The federal income tax has a very strong progression: It doesn’t really exist for incomes below ~80k CHF and only really kicks in above ~130k CHF. At assumed 5% CR that is far in the seven-digit territory (as your table shows).

Yet, I am sure any change would have to increase taxation for any mid-six-digit amount quite a bit, otherwise it would only hit very few people (and maybe even generate less income taxes as per your example).

Also: What kind of net worth and especially capital withdrawal are you personally aiming for? I thought my examples are showing my privilege, but you hit the ball out of the park with your assumed ranges. I myself expect an eventual capital withdrawal in form of WEF of about 1.25 Million CHF, or at least I did so far.

To be honest, i just selected sum numbers because I wanted to understand the full impact of this change.

If we assume salary of 100 K at age of 25 and that increases by 2% until age of 65. The 12% contributions to 2nd pillar (including employee and employer) would end up with final capital of 1,000,000 CH with 1.5% yield. And 7 K contribution to 3a with 3.5% yield would result in 600K. This adds up to 1.6 Million. These numbers would be higher if employer contribution is higher or if interest rate on 2nd pillar is good or if 1E plans are offered.

I assumed that all money is withdrawn in one shot. I added 2nd and 3a because i think in the end this whole staggering thing would go away.

So i just said okay, what if someone makes 5 times of that , then they would end up with 5.5 million. I know people with income in both spectrums, so I wanted to look into all of it.

I would be happy if i end up somewhere in middle. Really depends how long I am employed. Rest was only for the mathematical purposes as i did not want to exclude people on this forum who might have even higher incomes

What makes me surprised the most is that proposal was made about taxation on pension funds. These funds are already not able to give good returns to employees. We have long way to go to catch with NL etc. and now we are thinking of taxing more the already low yielding funds. Not sure why income tax was not considered which has much more impact. CH is often applauded for forced savings which makes it mandatory via pension laws which eventually should support people in retirement. And then the committee goes after the forced savings where people do not have much of a choice. Whatever the pretext, still is a bit strange.

I would not be surprised if this tax is going to impact mostly the people with high capitals. Someone below 1 million in capital is already taxed higher than income taxes. So any increase for them would not make sense. But based on your other calculation, it seems there are not many people with high capital anyways. This is a bit confusing…

I agree, the more I look into it, the less sense this makes. Equalizing taxation between capital withdrawal and annual pension on federal level is a really odd thing, would be much more logical in certain cantons. Either they really only target very high capital withdrawals, or they mean something different than their statements imply to me.

Anyway, I close this topic for me for now. I concluded that I will still buy into my pillar 2 with a 1e solution this year, and then reassess based on an actual specific proposal and the political process next year.

Other cantons have different non-income basis of taxation.

For example, in my Canton, I was planning for around a 7% tax on the capital. If this changes to an income basis of taxation and goes to, say, 28%, that would be 4x the tax.

So, as long is only the Federal tax treatment changes, I’m not too bothered. If the cantonal tax also changes - then this would be a significant impact.

It details how this is calculated today on the federal level and in each canton. The document is in German and French (each canton in their main language, except TI which got French ).

