I must admit that my emergency fund is rather small (1 month expenses) because I don’t see what could happen that would force me to sell my ETFs. I get why people in USA have 3-12 months of expenses as an emergency fund, but do we really need that in Switzerland? My situation:

I don’t have kids.

I don’t have real estate, I live in the apartment owned by my girlfriends father (very cheap).

I have a very very stable job situation (my employer would never let me go freely, as I’m one of his most valuable employees).

I’m using public transport and I’m not that dependent on a car. We do have a VW Polo, but replacing it with a similar car would cost us maybe 5k (she would pay it as she wants to be the sole owner).

We have a good insurance that covers basically everything (even vet bills over 100 CHF are 100% covered, or driving a car from a friend 90% covered).

My parents are from Bosnia/Serbia. We have a flat in Pale (close to Sarajevo), where I get free accommodations and very cheap dentists (like 10x less expensive than here, including flights).

I have a very thoughtful budget and different savings accounts (tax, vacation, yearly expenses like clothes, insurances, car expenses) with appropriate standing orders.

I don’t really see what scenario could put me in a difficult situation? Everything what could break (like smartphones, PC etc.) I’m able to replace with part of my monthly savings rate.

The opportunity cost incurred by an emergency fund in cash is huge. I made a small simulation some time ago:

Takeaway is that even if you use your fund often, you will be much better of than by just letting it sit around.

Here is the simulation for someone who invests everything into the SP500 and someone who fills a 21’000 emergency fund beforehand and has a 15’000 emergency every 30 months and a 6’000 emergency every 12 month. Then we look at the net worth of both strategies after 30 years. Data used is the real sp500 including dividends with monthly data.

Thanks for the useful simulation. I don’t really see why an emergency fund as such would be necessary in Switzerland. In Switzerland you already pay good money for ALV/IV/UVG and other insurances to cover emergencies.

I would recommend having some money invested in fixed-yield assets though (i.e. bonds, medium-term notes, fixed deposits). The reason for that is, the stock market can drop and stay down for a long time (as we saw from 2008 till present). The last thing you would want is to have to close your positions while the market is down because you need cash. Yes, the opportunity costs can be high, but potential losses of selling at a bad time can arguably be higher.

The whole point of the simulation is to show that it makes more sense to invest than to hold cash. Even if you have to sell at a loss, you will also be able to buy when the valuations are still low, mitigating the impact a sale at an unfortunate time has.

True that you can subscribe enough insurances that you won’t need an emergency fund. However, assuming that the quants of your insurance company do their jobs, having an insurance and investing the money should be more expensive on a risk adjusted basis.

Concretely, you may want to consider cheaper insurances and have an emergency fund instead. Statistically you will save money on a risk adjusted basis.

Also, in your list of considered risks, I didn’t see breaking up. One of my best friends was dumped 2 years ago and still hasn’t recovered. He certainly had not see it coming (neither did I).

Some insurances are just a nobrainer for me. Health insurance and car insurance is obligatory of course, so they aren’t additional and not considered here.

Household insurance (150CHF/year)

Personal liability insurance (250CHF/year)

Pet insurance (96CHF/year)

Those 3 insurances saved me around 5500 CHF in the last 2.5 years (since I moved out).

I completely agree with you in principle. My point was that holding an “emergency fund” in fixed-income vehicles for the event of a long-term dip in the stock market can be a good financial move. Holding a large reserve in cash would definitely result in a big opportunity cost.

The Swiss social insurance system has about 1 1/2 gaps:

When working, you are insured against invalidity caused by an accident: healing costs and loss of wage. Your benefits here are cut only when you took too much risk. For example a base jumping accident, reckless snowboarding without protection or sitting on the front part of a fast moving motor boat, falling off and getting injured by the propeller.

The more frequent scenario is however not so well insured: invalidity caused by an illness. Health insurance pays doctor’s bills etc. Your employer has to pay your wage for a certain time (he can insure that). This depends upon the length of your employment there. Usually 3-6 months. Now, invalidity rents start 2 years after you can’t work anymore. There can be thus a gap. Some employers, like the Confederation, pay for up to 2 years (not 100%).

The second possible gap is being fired “for cause” or leaving your job yourself. In these cases, you usually get a waiting period at the unemployment insurance.

The above is a description of some risks for the awareness of everybody. It does not argue for any specific amount of emergency money.

Do you know if there is any good and worthwhile private insurance for that? Since as someone working in an office, that would be more realistic than some incident…

Hi Cortana, from what I understand, Swiss Life Protection bunldes disability and life insurance. Is that the case with the policy/premiums you mentioned? If so, I would say that’s pretty reasonable. Most insurers charge you around that price for disability insurance only.

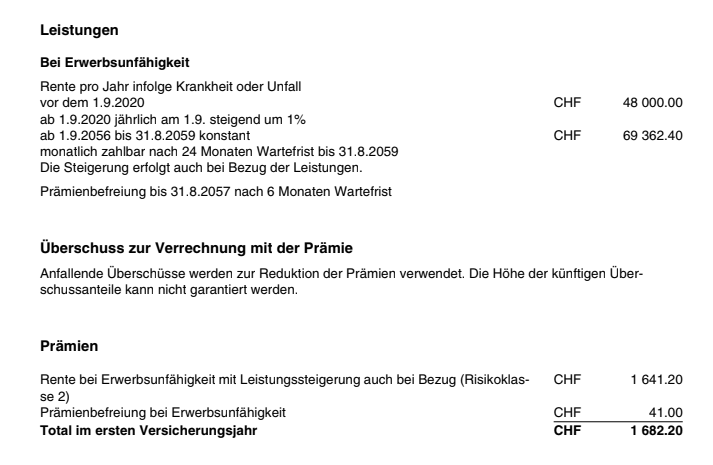

Yeah, because my girlfriend got self-employed this year and isn’t covered anymore by her previous pension fund we had to look into some of these options. I checked with over 10 Swiss insurance companies and came to the conclusion that Swiss Life Protection is by far the best deal.

What’s also great is that they offer an increasing insured sum as you see (+1%/year). You can also increase that to +2%/year if you want to pay more. You are getting 100% as soon as you are 66%+ invalid.

I’m not 100% sure about the death case. I just wrote them an E-mail to clarify that. We haven’t signed yet.

Yes it is, but IV rent is pretty low. So either you have a 2nd pillar with employer or if you are self-employed (like my GF) you make an additional insurance to get to a decent income in case something happens.

As far as I know, the legally-required disability pension you get with the 2nd pillar is based on your pension benefits at the time that you become disabled. If you are young or have only recently begun working in Switzerland, your pension may be very small - same as with the IV pension.

Many pension funds automatically include disability insurance from a third-party insurer. You pay the premiums for these along with your contributions. But not all pension funds do this, and the insurance benefits vary among those that do. So whether or not additional insurance makes sense depends on what disability insurance you get from your pension fund.

Usually you pay a premium listed as risk insurance. As soon as you are insured with a pension fund you will receive the coverage. In case the IV deems you unfit to work, you get the projected balance at retirement based on your current balance and the projected future contributions and the projected interest times the conversion rate.

Even during an illness and invalidity in most cases you should be covered by the IV and the PK (2nd pillow). If and how much you would be covered is available on your “PK-Versicherungsausweis per …” you usually get in the beginning of each year (only for the PK part).

Hopefully nobody gets in this situation! But just in case, there is a always a certain risk that PK and/or IV will analyse your situation differently with their doctors/lawyers and reduce your rent to a certain percentage. So that you might discuss and fight this in front of a court over months or even years. And for that an emergency fund would be really helpful and necessary.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.