Yes, the last proposal is from January.

Do we know if the additional proposed tax is for pillar 2a/3a new payments from the day of implementation ( earliest start 2027), for payments that was done less than 3 years prior to implemenation date (so start 2024 in case of implementation start 2027) or retroactively for any payments done at any time in the past?

The latter seems utterly unfair as you buy in under one set of conditions, then get hit with new taxes without any way to mitigate

Those things are not retroactive, a tax change is only applied after it comes into effect.

Question was, whether money paid in before the change will also be taxed more in the future, to which the answer is yes (= ‘retroactively’). So if you paid in 30 years, all of those payments will get taxed more if the change goes through.

Of course if you retired and paid out 2 years ago, this will not affect you.

2 Likes

Yes it is change that would impact all of your pension capital and not just the new contributions

That’s why there was a concern that this change might trigger withdrawals before implementation as people might want to plug money in Real Estate

And yet this has been done countless times around the globe for decades.

I always thought that screwing over those who make sacrifices voluntarily today so they aren’t dependent on the government when they retire would never happen in Switzerland. Yet here we are.

4 Likes

Good day

I also read this discussion about increased taxes for 3a.

I wonder. I have now since many years paid the maximum allowed amount into my 3a, year by year. Also upon advice from my bank, I have changed from a normal 3a savings account to one that uses an ETF, pays a dividend and reinvests. I have now a very good performance, but I am worried - if this 3a tax exemption gets scrapped, I am not so sure anymore if it is really worth putting money into 3a. In the end, what happens is, that this money is basically locked away for a long time. I still have ~30 years until retirement, and if the tax advantage of the 3a would be removed, there would therefore be no further advantage of locking away money in 3a.

I have done some basic research about this topic, but I could not find any information what could happen. So my question is, what do you guys do with your 3a? still pay it, or instantly stop it and just use VT/VTI/whatever on your own, and accept that you have to pay more taxes? seems also not so attractive. I wonder what the best solution could be.

I don’t look at what could happen in future, but make my decisions based on the current laws. Therefore: I pay in full. In 30 years, things could also turn the other way and taxes could be cheaper than they are now. Or nothing changes. You never know.

9 Likes

Same here, already paid in for 2025, even for pillar 2 buy-in.

1 Like

I agree with @markus654 and @Brndete - “law timing” seems about as ill advised as market timing. ![]()

It’s actually not scrapped IMO.

Your pillar 2 and 3a contributions are still deductible from your income (and hence not taxed) and any distributions received in pillar 2 and 3a accounts aren’t taxed, either.

Maybe you should read up on this topic in the thread above to get a better sense for what might change, but in essence (I think) the proposal (still to be) discussed wants to tax capital withdrawals in pillar 2 in the same way (on a federal level) as if you chose to get a pension (which would be taxed as income); ditto for pillar 3a (which of course you can only receive as a capital withdrawal).

I think there are two things at play here for 3a.

- ability to withdraw money in staggered form

- lumpsum rate

I think #1 also impacts lumpsum rate because you can split your withdrawals. So if the govt doesn’t stop #1, ideally 3a should still be interesting

In the original idea, there was also a plan to count individual‘s „other income“ to define the tax rate for lumpsum. I think that is not part of the government proposal.

Govt is proposing simply to increase the lumpsum federal tax rate which would be based on how much you withdraw but it is not based on how much your annual income is.

Given the case that people split their 3a and withdraw over 5 year periods , I would say we can expect payouts in tranches of 100-150k and hence the tax rate for 3a withdrawal is not very prohibitive in my view.

The calculation for this is a bit dependent on individual situation and different tax rates need to be accounted for. But I think in most cases buying a world ETF inside 3a should not be worse off than buying VT in taxable account

The following Reddit thread might be useful

FWIW, even if you had the same withdrawal tax rate as the marginal tax rate at time of contributions, you still wouldn’t be worse off (due to wealth tax + income tax sheltering).

And I find it very unlikely that the withdrawal tax rate would exceed the typical marginal tax rate.

(Also keep in mind that you can easily have 2-3x withdrawal rate difference depending on the canton, so if you do care about that make sure to plan your retirement to live in one of those cantons)

I agree

I added the money in 3a in first week of Jan.

I think it would be fine.

Quick update: This thing is so dead on arrival, that the federal council had to extraordinarily issue a media release this week, reaffirming that they are willing to engage in discussions with the cantons to find solutions (as they’ll otherwise kill it in the Ständerat). The Vernehmlassung still technically runs until May 5th.

Edit: To be clear, this concerns the entire savings packet, not just the specific tax increases for pillars 2 and 3 (which is the most contested measure in the already contested package).

