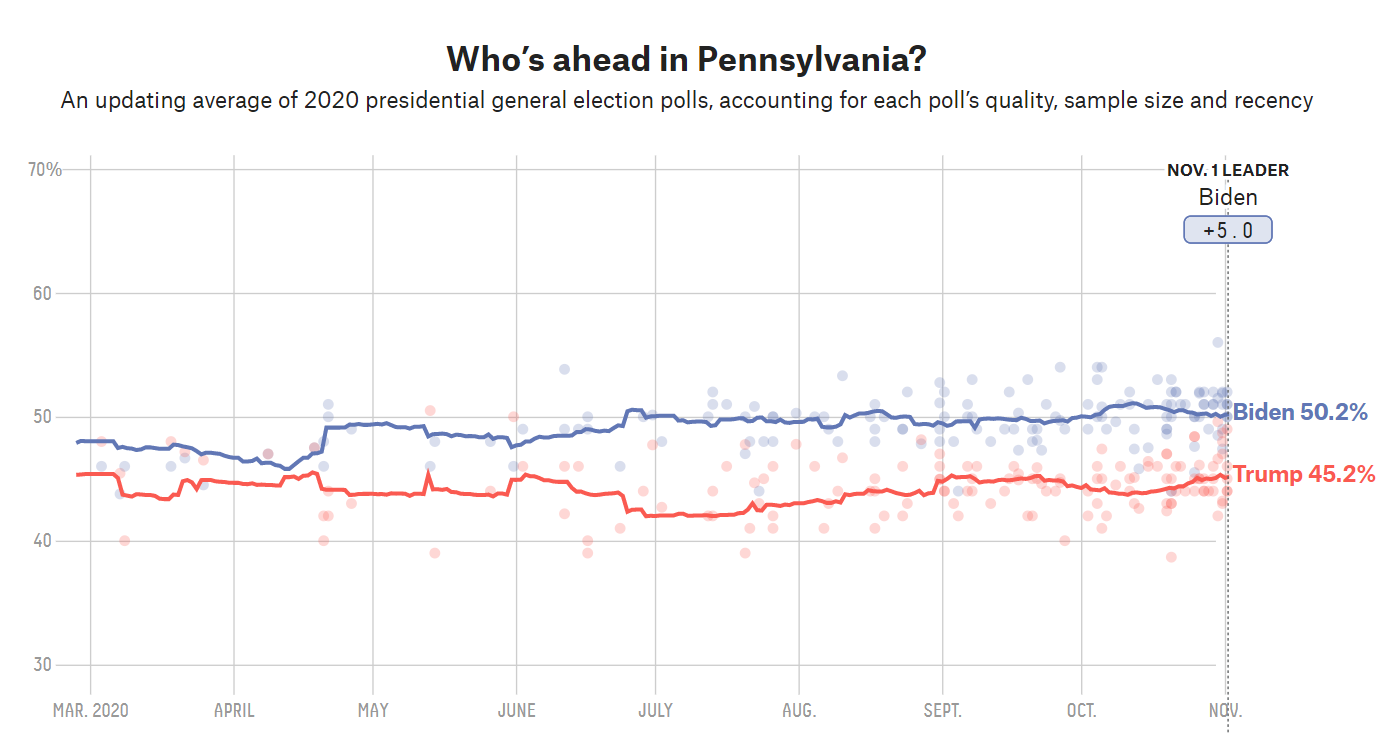

If Biden were to win Pennsylvania he has a 98% chance of winning. According to 538.

Trump needs a polling error of 5%, which would be historical (and much larger than the large polling errors in some states in 2016).

You can toggle swing-state on and off to see how their prediction changes here:

I found this article very interesting about your concern:

That’s a very interesting read. But it’s not about how much you should bet every single time, but provided that you have an infinite number of bets (long term).

So if you see a once in a lifetime opportunity, or you know that it’s the last bet (as it often is the case in poker), things might look different.

