I can‘t imagine Truewelath can offer that? How is TW making money if they have zero fees and use funds with zero fees? Only by also selling their Robo Advisor to people already being in the 3a? So essentially the 3a being an indirect ad for their actual seevice.

They probably get some comission from ishares etc. for the ucits funds. But CS offering substantial comission for their zero fee pension funds?

Maybe the advertising is enough, but I have a hard time imagining that.

I know, and this “trickery” was precisely the reason I wasn’t with them up till that point.

Nevertheless, on paper this meant that the fee was reduced.

I’d kinda expect competition to continue and that at some point we’ll get a competitive 20bps provider, with no TER on funds. Beyond that I’m not sure the fees are really meaningful (most ETFs have 10bps or more while the providers have bigger scale, 20 is fair esp. given it’s tax sheltered).

I believe that’s very difficult to achieve , let’s assume 2 billion CHF assets under management for calculations sake. 20 bps will mean 4 Million CHF revenue

4 million will need to cover

costs of buying / selling / holding / rebalancing underlying securities because let’s face this it’s not free to replicate the world index

costs of employees and Tech running the operations

profit for the business doing all this

regulatory/ compliance costs etc

I think 20 bps might be possible with very large AUM but can be tough for new ventures.

I believe sometimes we forget that Switzerland doesn’t that same advantages of scale like US, possibly even UK or other countries. Any business which wants to serve Swiss market (unless an international player) will always have higher fixed costs. With AI such costs might reduce but it’s a difficult task. We all like higher salaries in CH but not the higher costs (kind of ironic ;))

I’d split the cost of fund vs. the cost of running the pension foundation.

Funds have massively more than 2B under management (the market is basically the entire swiss pension stash), do you think CS/UBS charge way more than 10bps for their 0-TER passive funds?

I agree. I don’t think CS/UBS charge a lot. But I think they still need to charge something. Zero fees fund is simply not possible. So it might not be mentioned in TERs but there has to be costs for buying such funds. There is exchange fees, there is stamp duties, etc in various countries. Even vanguard incur 7 bps fees to run VT.

So let’s say 5-10 bps for underlying costs of securities and then 10 bps left to run the business. Hence, it would need significant large AUM to get down to total of 20 bps. Of course it also depends on competition.

I think 1E plans are close to 30-32 bps at Finpension so maybe it’s achievable to get down to 30 BPS. Let’s see.

Also, i don’t think it’s cheaper to run an ETF than a fund, And we need to compare with european based ETF which are around 0.12% for developed world and 0.2% for global.

How would it be possible for UBS or ZKB to run a fund cheaper than Vanguard, Ishares or State Street?

As I said I don’t know. I just wanted to say it’s not Zero.

You are kind of confirming what I was trying to get to. I really don’t think we can get 3a offers for 20 bps.

I know true wealth is offering something very low cost but I don’t understand how is that even possible.

Funnily, it seems that Google already indexed some of their investing pages [1].

What can you expect from the wealth management offered by finpension?

You can expect a tax-optimized and cost-effective investment of your assets from the service we offer. We focus on the passive management of your investment strategies and mainly use ETFs (except for private markets). The investment strategies offer good growth opportunities while at the same time minimizing risk. In addition, we allow you to adjust your investment strategy and define the allocation yourself. [2]

So it seems it’s more or less same as 3a + higher cost funds. I would be curious to see which funds they actually use and if they are tax advantaged or not (most likely not)

Thanks @oswand Snowden for publishing finpension leaks.

So in summary (provided this is not an older draft but the final conditions and nothing changes before launch):

fractional trading, up to 10 different portfolios

access to private equity (through a private equity ETF?)

no transaction fees on top of flat fee (what about stamp duty?)

