Thanks for sharing some numbers. I agree on average the impact would be not huge.

But , I think the impact would be different for different amount of withdrawals and also different cantons. As shown in Finpension article , the gap between lumpsum & annuity tax is much lower in ZH vs GE (for basic „other income“ of 25000)

Some people wouldn’t get impact at all while some would see higher impact. As always in math, people don’t experience the averages , they experience the deviations

I wouldn’t be surprised if the outcome of this would be that every canton would do different things.

Good point. The 2nd option would work quite well and would be also accepted by society. To be honest it would make everything much easier. No more several 3a accounts, splitting pension fund into 2 vested benefit accounts and other trickery.

But this is only about potential increases in federal taxes, no? So if your canton e.g. has progressive tax for 3a, you’d still profit from a staggered withdrawal.

So a way to avoid these taxes for people who own real estate in the next 2-4 years and have a lot in their 2nd & 3rd pillars. Glad these poor sods have a way out, they already have it tough

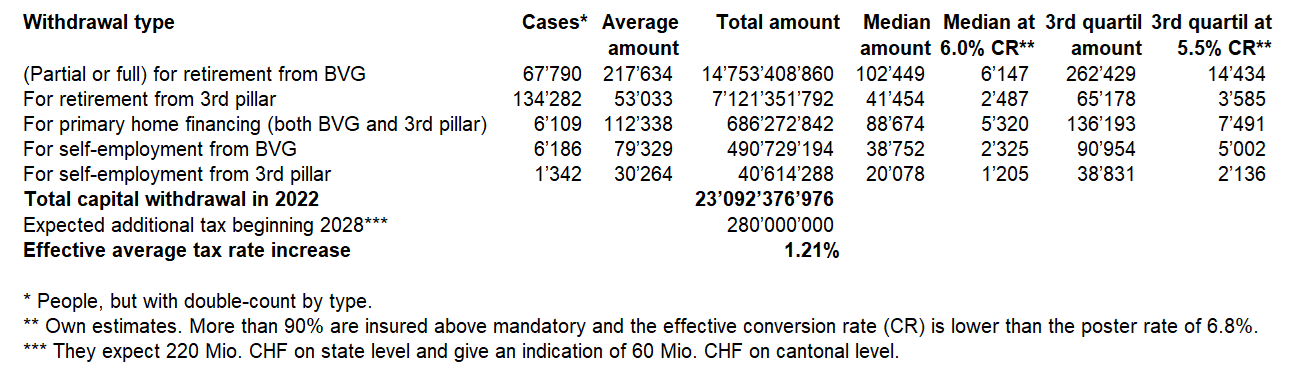

Very good point @Cortana regarding the average tax increase. I have looked at the actual capital withdrawals and did some maths (sources here and here):

Basically: As you said, they seem to expect really only a 1% to 1.5% increase of the average tax rate. But that is because the amounts, on average, are really quite low. Translated into an annual pension the income for taxation for the vast majority (3rd quartile and below), even accounting for an additional maximum AHV income, remains well below 50k CHF per year. At this level, the tax really is a non-issue in most cantons, but this can change drastically for higher capital amounts.

The positive element is, that they must have calculated their estimates by upholding the separation of the income from capital withdrawals from other types of incomes. I am convinced they would have otherwise reached far higher expected additional gains (plus that would kill both WEF/self-employ withdrawals and staggered withdrawals).

I conclude for the moment (won’t have more details until early 2025):

Some change in taxation of capital withdrawal might come, but I consider it unlikely.

If it changes, I would expect it to change not before 2028 (despite KKS partially saying different).

Increase won’t be a big deal for average amounts, but can increase significantly if you have a multiple of the average capital (like many privileged in this forum have). Impact will also be varying significantly by canton.

Despite all these negatives and unknowns, as long as you can choose your own investment strategy, it will still be beneficial overall.

As such, pillar 3a and pillar 2 1e solutions are still a (very) good deal. I would not buy into ordinary pillar 2 anymore, with a lower expected return, where the tax advantage is the only thing that makes it a sensible investment (if at all).

It is part of a large savings package that consist nearly exclusively on reducing expenses. I could see this relatively miniscule (5% of the total sum) part getting thrown out by the left (SP, who fight for higher pensions) and right (FDP and SVP, who don’t want new taxes but rather decreased expenses).