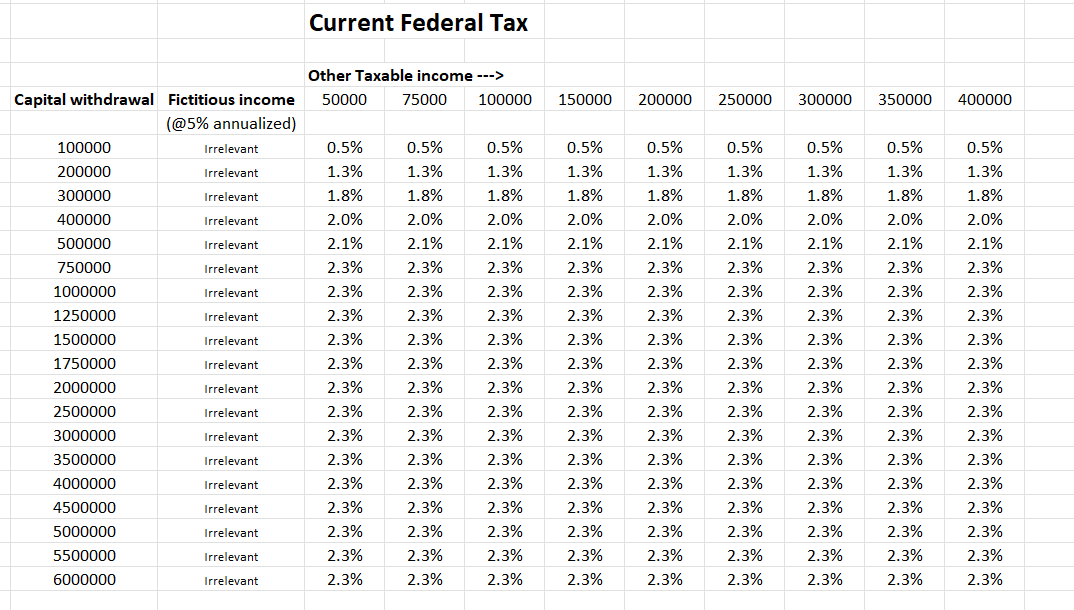

Since income tax rate for incomes above 783,000 CHF is 11.5%, the federal tax for lumpsum is 2.3% for any such withdrawals

For lower withdrawals, a different rate would apply

If tax rule were to change, it appears Federal rule might get closer to what ZH is doing for cantonal rules. And hence the calculation method would need to change. Rather than applying a multiple to tax rate, a multiple to „deemed income“ would need to be applied.

Very interesting thread. May I suggest that we change the topic title? Most of the conversation here is about the proposed increase of the Pillar 2/3 withdrawal taxes.

Besides, the original title was inaccurate anyways: they don’t actually propose savings, they just want to slow down the rate of growth of expenses (with these measures they’ll still spend more in 2027 than they do now).

If this really comes into place, there would be no incentive to pay into 3a. You would be taxed when you take it out the same (except you have less income comp when you pay in) and the money would be locked up.

Linking lumpsum tax to the salary/income of a person at time of withdrawal is very drastic move. Reason being that most people will have higher income at old age vs. young age (when they made the contribution & saved taxes). So I am not sure who would actually benefit from this kind of rule.

But to be honest, as I have not seen (as i am not paid subscriber) the actual calculator or full article from tagesanzeiger, I cannot really say, if this is indeed the proposal

This is much different than what was discussed (which was brining closer the lumpsum tax to tax on annuity) before

Bestimmen der direkten Bundessteuer aus dem Alterskapital anhand der Steuertarif-Tabelle.

Das Resultat aus Punkt 1 geteilt durch 5 ergibt die Kapitalbezugssteuer.

Berechnung nach neuer Regel:

Das Alterskapital wird analog dem Pensionskassensystem mit einem Umwandlungssatz fiktiv in Jahresrenten unterteilt. Dabei ergeben 5 Prozent des Alterskapitals rechnerisch eine Jahresrente (Umwandlungssatz).

Die unter Punkt 1 berechnete Jahresrente wird zum steuerbaren Einkommen im Bezugsjahr gezählt, so entsteht ein fiktives Einkommen.

Mit der unter Punkt 2 berechneten Summe (fiktives Einkommen) wird anhand der Steuertarif-Tabellen die direkte Bundessteuer ermittelt. Dieses Resultat dient nur zur Ermittlung des spezifischen Kapitalbezugssteuer-Tarifs.

Es wir ein prozentualer Steuersatz aus der unter Punkt 3 berechneten Direkten Bundessteuer und dem unter Punkt zwei ermittelten fiktiven Einkommen berechnet.

Der unter Punkt 4 ermittelte Steuersatz wird auf das Alterskapital angewandt. Das ergibt die Kapitalbezugssteuer.

TA:

Was viele ärgern dürfte: Der gestaffelte Bezug der dritten Säule würde nach neuer Regel schon bei mittleren Einkommen steuertechnisch nichts mehr bringen.

As I understand it, staggered withdrawals would still help but the difference would typically be much smaller.

TA:

Wichtigster Punkt: Neu soll die Kapitalbezugssteuer auch vom Einkommen abhängen und nicht nur vom Alterskapital. Das Gesetz soll zudem verhindern, dass man das Einkommen im Bezugsjahr herunterschrauben kann, um Steuern zu sparen. Möglich wäre dies, indem man etwa die Renovierung der eigenen Wohnung genau auf diesen Zeitpunkt hin terminiert. Doch auch dieser Trick soll verboten werden.

This part doesn’t seem reasonable to me at all.

Changing the calculation to be based on a fictional pension instead of simply dividing the regular income tax by 5 may actually be sensible. ZH already uses this approach, if I remember correctly.

However, adding that fictional pension to the pre-retirement income doesn’t make sense to me at all. As I understand it, it might not affect people retiring before 60 much (except for earlier withdrawal e.g. for buying a house) but it would penalize people that can’t retire before they hit the deadline of withdrawing from pillars 2 and 3a.