9 Likes

What are the alternative measures that the cantons suggest?

Do we know?

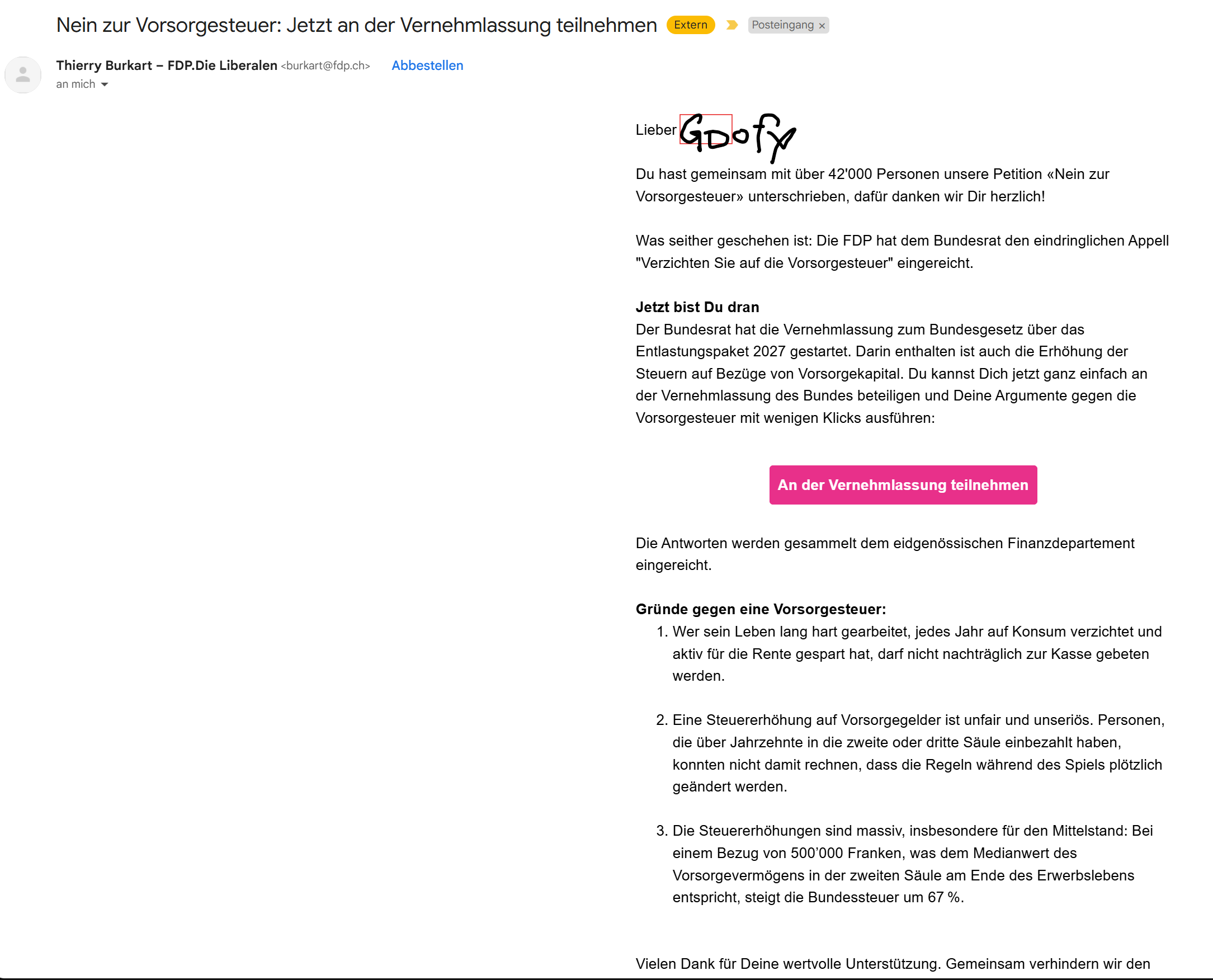

I, as one of apparently about 42k, participated in the petition against this proposal (which the liberal party launched at the time).

Their president keeps sending me personal (ly addressed) emails since. The latest one:

If anyone else wants to participate in the corresponding Vernehmlassung, here’s the link: Nein zur Vorsorgesteuer! - FDP Kampagnen (available in German and French).

