges. But as long as I have steady revenue stream (salary), I can start from literally zero savings and average costs over time. With one-time transaction-only fees and no other recurring costs (other than the ones baked into the fund obviously).

Which fund size is considered as “safe”, i.e. low risk of closing? 500M CHF?

At the moment I don’t plan to under-/overweight. I am just asking myself, if I should chose VWRL/VWRA or SWDA + EIMI. That’s why I created the cost-comparing table above.

I do plan to invest on a regularly base, but rather quarterly than monthly. I assumed that Degiro is considered as the “best” (whatever best means) broker for investments lower than 100k.

I don’t know. But I wouldn’t be particularly concerned anyway. Their All-World ETF is their second biggest Irish ETF - and the accumulating one is just a variation of it. I ca

Being “considered as the best” on this forum is mainly a result of…

DEGIRO indeed being one of the cheaper European ones available to CH residents.

Them speaking English (which virtually no one in Germany does)

People on the internet (including this forum) jumping on the bandwagon

To be clear, there’s nothing seriously (morally) wrong with earning referral commissions on one’s website. The reader just should use proper judgment in deciding for himself. Weighing the fact that the brokers has been tried and tested by someone (many) vs. the fact they also might earn a commission from promoting it.

Also, I don’t think there the one “best” broker. There might be “best” ones for someone’s needs.

Me personally, I don’t expect big website to be 100% up to date and correct on everything. But I do find it a bit of a red flag that they (DEGIRO) have linked the “wrong” price list on their website. I also prefer renowned banks for their supervision and experience.

That said, I have been and would still be using IBKR even below 100k - as I’d do monthly exchange of currency anyway. Used to do it via TransferWise, which would cost me 4-5 CHF. With IBKR I’d just count it against their minimum commissions.

No problem either.

It’s micro-optimisation, really. If you don’t want to overweight/underweight EM, I’d just go with one of them. iShares has had an MSCI ACWI ETF for years - which seems to have (only slightly) lagged VWRL. So I’d probably go with VWRA - as being the (accumulating) sibling of their second-biggest Irish equity ETF.

Since you’ve been a “long time reader”, it might be more important to take action than to overanalyse and -optimise. In your investment career, you are inevitably going to take sub-optimal decisions along the way. That said, with between the two choices you present, you’re hardly able to make a relevant “mistake”. The difference in outcome is most certainly going to be very small. The more important question might be if you’re ready - and suited - to invest in equity markets. And if so, when, how much, and on what time horizon.

You got my weak point. The last hurdle seems to be the biggest.

Before I discovered this forum, I only considered Swiss broker. After reading many posts, I was pretty sure to go with Degiro. I registered and I was disappointed about the waiting list. Now I am about to set up the account, but I started doubting if Degiro is the right choice.

Let’s assume that I made my choice concerning the broker. How would you invest 50k CHF?

I thought about buying for 5k CHF every 4 months. After 3 years, 45k CHF would be invested.

I am aware that DCA is not the most profitable way. But I am not that confident as a beginner to invest a lump sum.

Well, you’ve basically answered your own question, haven’t you?

Now imagine you invested everything as a lump sum… would you rather kick yourself for missing out on a great opportunity, by not trusting some random “Cortana” dude (and his links. “Live smarter. Live richer”) on the internet? Or would you rather berate yourself for following his advice, even though you didn’t really feel comfortable about it from the beginning?

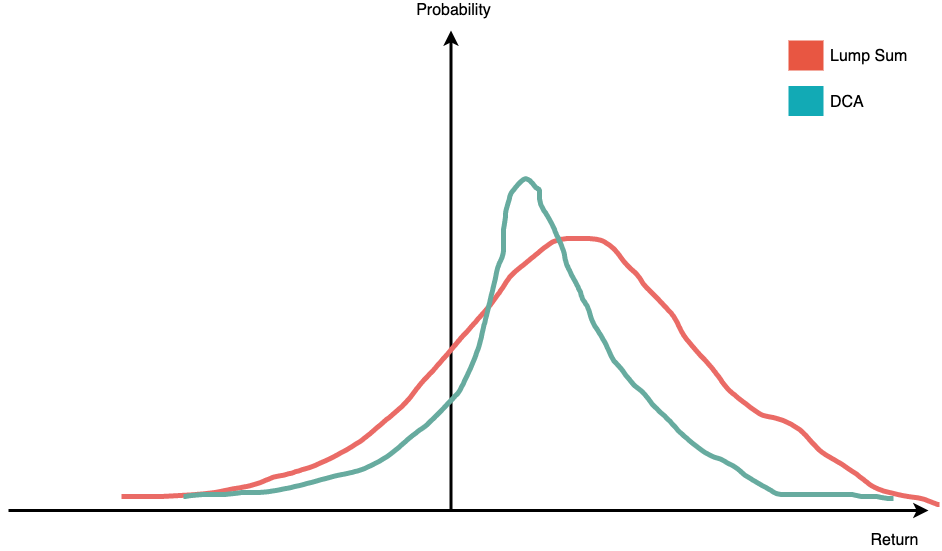

side note: I see nearly everybody advising against DCA based on several articles which demonstrate that - from a numeric point of view and based on historic data analysis- LS provides better results

Nevertheless, with reference to 3rd pillar payments, I understand that most have set up a recurring - monthly - payment, even if the amount is “only” 6’800 CHF…

Me, I’m used to transfer the $$ as a LS at the beginning of the year… unfortunately, it seems to be always the “wrong” moment as since I opened my VIAC account (2018) and despite 3 LS payments, I’m -2.62%, while nearly everybody seems to be gaining…

Well if the money was avalaible, I would lump sum invest it anyway. Problem is, my emergency fund is already full and I don’t have any dry powder anymore. The only thing I can work with is the 2000.- I save each month. So no other choice than buying every month as soon as it’s on my account.