The criterion doesn’t guarantee that any one bet leads to an increased wealth (obviously, otherwise you’d require 100% sure bets).

But in order to show why we should use the criterion, the proof refers to what would happen with an infinite amount of bets.

The criterion itself can nevertheless be applied to any one bet.

Alright, I guess you’re right. Cool, this method is really great, why have I never heard about it before?

So let’s put the method into practice.

Bojack

p = perceived probability of win = 36%

b = net odds = 4.000

f = fraction to wager = p - q / b = 36% - 64% / 4 = 20%

w = wager = f * capital = 20% * 100'000 = 20'000

Trotro

p = perceived probability of win = 90%

b = net odds = 0.333

f = fraction to wager = p - q / b = 90% - 10% / 0.333 = 60%

w = wager = f * capital = 60% * 10'000 = 6'000

So if we chose some middle ground for the wager (1.333 for Biden and 4.000 for Trump), I should put 20% of my wealth, but you can put 60%

Man, I love this stuff. Could prove really useful in poker or blackjack.

Yes, it’s fun to play with.

But even just your examples show that the criterion is very aggressive.

If I were to act according to the criterion, I’d use it on some fraction of my wealth I’m willing to use for bets. And if I did larger bets I’d also take into account that I don’t get linear utility out of spending (but I’m not sure how to do this correctly).

Yeah, it really is aggressive. If these were the real odds (20%) vs probability (36%), then I should bet 20% of my wealth? And your case: 80% odds vs 90% probability means bet 60% of your wealth, lol!

It also depends on how often you encounter such an opportunity. The strategy works long term.

If I’d know that such an opportunity would be there a few times per year, then it is quite a no brainer to behave in that way because the likelihood to be in the red decreases with every additional opportunity.

That’s what I meant a couple of posts back, but trotro thinks it applies every time. And, come to think of it, you do run into opportunities time and time again, you just don’t stop to look at the odds. Sometimes they’re small, sometimes they’re big.

I really like this formula, because it lets you consider all these theoretical scenarios. Like, you encounter a great opportunity (invest in a promising startup) and let’s say you have a 20% chance to get a huge payout (let’s say 1 billion, or “infinite money”). The formula says: f = 20% - 80% / 1 billion = 20%. So in such a case, the proportion of your wealth to invest is the same as the chances of success, be it 1%, 20% or 50%.

the criterion tells you that you should only bet if the odds are diverging from the probability of the event occuring. For instance, if a bookie suggests a bet that pays 2-to-1 for an event that has a 1/3 chance of occuring, the bet is properly weighted, and Kelly tells you that f = 1/3 - (2/3 / 2) = 0, i.e you should not bet.

It is not enough that the odds should diverge, they should be in your favor as well. For instance, if a bookie proposes a bet that pays 1-to-9 for an event that has a 80% chance of occuring, the criterion will return a negative number: f = 8/10 - (2/10) /(1/9)) = 8/10 - 18/10 = -1 => do not bet.

Careful with that. Kelly works well only if you can make many times the same type of bet with the same discrepancy between betting odds and probability of the event.

