The question is if and how you’re going to be eligible for withdraw while (resident) paying taxes in Zug.

By becoming self employed.

The question is if and how you’re going to be eligible for withdraw while (resident) paying taxes in Zug.

By becoming self employed.

Thank you!

AFAIK, it is possible to take the 2 pillar money after reaching retirement age as a lump sum or as monthly payments until death.

Do you know the rules for monthly payments?

How long a retiree need to be alive to benefit from the sum of monthly payments being larger than the lump sum?

The Umwandlungssatz is about 5% (varies from PK to PK), meaning you get 5% annually (in monthly installments) for the rest of your life.

So after 20 years you’re getting more than your lump sum. (ignoring the returns you’d make if you would invest your lumpsum)

…only from a pension fund (not from a vested benefits account).

Link to NZZ Article on withdrawing 2 Pillar when moving abroad.

"The mistake that most expats make is that when they leave Switzerland, they deregister directly from their old place of residence and re-register in the new country.

In contrast, consultants recommend waiting about a month before re-registering. During this period, during which the person moving can continue to live in Switzerland as a tourist, the pension capital is transferred back to their home country. When they subsequently register at their new tax domicile, the increase in assets in their bank account has already taken place"

Not sure what to make of this. Seems borderline fraudulent to announce your departure on date x if you don’t actually register in another country until later

I’m trying to figure out if I should withdraw my pillar 2 and 3 domiciled in Schwyz in one go as non-resident or to make a staggered withdrawal. The Finpension page states that the “max tax rate” for tax at source in Schwyz is 4.8% but what is the progression to 4.8%? Has any one got experience?

Seems borderline oppressive by certain countries to tax pension savings accumulated over decades as „income“ in the year they get withdrawn.

Edit: The canton‘s schedule is here.

Disagreeing with how your residence country taxes isn’t a reason to do tax evasion.

Designing your life circumstances in a way so you don’t get caught by oppressive (or sloppily drafted) rulesets isn’t tax evasion.

From the NZZ article:

The big shock arrived a good five years later: Danish tax authorities informed the woman that she would have to pay the equivalent of 600,000 francs in tax on her 1 million in assets. This despite the fact that she had already correctly paid tax on the pension money in Switzerland. … «The contradictory logic of the tax systems means that those affected fall between the cracks. …»

The solution suggested in the article seems to be to declare to the swiss authorities that you have left and arrived in Denmark, and then in front of the Danish authorities claim that you have not yet arrived and are still in Switzerland

Probably neither authority will find out, but I would not fancy my chances if I had to defend that in court

Thanks but is this only for if I’m still a resident of Switzerland? Is there an equivalent for withholding tax for when I am no longer a Swiss (or EU resident)?

That’s not correct. The idea is that you de-register and wait before immigrating to the other country.

You have to register before you leave the country and in Zurich, you can do so 30 days in advance.

Then you are technically non-resident (maybe a tourist) for those 30 days - assuming you remain physically present in Zurich.

That’s the old and recurring argument of any tax evader and such consultants in Switzerland.

But no, of course it was not “correctly taxed in Switzerland”.

That’s the equivalent to saying “but my dividend was already correctly taxed in the U.S.” when referring to the 15% withholding tax from your VT investment - and then not declaring any dividend in your tax return.

Withholding tax are a means of collecting tax and prevent tax evasion - they are not final personal income tax. Even though Swiss banks arguably blurred the lines during all the years they were happy to offer unreported accounts to foreigners.

As I understand the Swiss-Danish DTA, she would also receive tax credit for the Swiss tax in Denmark.

See my post above.

How is getting a 600k tax bill on a 1 million pension payout not theft?

The topic of becoming stateless was discussed on the forum. I recall the conclusion was it is not possible. You remain tax resident in CH until you establish residence in a new state.

I am no expert but where would you be tax resident during these 30 days? You signed paperwork saying you were going to leave on date x, but then you stayed ?

From what you describe it sounds like Zurich authorities may not care and are unlikely to challenge it anyway

It isn’t that easy. The Swiss authorities can challenge your situation.

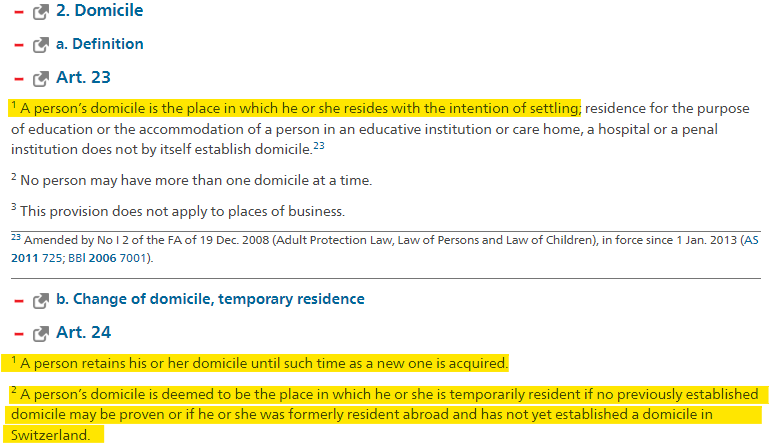

As a reminder, an extract from the Swiss Civil Code

Authorities do not like no man’s land situation.

This topic was already discussed a lot in this forum

It was probably more like 55%+ rounded up.

That’s certainly not unheard a tax rate in Denmark.

On the other hand, it’s often only loosely enforced, particularly with such transitory periods.

I mean, since you’re able to withdraw your pension funds benefits anyway, they wouldn’t collect any more tax - so why bother?

I think the argument in the case of the Danish executive is that her entire pension fund savings from Switzerland are treated exactly like “income from labour”, and taxed like she were an income-millionairess that year, due to incompatible tax systems across countries. The suggestion (not mine, and we can argue whether or not it is borderline) was to avoid having 60% of your retirement nestegg taxed away by avoid being subject to Danish jurisdiction at the time of withdrawal. Isn’t it worth paying at least as much attention to such items as a couple of basis points more or less on a fund’s TER?