25 years ago, I got my first salary. 10 years ago, I passed 7 figures and got really serious on FI. I can now declare FI victory, having passed into 8 figures. Reflecting back on my journey, I made this list. Maybe it could be useful for those still underway. And certainly I still struggle with the last one…

Financial independence is the ultimate form of freedom. Money’s highest purpose is to give you control over your time and choices.

FI is an internal journey. Confidence, freedom and peace compounds, just like your money, as you go

Most people dont understand FI and think it is to have money to spend money. They will most likely never be FI

Wealth is what you don’t see: buffers, savings, and optionality.

Mediocre/average return is good enough, never ever put yourself in an irrecoverable position by taking on too much risk

Be patient, FI happens slowly, then suddenly. Patience is a financial superpower few develop

FI amplifies your traits because you do things on your terms. That may be good or bad

The goal isn’t to be rich, but to be unburdened. Money buys happiness primarily by reducing worry

FOMO is very dangerous. Remember survivor bias

More money after FI rarely changes your actual life. More freedom always does. This may mean RE - or not, but for FI to be meaningful you should make choises for other reasons than money. If not, you are not FI, you are a slave to more money. FI is not just having enough. It is to not let money rule you

@finalcountdown knows how much I admire their vision and path.

Still there’s one thing not everyone can/will reach, one parameter essential to their success, it’s their uncommonly high revenue.

Hats off for not being a “victim” of lifestyle inflation and choosing the life and freedom you want given the available options, also stick to it as a family.

I fully recognize that income plays a role in creating enough savings - and investment potential. We always saved more than “usual” in %. That is key. We organized our lives in a way that FI was attainable in the first place. 10 years ago our FI number was 2.5M because 100k was plenty as annual spend. Today it is double because we did some deliberate and concious decisions to spend freely on specific things that bring us hapiness AFTER our net worth - not salary- could support it. Had our income not gone up I suspect we’d still be spending 100k and still be FI today because our savings mindset. Who knows.

I also fully recognize the role of luck. We never faced financial hardship, conditions affecting earning power. Never lived in a conflict/war area, had access to education, never hung out with the wrong crowd/ never introduced to drugs. Ended up in professions where good money could be made by luck. That list is long.

Anyone reading this message is already a lucky one. Sure you can always be luckier, but just being born in a reasonable country and having electricity and a device to read this message is already luckier than most.

I’m sure you were not born into your profession, unless you happen to be King Charles Take some credit for the choices you made along the way

We each get the cards we are dealt, how we choose to play them is up to us.

I think Phil’s right, many many people around the world fit these criteria and live hand to mouth. I know a few, in fact most of us know a few, I am sure!

Making the right choices or (as Munger said) making sure to avoid the wrong ones is a huge deal! Enjoy!

Thank you for sharing this - I fully concur with this mindset and hope that in 10 years time, when I’m approx. your age, I will still be healthy and happy with my family and loved ones. Most of the points you’ve collected are also covered by a book most of you likely know - The Psychology of Money. But there is one aspect I liked very much in this book that I wanted to add to this list:

“Avoid regret at any cost. Exponential growth only works if you can stick with the plan for decades and that applies not just to money, but to careers and relationships. Consistency beats extremes. Aim for balance: a solid savings rate, reasonable hours, limited commuting, and real time with family and loved ones. This increases the odds you stay the course and don’t look back wishing you’d traded less life for more money. Because if you die at 60 with a pile of money or get seriously ill, the only real failure is regret. The goal isn’t to maximize net worth at all costs, but to build wealth in a way that still lets you live, love, and stay healthy along the way.”

I have one question. In your original post for FI journey in 2020 the NW was 3.2 M and goal was to get to 5. Did I understand correctly that now the NW is already 10M (8 digits) ?

This is quite a jump of almost 3X in 6 years. Quite remarkable.

Was there a post that explained your investment strategy? Considering the high contribution from salaries you still achieved a 16-17% return every year for ten years.. incredible! how was that possible?

he also just picked (or got handed, this is luck & survivorship bias really) a really good period for the stock market, even plain old S&P 500 did 14-15% over the past 10 years.

The first bucks I had to invest was around 2008. That was probably the best time to start investing.

In my young age, observing what Mr. Market was capable of just made me avoid it. No one could know what would be coming next and the curves looked BAD and SCARY.

So yes, luck but also knowledge and commitment.

And even if things are more accessible, known and sound simple today, through products, forum like this one, ads, neobanks, etc., talking to financially illiterate people today reminds me how much basic stuff you need to learn if you want to understand (a bit of) what you’re doing. I was there.

You need to understand yourself, your relation with risk and money, and it also comes with life experiences - the ones you can’t control and haven’t asked for.

In finance but also in other aspects of life, you may not make the best choice every time, but when you choose consciously and know the reasons why, at the very time you’re acting, it helps avoiding regrets. And if that was a mistake, it’s now a lesson.

16-17%, I wish. Much more modest returns, as I brought in significant new money as well. In 2025, half was return on investments, half new money

my investment strategy? Simple. Before 2016 very little investments, priorities were much different. No regrets. Then until 2021, I put all in low cost ETFs, then 2021-start 2025 all income >250k into pillar 2a. Done with that, is my safe basis. Now diversifying to land on RE asset allocation and leave things alone

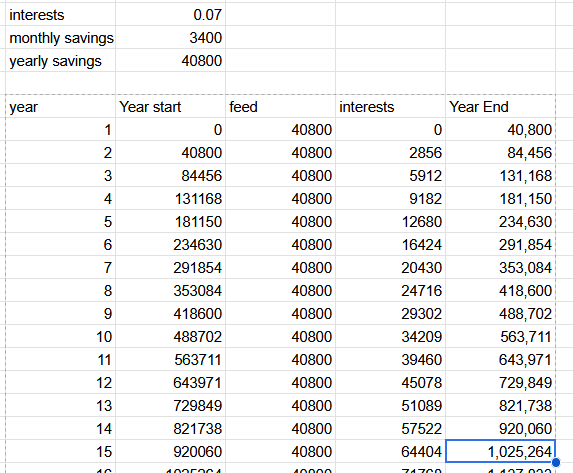

I am intrigued by such a success story. is this generally reproducible? SO i ran a few compounding interest scenarios. assuming “7 figures” means 1’000’000 and “8 figures” accordingly 10M.

the “7-figures” after (25-10=) 15 years i think is quite realistic for typical frugal people with decent income to achieve. assuming yearly interest of 7%, monthly savings of 3400 already get you there

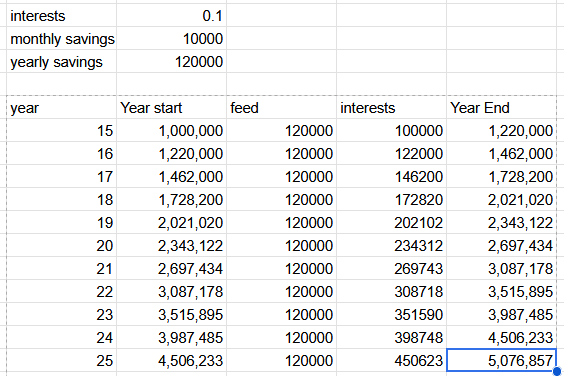

Hence your story involves either serious inheritance, enterpreneurial success or other forms of extreme financial luck that I’d doubt are generally reproducible. But i think you mentioned luck somewhere in this context.

anyway thanks for sharing!

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.