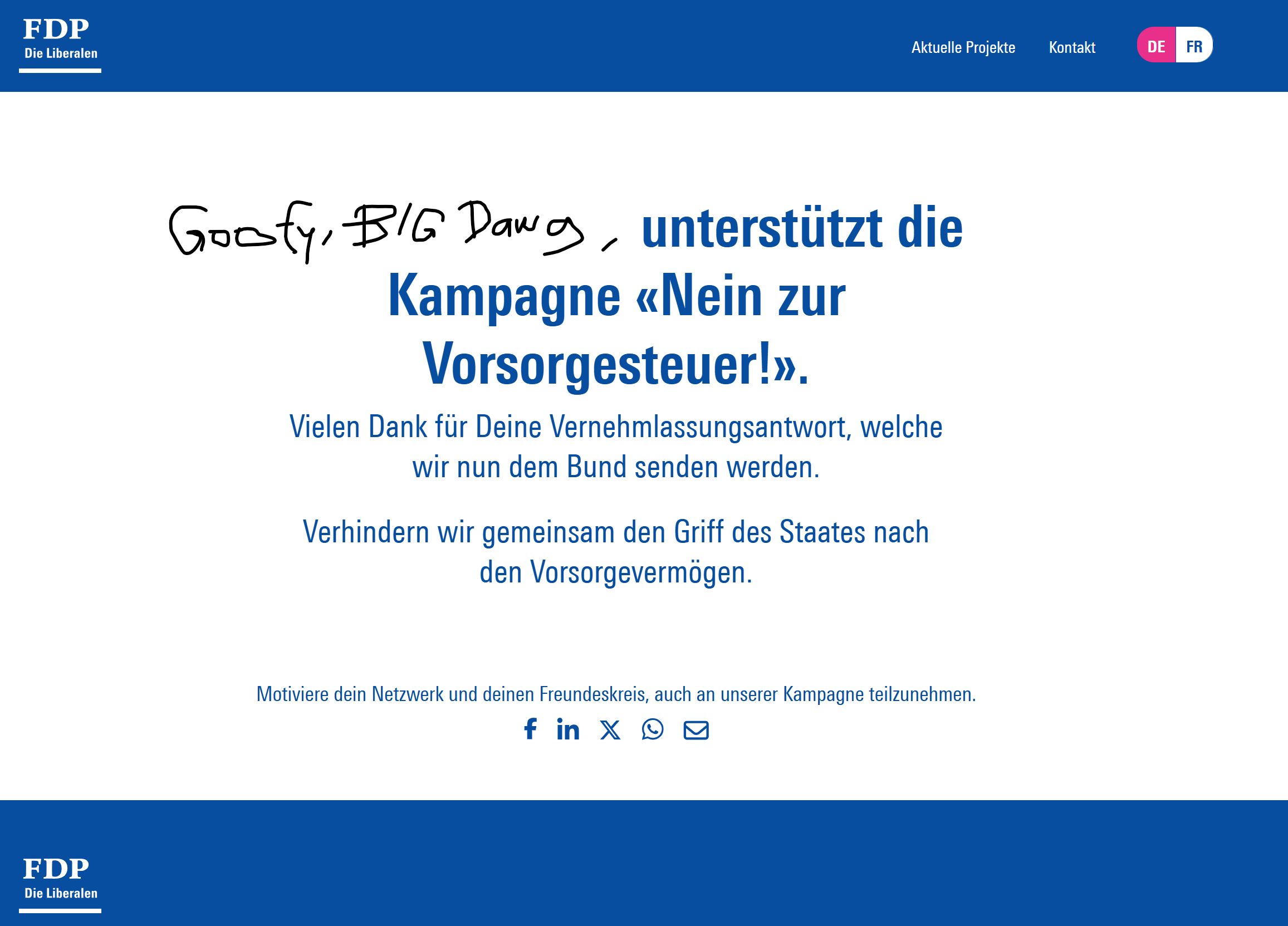

Goofy did his part:

5 Likes

It’s dead. Not formally yet, but Die Mitte has withdrawn its remaining support too.

What remains is a generic left-centric consensus to curtail tax advantageous savings scheme for high earner. That means the buy-in potential into pillar 2 might be limited at some point (apparently Die Mitte floats ideas like a yearly maximum and/or a reduced maximum potential of 50% of what it is today).

4 Likes

The proposal to reduce buy in is interesting but I think it’s a bit strange

The main purpose of those buy-ins are to close pension gaps. This means buy ins are only allowed if someone has pension gaps. So why to reduce it?

In my view put a cap on how much one can voluntarily contribute in a given year might make more sense as it would reduce big buy ins to withdraw soon behaviour

The way I understand it is that the gap is lowered. Closing the gap to a income of e.g. 60k to 100k is fine, but someone rich closing the gap of an income of 200k to 250k (and gaining tax benefits from it) is “a gift for the rich”.

4 Likes

Well. If the rules are going to be different for people for high income, then it’s a different thing

But most of the rules in CH are generally not discriminatory based on income levels.

One can argue it’s a gift in each case.

1 Like