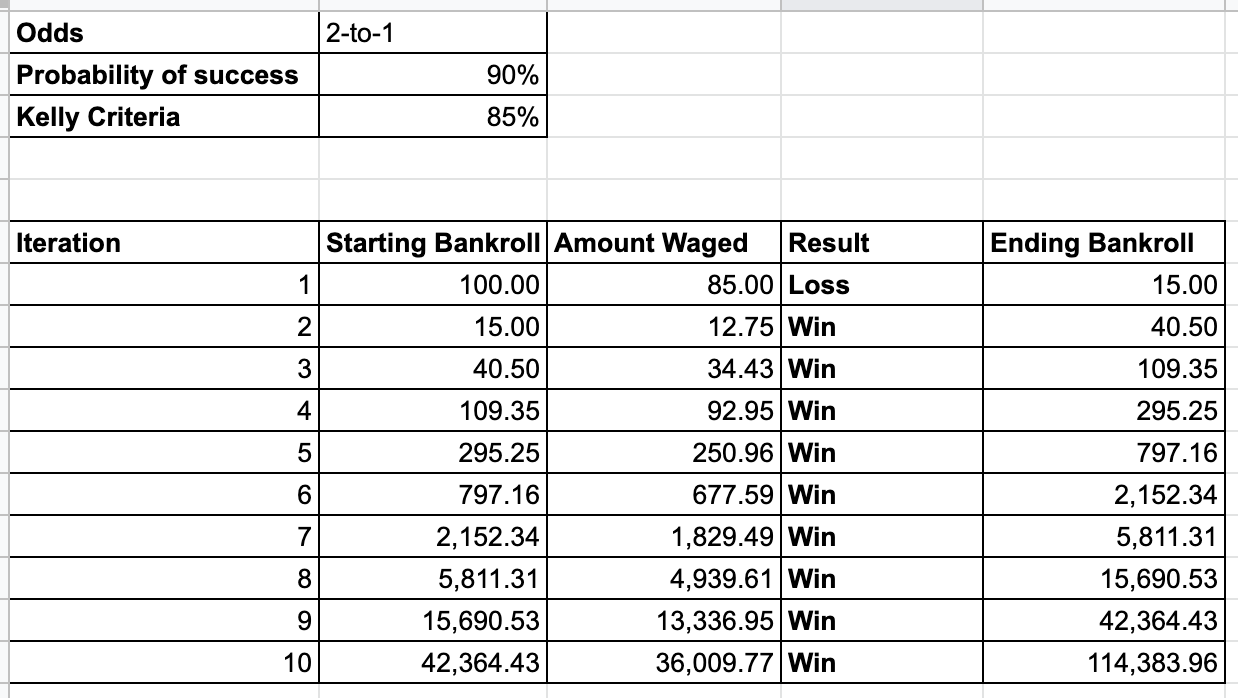

Let me give you an example: let’s say you correctly estimated that a team has a 90% probability of winning a coming game. Then a unsophisticated bookmaker comes and offers a bet that pays 2-to-1 if the team wins. Kelly says you should wager 90% - 10%/2 = 85% of your bankroll.

Even if you are absolutely correct in your estimation, you will still lose 85% of your bankroll 10% of the time, so you need to have at disposal a lot of similar bets with the same discrepancy between odds and probability.

Let’s say that you get very unlucky on the first bet, and the team does not win, and you lose 85% of your money. Now if suddenly the bookie wisens up and all the subsequent bets are not so interesting (say he offers you 12-to-100 for events having a 90% probability to occur), the odds are still slightly in your favor, but now you can only wager 7% of your bankroll that has been already diminished by 85%. In other terms, getting back in shape will take a very long time…

I heard a related topic on the RR/BF podcast, but it was about the other way around:

The premise was the presiding party having an apparent effect/correlation on stock market performance (surprisingly democrats’ periods were better).

But it was in fact a confounding factor at play - the (social) crysis and risk aversion before the elections, that steered the presidential choice (to socialist/dem) and rewarded the ones willing to take risks via the stock markets (with higher reward).

Got it. Yeah, wouldn’t like to take a 10% chance of losing 85% of my wealth. The criterion is surprisingly aggressive, especially for events with low chance of failure.

Good point about the difficulty of predicting how many good betting opportunities will arise in the future!

Assuming you could be sure about future bets, I see another problem:

The Kelly Criterion doesn’t take into account that, in real life, you could become bankrupt/become unable to further participate in games (because you always need some amount of bankroll to survive until the next bet resolves).

The Criterion misses the value of choosing a betting strategy that ensures you can keep on betting, by simply assuming you can continue with any positive bankroll.

So a less aggressive strategy would be to only apply the Criterion on your “expendable” bankroll.

This would be interesting to simulate.