This is for sure the case in my opinion.

Tax increase should be based on some story. The story in this case is not that there are people with high income and people with low income. The story here is that choice of annual pension scheme tends to be disadvantaged (from tax perspective) vs. Lumpsum in some case.

So the calculations need to be based on „other sources of incomes“ which are guaranteed by state (if any). Only thing I can think of is the AHV income which is guaranteed. Not sure if there is anything else.

Everything else like income from Investments (dividends, rental etc) for retirees ideally should not be part of these calculations because that is not a given and will vary at individual level.

I would say people should try to estimate worst case scenario for the effective tax rate for lumpsum and then decide. In some cases 3a or 1E might not make sense if the expected rate is too high.

For example if 2nd pillar + 3rd pillar adds up to X at time of withdrawal, then what could be the worst tax rate if such a law is passed.

I did some calculation based on annual income of varying numbers. I used Zurich city as basis. And just assumed single person , no church, no kids to keep selection simple in the tools.

Following are effective income taxes (all included)

taxable income of 100,000 CHF will lead to effective tax 16.5%

taxable income of 150,000 CHF will lead to effective tax 21.5%

200,000 CHF will lead to 25%

250,000 CHF will lead to 28%

350,000 CHF will lead to 32%

500,000 CHF will lead to 35%

Hence, if we assume lumpsum capital and 5% effective conversion rate, then

If X= 2,000,000 CHF will attract worst case 16.5% tax (today it is 15.8%)

If X = 10,000,000 CHF will attract worst case 35% tax (today it is 26.2%)

Yes, 10 Mio. CHF will be taxed higher than 2 Mio. CHF. But you are just looking at the final taxation event. Where is that money coming from?

In your example the difference in pension capital of 8 Mio. CHF represents your savings that you can choose to either buy-in to your pension fund, or invest freely. At that income level, you will have paid the maximum marginal income tax rate on your income throughout most of your life anyway.

So yes, in the future, you don’t necessary get a tax advantage that way anymore. But you get years or likely decades worth of postponing your taxes, same in savings of wealth taxes (and AHV contributions if you retire early) and it doesn’t cost you anything on the expected return of your investments (as I stated in pillar 3 and pillar 2 1e). What it does cost you is the fact that you pay income taxes on your investment gains (translating tax free capital gains into taxable income). But I doubt that in anything but the most extreme case this yields a different result, i.e. that not buying in is the better option.

They explicitly state that they expect 220 Mio. CHF on federal level and an additional 60 Mio. CHF on cantonal level.

Well I just showed the calculations , there could be various ways to end up with higher pension capital. Voluntary buy ins is one way. But what if someone has a very high salary or a fund with higher interests and employer contributions? They could also have higher sum of money.

Nevertheless, these rates need to be defined in the end using common sense as well. Roughly speaking at 32% effective tax rate, any money added to a 2nd pillar (which might yield 1.5%) would end up being lower than initially added capital post tax. This is not just for voluntary additions but also mandatory additions.

100 CHF added to 2nd pillar will become 99 CHF after 25 years and paying 32% exit tax assuming 1.5% yield. Is this really good use of someone‘s money?

I see your point now. And sure, if you assume that the cantons themselves change their taxation and/or their methodology too, this might look quite a bit different. But AFAIK no one is proposing that, and it is certainly not a technical necessity. We already today have four different methods of how the cantons tax capital withdrawals. See here, again from finpension.

I would speculate that the two simple and realistic options to change the federal level are either

Decreasing the discount. Today you pay 1/5 of the regular taxes, that may be increased to let say 1/3.

Change the federal methodology to the one such as ZH already has today. This is exactly what they state, in which you translate the capital into a theoretical pension and tax it at that level. ZH does it by the way with an assumed 4% conversion rate.

No it isn’t. And let me reiterate: My statements concern only pillar 3, and the special 1e solutions in pillar 2. In those you can freely choose how to invest your capital, and can expect a much higher yield than 1.5%. As mentioned, if your option is only the usual pillar 2, with a yield expectation of just 1.5%, I would not buy-in anymore until potential change is clarified.

Thanks for clarity. I made the following table for current status. Time will tell what gets into the last column. If it would be 1.5 - 2% plus the current levels … or full gap vs income tax would be closed.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.