Those are really good thoughts. I think the latter is rather true in my case.

It’s also a struggle between brain and gut.

My brain says: You read many (scientific) articles and post from this forum, which clearly shows that lump sum investing leads to a higher profit in most of the cases. It’s a fact.

But my gut is more like this: What if those articles are wrong? Isn’t the current situation extraordinary? Better start slowly and gain confidence over time.

I don’t know how you started investing. I guess that most of you made small steps in the beginning as well.

To add my 2 cents of thoughts (and it might be all they are worth ).

Yes, lump sum beats DCA in 2/3 of cases, i.e. on average.

I would argue that we are not in an average period of times. (valuations almost at all time highs again, for some companies even at ATH - with what follows economically - a bit hard to believe; but I am no market expert)

DCA works in a “bearish” market, as Cortana linked.

Opinions on what follows from today onwards are just that - opinions and speculations, nobody knows.

In your shoes I would setup a personal rule, which would work for you “emotionally” as well, whatever lets you sleep at night (even though it might statistically be wrong) - and follow it throughout.

E.g. “If the amount to invest (bonus / future windfall etc.) is more than 10-20% of my investable assets, split it up into chunks and invest over a certain period of time”.

But probably not 3 years, rather a couple of months/quarters.

Going back to your question on 50k - you need to put it into perspective of your future income and savings over the next 3 years.

And as a matter of fact, all of your future income/savings - these 50k will probably be “popcorn”.

If you save another 50k within 2-3 years, there is no point in splitting this current 50k and investing them over 3 years, as you would end up with loads of cash sitting around (unless it matches your decided asset allocation).

Personally, in that situation, I would probably invest 5k each month.

The advantage of lump sum vs DCA is common sense. If today is the best day to invest $100, then it is also the best day to invest $100’000. If tomorrow will be the better day to invest $100, then this will also apply to $100’000.

That is, if we’re speaking about maximizing our expected return. It’s a different story when we talk about the volatility / standard deviation. I would not be surprised if DCA guarantees lower volatility, as our intuition tells us.

I am pretty confident that I’ll save another 50k in the next years. Therefore, I reconsidered my investment plan and intend to invest the amount within a couple of months.

This is also my knowledge. DCA lowers the expected return, but also decreases the volatility.

I found a paper from the university of Mannheim, which states the following:

Das Einmalinvestment ist systematisch überlegen hinsichtlich der mittleren Wertentwicklung. Dieser Vorteil steigt generell mit der Länge des Investitionshorizonts.

Der Sparplan ist hingegen systematisch überlegen hinsichtlich der Standardabweichung

des Endvermögens.

Well of course it reduces volatility. You have basically a lower stock allocation over the whole DCA period. At the beginning you have 0 risk, at the end you have 100% market risk. So 50% market risk on average in those 3 years.

Everything can be obvious once you give it enough thought Also, some things may seem obvious but be counter-intuitive. So it’s good to really check. Also, people, also in this forum, have different DCA strategies, like buying a little after each 10% drop, which we could witness during the corona panic.

I guess the takeaway is that when people do DCA, they instinctively do it in the hope of lower volatility and not of higher return. Losing 10’000 affects us more than winning 10’000. But once you’re 100% in, it’s all the same from that point.

I bought 100’000 for of VTI at the beginning of March (it recovered, woo hoo!). Would I have been better off doing the DCA? Probably, but also maybe I would hold off investing even further, constantly evaluating if it’s the right time. Once you’ve committed yourself, you can at least stop obsessing about it.

That’s IMO one of the biggest advantages of lump sum. You stop thinking about the market and you don’t really worry about the future.

Maybe if you started with DCA you would have stopped at some point in the hope to get even lower prices. Then markets went up and you probably would still sit in cash with 80% of your assets. Still waiting for a new drop which might never come.

DCA is “market timing light” and might hurt you greatly longterm.

This sums up my my thought as well. While the statistical advantage of dollar cost averaging might be true in “normal” times, I’d also argue we aren’t experiencing them at the moment.

On the other hand, I’d assume the economy and markets to return to normality within three years. Even the 2001 and 2008 bear markets (or crises, if you’d call them that) didn’t last longer than three years. Though it might possibly be a “new” normality, with some societal changes, and maybe unprecedented fiscal policy, interest rate or credit risk factors.

Whatever happens, I don’t think there’s a point regretting cost averaging over something like the next three years.

In doing so, I’d also try to (conservatively) estimate future income than can be invested over this period and do the calculation on this basis, e.g.:

Having an investable lump sump of 50’000 now and

an estimated 2’000 monthly investable income (or 72’000 over a span of three years)

…makes for a sum 122’000 (ignoring inflation and small wage hikes) to invest.

Cost averaging over the next 36 months, that could mean investing 3’389 a month.

A global pandemic, which makes world’s economy “shut down” for a couple of months, and people losing jobs at an unprecedented rate (in the US at least), with certain experts claiming that not only a recession, but a depression might be at the door; could be one example.

But, as mentioned earlier - stock market != economy - so no real “predictions” anywhere.

Not really.

Some people just have a feeling they can “time the market” a bit this time, on a macro level.

Disclaimer: I am still as invested in my ETFs as before (even more so, was lucky to grab some stuff while around the March bottom).

Piling up slightly more cash than usual (also because I have some expenses and alternative investments coming up).

I will definitely not sell everything because I think it will all go down. Just spreading out my risks a little bit.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.