So I was looking ahead to figuring out how I would set up my pension fund allocation after I quit my job and put the Pillar 2 into a VB account. I plan to split the pension fund between VIAC and Finpension to not have all my eggs in one basket.

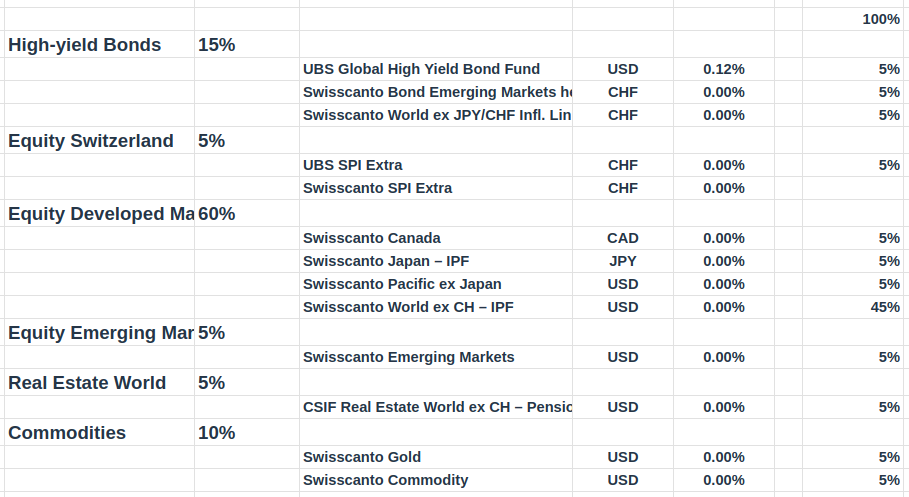

I noticed most Swisscanto funds had zero TER compared to UBS/CSIF. Does this mean that it is a no-brainer to go with the Swisscanto equivalent fund? Or are there fees hidden elsewhere or other quality issues?

I think the main fees is coming from the custody fees of the portfolio and that’s how they pay for the funds. Otherwise the difference between average TER or SWC vs UBS would be less than 0.01%

If you like SWC, just go with that. Wouldn’t matter much in long run.

I want to make one point . The more granular you go into your approach , more possibilities you would create for rebalancing.

Each of the fund also have buy/sell spreads. So everytime rebalancing happens you will incur those fees.

I know VIAC & FP always try to reduce the need via net pooling. But still something to be aware of

I agree that higher equity allocation (inside pension funds) might be easier to manage from psychological perspective. But in CH, this might not be optimal due to the lumpsum taxation.

For example if your portfolio is X and 30% of it is bonds. And let’s also assume 30% of your portfolio is inside pension assets (3a , 2nd pillar)

In some cases (depending of wealth tax, lump sum tax etc), it might be beneficial to have VB allocation = 100% bonds

You mean given a stock/bond allocation, and a taxable and non-taxable account, you push the bond allocation as much into the non-taxable as possible to:

Receive interest tax free

Reduce capital withdrawal tax

It’s a good idea. As bond/cash component is partly for liquidity, you could end up having to make occasional manual adjustments to move the liquidity from the VB bucket into the taxable bucket.

I guess I could weight it towards the VIAC side since that has weekly re-balancing.

Not an expert and therefore just voicing some thoughts. Also, surprised about zero TER for Swisscanto ETFs.

I wonder about the bonds. It’s an asset class I don’t even consider. China as second largest economy is ominously absent from your asset allocation. Why Canada and not India?

For an all-weather portfolio, I would go for a higher percetage of precious metals (Au, Ag, Pt), preferably from ZKB, where physical gold is stored. Not sure if the Swisscanto Gold Index is the same.

To lower the counterparty risk, you might want to replace some Swisscanto Funds with other emitters.

It’s a lot of positions, was my first “impression”.

You have World ex CH and Japan, Canada, EM etc indiviually. Is that intentional (to reduce overall weight of US)?

There’s cheaper ways to get gold (& probably commodities) exposure than Viac’s + Finpension’s 0.4%. Also I keep such non-yielding assets out of the tax sheltered.

At Viac you’ll be getting 2 “portfolios” (oblig/non-oblig), will you set both identical?

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.