Securities lending allows you to lend your stocks/ETF to someone looking to short them. They will pay you a % borrow rate, and sell the stock hoping to buy it back for less when they return it to you.

This seems like a very low risk way to get additional cash while holding equities.

IB will lend any applicable stocks/ETFs you hold to short sellers

They will pay you 50% of any borrow rate they collect

Lending is done on a pro-rata basis, so if 100 stocks have been offered for lending but there is only demand for 30 stocks, IB will lend 30% of everyone’s offering

Downsides/Risks

As I understand some reasons not to bother opting in for securities lending include:

Feeding the short sellers incentivises them to push prices down lowering your returns

Returns aren’t too high. Borrow rates are generally fairly low (although can be as high as 50% annualised around certain events!)

Demand for securities lenders isn’t so high so won’t be able to loan out all your shares

Tax issues: In the US dividend payments from the broker while your stock is lent out count as ordinary income not qualified dividends so you may pay 30%+ tax vs 15% tax on dividends.

IB will take 50% of the profits, further dampening your returns

Regardless, additional return for negligible risk seems very tempting as an ETF holder with a long time horizon.

Does anyone have any experience attempting this in Switzerland? In particular through IB with the typical Mustachian funds (VT, VTI, VXUS).

Also take into consideration that most ETF’s do securities lending themselves. Of course there’s a difference between Blackrock “failing” and IB “failing”, but still.

With IB, you get a cash deposit in the value of the lent-out shares as security in your account. Cash is protected in a bankruptcy under the applying regimes. If you used margin, IB will rehypothecate shares of yours in the same amount, usually the most profitable ones. There is, of course, no deposit in this case.

Funds are separate entities from their asset manager. A bankruptcy of Blackrock would not encompass those assets. Funds get securities from their borrowers covering over 100% of the value of lent shares. Securities should be of good quality. The prospectus will tell whether they rehypothecate those securities again.

That’s why I put “failing” under “” in both cases. I just wanted to emphasize the almost never known fact that almost all ETFs are doing securities lending and that some might not feel comfortable with it and might want to look to alternatives (like the very young SWRD for the MSCI World, which is even much cheaper than its ishares-counterpart).

Also, wouldn’t this “cash collateral” be a problem regarding US estate tax?

Of course ETFs which lend securities are overcollateralized, but what would the situation look like in a sell-off, with illiquid ETF-underlyings and illiquid collaterals… But ok, that’s another discussion.

This was too subtle for me … I wasn’t sure where you were coming from.

Cash on US bank accounts even makes one obligated to make a yearly tax declaration. IB serves Europe from Britain, so this is no problem. (USD-)Cash itself isn’t a US situs asset (no inheritance tax troubles either).

Cash at IB is not equivalent to cash in a US bank account.

It doesn’t matter which branch of IB is serving you, it is all considered US situs. Dealing with IBUK does NOT shield you from all the relevant tax issues!

Cash (no matter whether USD, EUR, CH, or whatever you want) in your IB account is US situs property. IB is a US domiciled broker. Everything related to cash is cleared through IB LLC. It is of no relevance whether you open your account with IB US/UK/HK.

USD are not situs assets when in an account outside of the US. IBUK is the entity tasked with holding USD. It is the legal firewall against having to declare US taxes annually. Shares are US situs assets. Treatment for income tax purposes 》 DBA with US. Treatment for inheritance purposes 》inheritance tax treaty with US.

Edit: Where the (trading) broker is domiciled does not matter in this. Wirh equivalence, they can contract outside their domicile. What matters is the location of the cash assets. And they are held with IBUK in the UK. I hope this is now clear.

I link here, for background, a presentation from the association of Swiss inheritance experts.

Witout commenting on everything else - this is complete and utter BS. You do not need to file US taxes just because you have a US bank account.

(Schwab don’t do the UK trick, Schwab customers also don’t have to file US taxes. Don’t get confused by Schwab UK, Schwab UK only serve a few countries, Schwab’s Swiss clients are direct clients of Schwab USA.)

