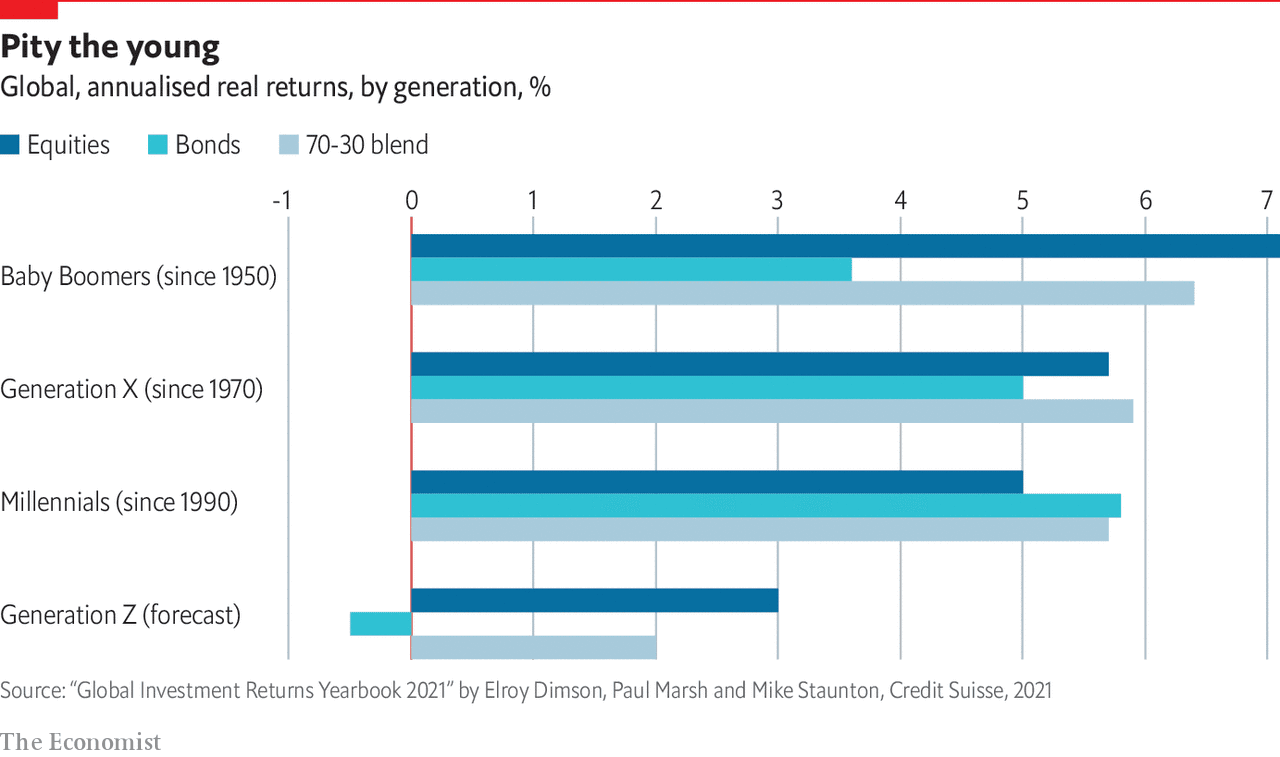

How did they come up with these numbers? “…current bond yields to indicate future bond returns. It then adds our estimated equity risk premium (relative to bills) of around 3½% on a geometric mean basis to provide a projection of equity returns” (pg. 27).

I’m not sure I buy into their (or anyone’s) attempt to predict the future, but the case for future real returns over the next decades being weaker than those of the past few decades is certainly quite strong.

Isn’t “future real returns” an oxymoron?

All they can try to predict are the expected returns, by definition.

[edit: Thanks nabalzbhf for the correction :)]

P.S. Yes I am also more conservative with my expectations vs. last decade’s returns.

P.P.S. Wasn’t there a similar topic opened up recently? Perhaps we can blend them.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.