If the fictional pension was added to the retirement income (AHV, possibly pillar 2), it would at least make some sense, but that would be more difficult to implement. A possible improvement would be to allow withdrawing capital after retiring.

There is a calculator for this (only for federal taxes): Steuerrechner

That earlier the impression was that tax rate would be increased for federal taxes but it would be same for everyone irrespective of what their actual income (salary , dividends, rental income etc) is at time of withdrawal.

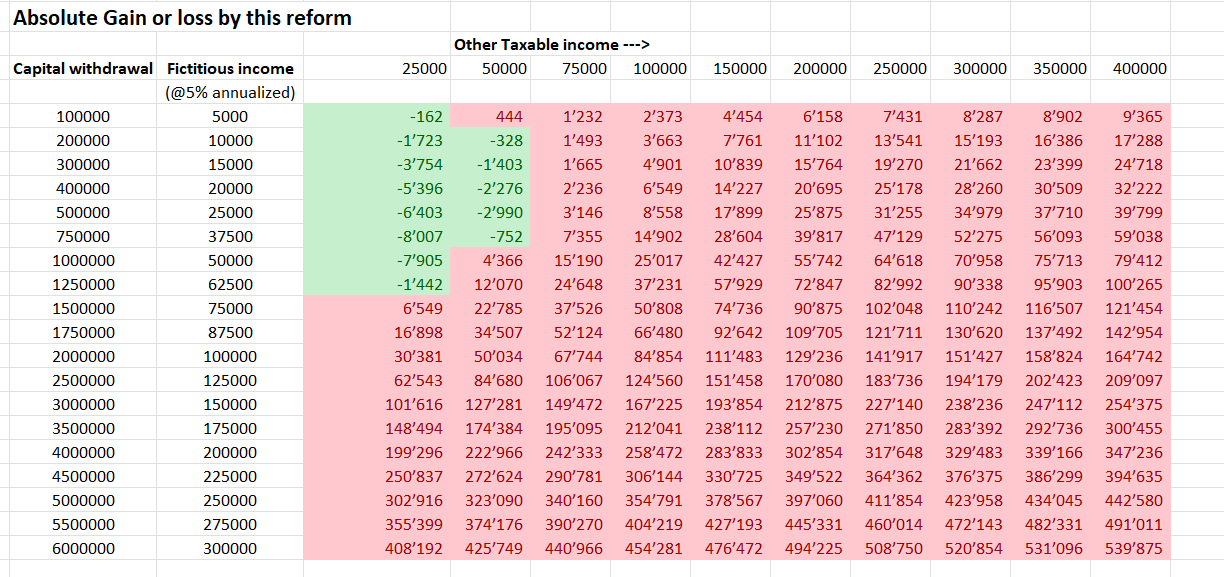

Now it seems the tax rate would depend on individual income. This can mean much higher taxes.

Well, according to this calculator and its description people with lower income. They would pay less federal tax than today.

So it’s better to retire before 60 as from that age onwards you will start to cash out your pension capital. From multiple accounts with your second and third pillar money.

Basically this measure reduces the attractiveness to work for a high income at a later age.

In this case it really doesn’t make sense to save in 3a. Because in this case the capital gain would be also taxed as income when you withdraw. (Except your salary is basically close to zero). Well the last trick of the federal council would be to introduce capital gain taxes.

Yes, it does. Capital / 20 to determine the tax rate, compared to full capital but tax rate / 5 for current federal tax.

Seems fair in a progressive sense. On the other hand, there’s a small minimum % to be paid (4% on average).

Agreed. That’s where the higher tax on this propsal come in, assuming there is still an additional income.

If they keep considering the fictive income seperately, changing to a ZH-like model would benefit anything below 2.3M withdrawal.

We’re still talking 3a, right? This sounds bad, also noting the point below that reducing income for the reference year/renovating a home and other such moves would be prevented. How does this play with withdrawing the 3a from lower tax Cantons like Schwyz?

Sealing the staggered withdrawal loophole is something I’d imagined would be done before long hence I’m not even trying personally.

Based on info shared so far by @jay and @capmac , I came up with following calculations. I will need to read through this again to ensure I understand correctly.

I do not see many people who will pay lower tax versus today unless there is some sort of exclusion.

Please note this is only FEDERAL tax. The cantonal taxes are separate and not part of proposal.

For calculations -: i just used Single person, no kids. But i think similar calc will be valid for other scenarios

Other taxable income = Net taxable Income from all sources as reported in tax return at time of making capital withdrawals

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.