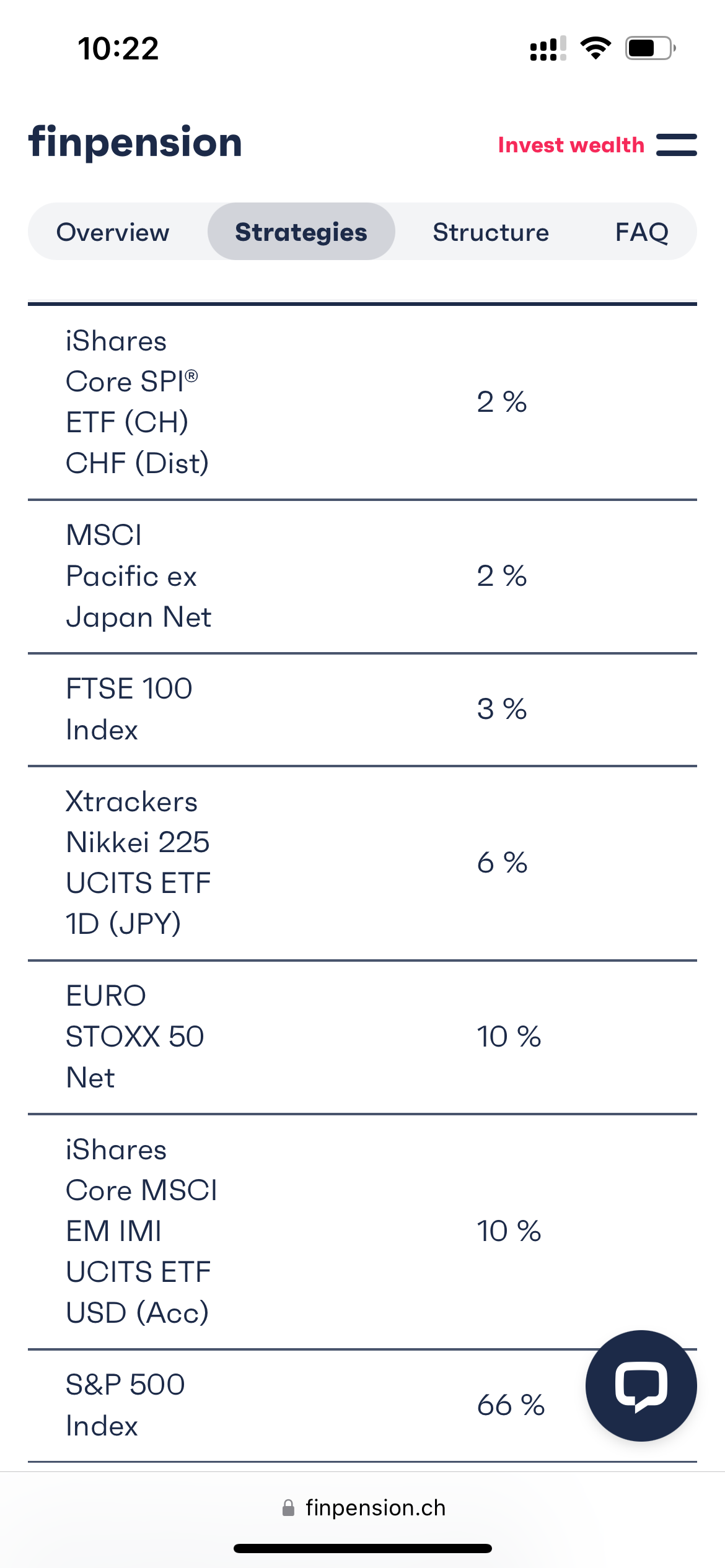

global strategy looks like generic FTSE All-World

no degressive pricing depending on amount invested (findependent is cheaper from 250k upwards)

no benefit in having both free assets and 3a money with finpension

So if I would buy 3 ETFs per month and had over 200k, I’d pay about CHF 600 yearly with Swissquote (arguably an expensive broker), but here I’d reach these costs with 150k already.

Probably just marketing. Most people have no clue about WHT, etc. So they just highlight that they use ETFs domiciled in Ireland or something like that. [1]

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.