The base model could be something like this:

You start of with a bankroll of $10’000

There are 100 periods, with one bet each

Each period you need $1’000 to get to the next period

Each bet is within a range of positive Kelly Criterion “outcomes”

Then it would be interesting to see what the probability of surviving until the last period is, and what would happen to this probability if you implement some sort of cap on your bankroll (e.g. at most put 65% of bankroll in any bett), etc.

In general it seems like surviving would largely be determined during the first couple of periods.

Yes, this is one of the assumptions of the criterion, you need to be able to do again and again the same bet with the same odds, and this is not a situation that occurs very often. It was used for example by Ed Thorp when counting card at the blackjack tables in Vegas. By counting cards he was able to know when the probabilities were in his favor, and he was able to do these bets many times in the same evening.

He later did this as well with Claude Shannon by using the first portable computer to have an advantage at the roulette table. Here again, you have many occasions during the night to place a lots of bets. Note as well that in these two examples, the betting odds are fixed, but the winning probabilities change during the game and Thorp/Shannon only played when the probabilities were in their favor.

Fun fact: John Kelly was actually a colleague of Claude Shannon at Bell Labs.

No, this is incorrect: the opposite is actually true. Kelly never advocates to wager a fixed amound of money, but a portion of your current portfolio. So if you only do Kelly bets, your portfolio could temporarily go to very small numbers, but assuming you have enough bets to do, you will never face ruin.

Let me take the example again of the bet that pays 2-to-1 if you bet for the team having a 90% chance to win. You might be unlucky on the first bet (and lose $85 if your starting bankroll is $100) but then your next bet will be with 85% of $15, i.e $12.75. You can see that provided that the probabilities are indeed 90%, the amount being waged is always a function of your current portfolio, and your wealth is actually quite big at the end (although volatile at the beginning).

Very interesting!

I guess you’d have to take some kind of “meta”-stance and incorporate the probability distribution of the bets you’ll encounter in the future into your decision strategy.

If I get time, I’ll look into the book

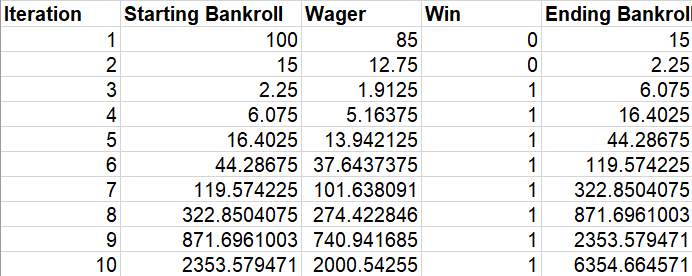

I didn’t mean to imply that Kelly would advocate a fixed amount, just that you might need a fixed amount to “survive” (be able to participate in the next bet).

Something like:

You have $100.

You bet it 85% of it on a bet.

You lose the bet and are left with $15.

You need all of that in order to “survive” and therefore cannot bet on the next bet.

In turn you’re not able to make the gains from future iterations.

But it’s not a strong counterargument. You can always just apply the Kelly Criterion to your portfolio minus the costs to “survive”.

