Depends. If it’s a genuine bank with a banking license and deposit guarantee, I’d have little issue with depositing up to that amount (under normal circumstances).

Swiss IBANs for sure. And individual ones per customer - although not in their name. That’s the catch.

IBAN number doesn’t determine deposit guarantee or country thereof.

I would still use Revolut whenever the operating company is not in Switzerland, even if the amount to be charged is presented as “CHF”.

I’ve had situations when the transaction was labelled as “foreign payment” and fees were charged for it, despite the currency.

(I believe with Booking.com or such)

My preference is completely avoiding cards that charge a fee for CHF processing outside Switzerland, but if your main card charges such a fee, it is indeed a good idea to use Revolut for possibly international CHF payments.

To clarify and correct myself: wouldn’t use or recommend them for CHF bank transfers to/from others.

Card payments are fine, and they thankfully don’t discriminate foreign merchants that might charge in CHF (but with foreign processor/merchant location).

Well, same thing as with a local, i.e. Swiss merchant: If you have the transaction currency already, it gets debited from that. If not, it’ll be exchanged from another currency. Which is free, up to a certain amount.

The thing is: Revolut only care about currency (and charge for exchange thereof) for card payments to merchants - little surprises there. No foreign transaction fee. And you always know the transaction currency.

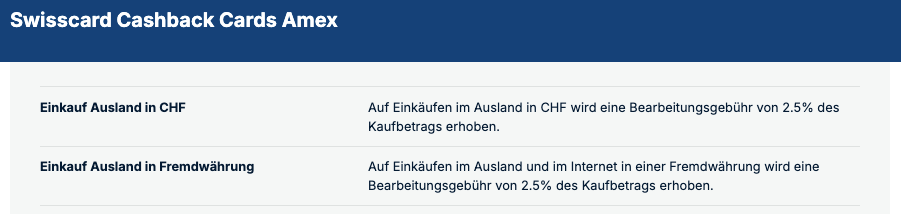

But many Swiss credit cards charge foreign transaction fees - even when paying in CHF. Which can be difficult to find out before you receive your statement.

When buying at “proper Swiss” online shops (Obi, Galaxus, whatever),

they often offer Twint (which is a good indicator of CH base),

so I just use that.

The only reason that I see to use the CH card with a non-CH vendor is if you have some sort of travel insurance cover - which implies you need to pay using that said card.

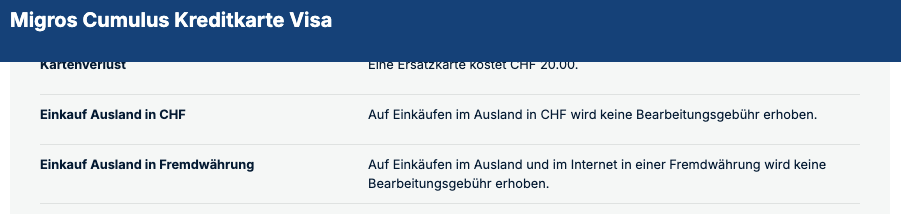

Or get a cc card that does not have this issue, I was so annoyed everytime UBS charged me that not being charged was one of the criteria when I switched

My idea of using the credit card in CHF is to get much cash back as possible. Twint has a CHF 500/month limit if you use it with a credit card. Considering this, what’s the difference between using Twint and using Revolut?

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.