Strictly looking at transactional costs, UBS key4 offers the best credit cards for non-domestic use (only talking about card payments, not ATM withdrawals, of course). No fee for international CHF payments and currency markup is 0.5% on top of the Mastercard rate (unlike the regular UBS credit cards, which are probably one of the worst). They come with a monthly or yearly fee, though.

Besides UBS key4, the swisscard visa and Migros Cumulus credit cards also don’t charge fees for international CHF payments. Their currency markup is significantly higher than UBS key4 (swisscard seems to be better than Migros, though) but they don’t charge a monthly or yearly fee.

Right. Which is not to be confused with the Swisscard Cashback Visa

Am I correct in stating that Migros Cumulus is the only credit card that has no fee for international CHF payments and offers cashback?

Actual cashback, I think so. UBS key4 credit cards offer 0.2-0.4% in KeyClub points, which you can use to pay the monthly fees or also for something like Migros gift cards, but you have to actively redeem points once a year or so.

Well, that’s actually not that different to the Migros card offering Cumulus points, but that might still be slightly more convenient if you anyway shop at Migros.

May I ask what these requirements are? I have now opened a Wir account for myself, my mother, and also know of several other people who opened a Wir account. I also recommend Wir to friends and family, so knowing about potential limitations would be helpful.

Ah, ok. Let me specify then:

Am I correct in stating that Migros Cumulus in the only credit card that has no monthly or yearly fee, has no fee for international CHF payments and has a system of direct or indirect (though points or similar) cashback?

I only met the the first requirement when I opened the account a few months ago, nothing else (in the mean time I bought some shares of my own initiative)

My rules of thumb for card payments - or any retail payment, actually:

Paying as much on credit card as possible, as this psychologically reduces spending and is easier to track.

Transations/merchants that I know are Swiss: use a credit card that collects bonus points or cashback, e.g.: Cembra IKEA Mastercard, Swisscard Bonus Card/Poinz cards

Everything (potentially) “foreign”: Using a non-Swiss card that doesn’t charge foreign transaction fees and has low to no FX fees/surcharge, e.g. Wise, Revolut, Advanzia. I don’t even bother thinking about using any Swiss credit for such transactions, they’re basically all more expensive.

Exception: Paying for something that I want to have insurance/warranty extension on and I’m OK with paying a little more.

Not sure that this is a downgrade. Yes, I also see Privatkonto top in my ebanking. But I also got the debit Mastercard and ebanking. So I have the full Bankpaket top package.

You’re right, mine is different. Still, I wouldn’t worry that much about it, but see it as a service that is not perfect in all details.

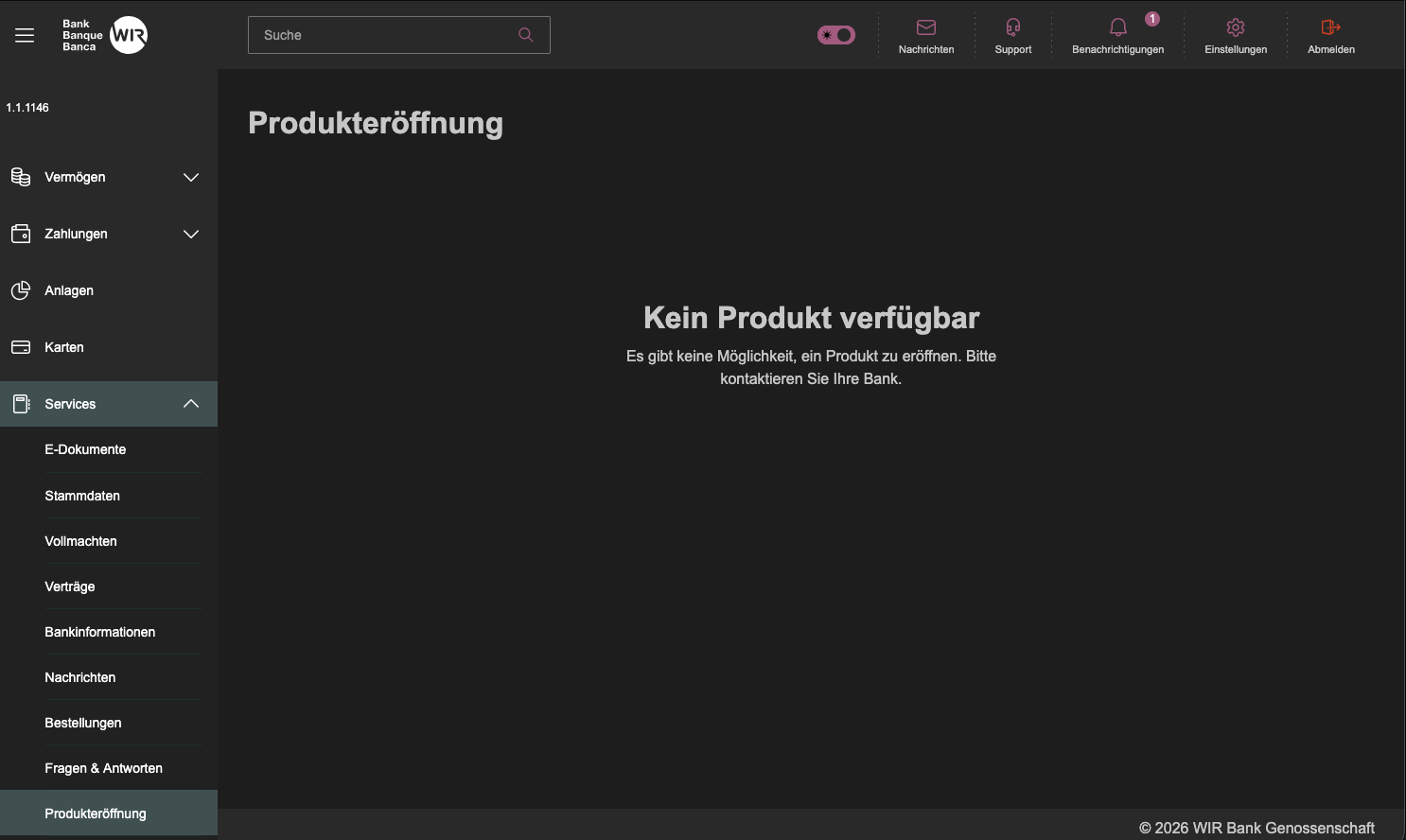

You have the option to open a EUR or USD account. If everything worked perfectly, I should also see this option, since I don’t have a EUR or USD account at Wir. But there is nothing visible for me.

This is correct, based on my research also UBS Key4 credit cards have the lowest currency markup with Mastercard rate, although they come with monthly cost, but you get KeyClub points, similar to Cashback. Contrary, Swisscard has a 2.5% transaction fees even with their Cashback option.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.