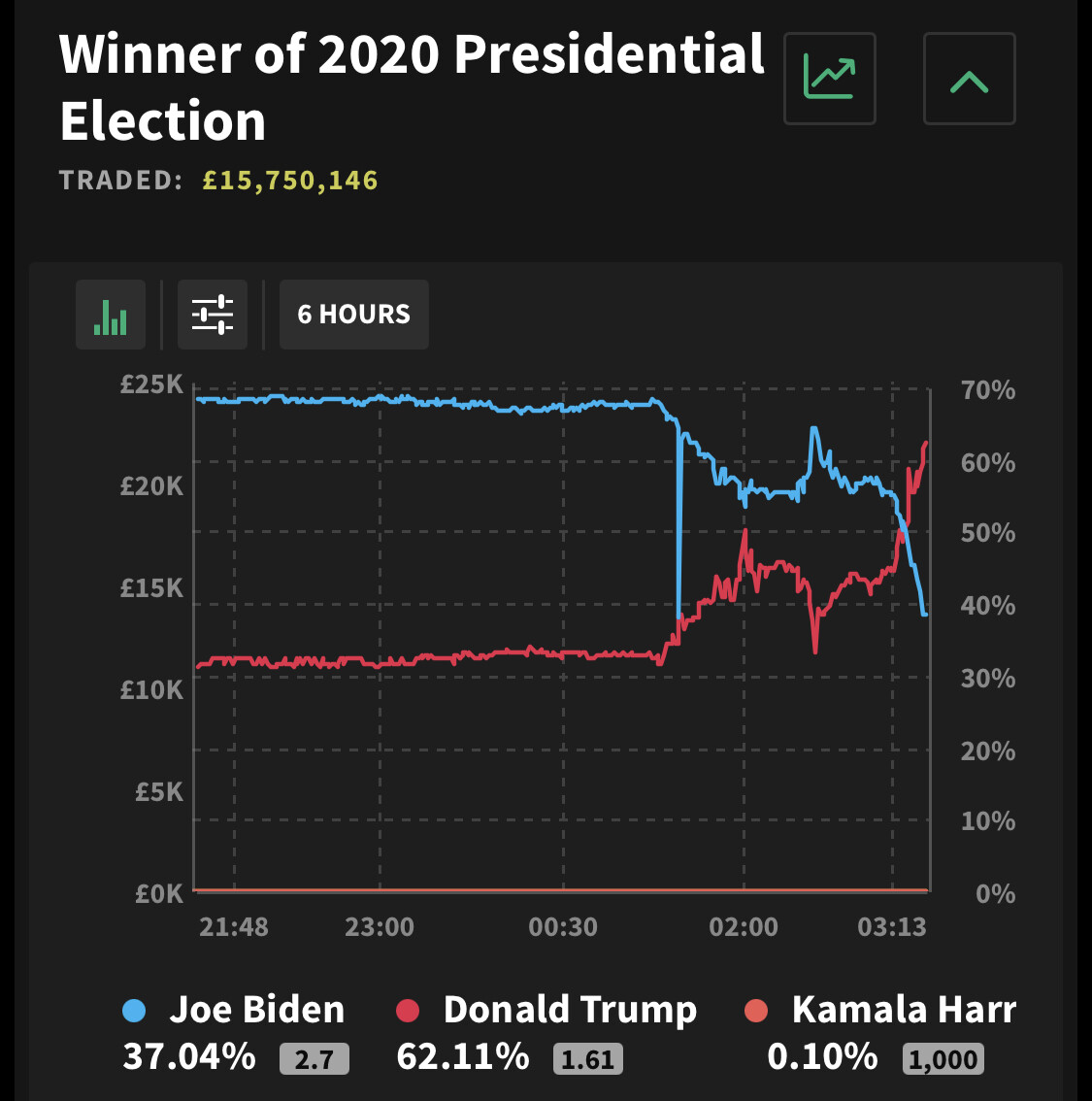

I should be sleeping, but my betting website’s odds just swinged strongly in favor of Trump. Fascinating. Could we witness an even bigger upset than 2016?

Either polling was massively wrong and it’s a 2016 repeat (in fact an even larger upset).

Polling was incredibly wrong in Florida but “only” somewhat wrong otherwise, in which case the race will be tight.

Seems like a lot of the uncertainty right now also stems from the fact that nobody really knows how to interpret the results in key battleground states because of unprecedented levels of early/mail-in votes.

Probably would give Trump a 40-50% now, but haven’t looked into it deeply.

And also slightly updating away from polls working very well in the US (they do work well in many other places), but I’ll mainly do that in the coming weeks.

Flipside, if Biden wins I expect a low prob. of civil war

Polling might have seriously misjudged Latino voters. They certainly did so in Florida.

Maybe has something to do with Floridas Latinos often being ex-cubans and Trumps anti-socialist message?

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.

And your case: 80% odds vs 90% probability means bet 60% of your wealth, lol!

And your case: 80% odds vs 90% probability means bet 60% of your wealth, lol!