Brokers and banks are always distinct entities in the US, unlike in EU, bank can’t be a broker there and vice versa, different laws and regulations apply to each.

In any case, Switzerland has an estate tax treaty with the US granting you an exemption of up to $11M so long as you die remaining a swiss resident or citizen. So there is no problem here unless you’re filthy rich. Worst case, some nuisance for your relatives to fill out IRS forms after your death to avoid the tax.

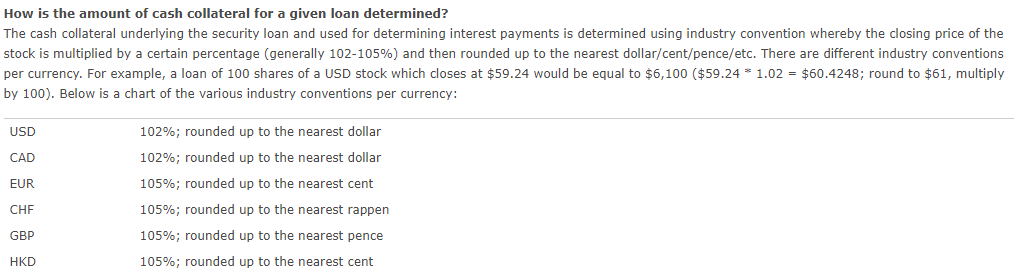

Getting back on topic, I have a question regarding this note from my IB Activity Statement:

Say that I participate in their “Stock Yield Enhancement Program” and my VT shares are lent to a short seller for which I get a cash collateral equal to last closing price X 102% (see below screenshot from IB’s FAQ). Does this mean that, if there is a high volatility in the market and the price of VT goes up the next day by say 15-20% and the short seller that borrowed my shares can’t post more collateral (e.g. goes bust), I will lose the shares and just get the original collateral posted initially!!! This will result in a loss on my account of 13-18% (i.e. the increase in price less the 2% additional collateral). If my understanding is correct, than this risk is very high imo and I’ll opt out from this program asap…

Hmm, this would make sense. If the collateral posted by the short seller covers a higher volatility (say around 15-20-25%) than the 2% that IB gives to me then theoretically it should be fine… Unless there’s a really big spike in a single day (e.g. a flash crash or some other ‘black swan’ event) that catches the short seller off-guard and unable to pay the margin call - something similar has already happened during these days (https://www.ft.com/content/7385a2f9-434d-4ffc-8d11-2b2a8973d258)

Hi there! I am bringing up this oldish topic to give you my experience with securities lending in Switzerland and the Interactive Brokers Stock Yield Enhancement Program (SYEP).

I had some CH securities lent out at the time of dividend payment and IB paid me dividends as “payment in lieu” (PIL), detracting 35% for the usual withholding tax. Too bad that I will not be able to recover the 35%, as it was not paid in my name, and that at the end of the year I will be paying taxes on those dividends at my marginal rate. So it’s 35% less, and then again taxes as usual.

So, my friends, if your CH stocks yield dividends, think twice before lending them out with IB as it could cost you a lot more than what the programs gives you back.

On the other side, if your experience is different, and you received an amount equivalent to the full dividend (without the 35% deduction), please do let me know – I tried bringing up the matter with IB, but without any result other than me opting out of the SYEP.

Hi Koreba! Since the shares were lent out, dividends were paid to the borrower, who can not reclaim the withholding tax as it is not the beneficial owner (I am). On the other side, my IB statement does not show that I paid the withholding tax (which I did not, of course, since it was paid by the borrower), but only shows that I received a given amount for “payment in lieu of dividends” (and this amount is 65% of the dividends). I live in Ticino, and I just can’t see how can I claim back something that I never paid. As others I have said, I would need to discuss this with the help of a professional, and the costs are likely to overcome any benefit.

I think that the problem is with IB. They should forward 100% of the dividends, and the fact that the borrower can not reclaim the withholding tax should be just part of their risk. I have terminated participation in their SYEP since the unpredictable advantage is not guaranteed to cover the certain disadvantage of being heavily taxed.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.