In the “pant’s down” thread, someone asked the details of my 2017 spending. Here you go:

|Health|15’574.30|

(as you can guess, this includes the health insurance)

|Taxes|13’780.60|

|Groceries|13’127.82|

|Rent|12’000.00|

(we live in an old building)

|Transports|3’782.40|

|Water, heating, electricity|2’797.90|

|Insurance|2’766.55|

|Charities|2’650.00|

|Kids various activities|2’073.90|

|Presents|1’867.42|

|Clothing|1’725.38|

|Electronics|1’720.90|

|other Non-food|1’640.05|

|Natel|1’010.75|

|Fun|1’010.41|

|Furnitures|1’008.95|

|Dog|568.30|

|Memberships|526.00|

|Holidays|320.25|

|Various|200.00|

|Garden|76.90|

I had the impression to spend a lot! And although to already have cut down many things. Hard to figure out how to spend less although we have a plan to stop owning a car.

ooh now I know why everyone is spending so much in Insurances… the car(s)!

Btw, what’s the total of it?

There is always space for improvement, even if just a tiny bit. I’m sure you won’t spend so much on electronics and furnitures every year, do you? On the other side you might spend more on holidays next year…

I think I pay around ~550 CHF for the obligatory insurance.

I also own a car but manage to fit into the smaller budget. If you need inspiration here’s my old breakdown (I’ll update it later as some costs changed a bit, but I still stick to < 4000 CHF per month budget):

You can also have a look into @Julianek’s budget for some inspiration:

We could also discuss your spending habits category by category and look for room for optimizations, if you’d like.

Here are the car costs for 2017:

|1’692.50|Insurance|

|1’304.60|Tires|

|937.65|Repairs|

|913.60|Gas|

|500.00|City parking mark|

|289.50|Taxes|

|161.50|Parking|

|40.00|Fine|

That’s almost 6’000 for one year.

Here you need to buy a city parking mark if you want to leave your car in the street for more than three hours.

The fact is I feel the FIRE thing is going too slowly. We already have a cheap flat. We don’t have Internet since we share a Wi-Fi connexion with our neighbours. There is no kid’s care as the grand-parents live nearby and take care of them during the school midday lunch break and still I can’t enjoy high savings rates as you guys.

Changing topic, at work I have one 55 years old coworker, very nice guy but he had several health issues recently. We told him he could retire at 58 but he complained he didn’t have enough money to do so. He explained he has only his 2nd pillar and would have to wait some years before getting AHV. Someone told him to save some money but he replied he can’t, he spend every penny every month. At least I’m not in his situation since I have some stash ready. Poor guy… he might even die before retiring.

@1000000 I would gladly accept any suggestion you have. Thanks for the offer.

That’s a nice car cost breakdown. I’m surprised by the cost of tyres. Can’t you replace them in Germany or sth? Or did you have to buy new ones this year?

Gas cost seems a bit low. Did you do only 6000 kilometers that year? That would translate to 1 CHF per every kilometer .

And then there is the implicit cost of car depreciation. I’d say a moderately priced car will lose half of its value in 5 years. E.g. you buy it for 20k and sell it for 10k. That’s 2000 depreciation cost per year.

This appears way too expensive, especially considering you don’t really drive a lot (only 913.60 CHF in fuel, translates to ~570L/year so ~7000 km driven).

Judging by the cost of tires, you either drive a flashy car on 20+ inch wheels, or you were taken for a ride by your dealer. A set of of premium brand summer or winter tires in 16-18" size shouldn’t cost more than 250-400 CHF if ordered online + another 60-80 CHF for having them mounted on rims.

You are also paying loads for insurance, so I assume it’s full casco. Is this feasible? Is your car rather new? Are you aware that the insurance you pay only covers your car up to its current market value, and not to new value, but the insurance rates do not decrease as the car ages?

Repairs? Expensive. If it’s a new car, why does it break down? If old, re-read paragraph above about excessive insurance. Or is it a flashy car which is expensive to maintain?

Another thing missing in your calculation is amortization. Your car is losing value every year, so you should probably account for that in costs of owning it.

I drive 15000km/year and my yearly costs of owning a car including tires (averaged over expected years of use), maintenance, insurance, tax, amortization and fuel is ~3000 CHF/year.

0.20 CHF per kilometer is exactly the price I paid my flatmate when we went for trips. A typical 100 km trip would have a cost of 20 CHF, which we would split in half. But this requires to have an older car, not fresh out of the dealership.

This is why Mr. Money Moustache makes a point of never ever buying a brand new car fresh out of the dealership.

The depreciation curve of a car flattens with age and mileage. If one drives only 6000 km per year, than it makes perfect sense to get a car with 140’000km on the clock as it will only reach 200’000 km in 10 years (if ever). Most cars can do 200-300 kkm without major problems.

Thank to all of you for all the car wisdom in your answers. I have to apologize, following your answers I found out I did a mistake 1’304.60 is repairs and 937.65 is tires. Still it is too expensive indeed.

What I take back from your answers is:

next time we need tires, I can go to nearby France. It will be much cheaper for sure.

as we plan to no longer own a car in the future, the full casco is not necessary anymore. BTW it is a full casco with new value. If the car is destroyed, I get the price of a new car. BTW (again) my previous car was destroyed in an accident and I was lucky to have such an insurance. I know it is not statistically relevant…

Long story short we bought it about 3 years ago at a used cars dealer. It was about 10months old at that time. Without knowing it I did a very mustachian purchase at that time. It is a Skoda Yeti 4wd. At that time we were living in the countryside far away from town, the kids were little, the public transportation not very convenient. But now we live downtown, near bus, Metro, shops all what we need. The car no more matches with our needs.

@ma0 we are a family of four. @all regarding health insurance, when the kids grow up, the insurance fees grow too. If I remember well, when they get 6, the next year you get some increase.

Today’s work story:

Young coworker G. came into our office to talk with young coworker J.

G: did you see? New Iphones released soon!

J: I can’t buy one this year, I’ll next year when I renew my Swisscom contract.

G: I can this year. I’m gonna get a nice new Iphone tomorrow! That’s 1’400* francs but what a nice phone!

Me(thinking): what a piece of shit of a phone you’re gonna get for such a lot of money!

I asked him if it was not better to save the money but he wiped out my suggestion: bank accounts pay such low interest nowadays**, I better buy Iphones!

not sure of the exact sum he mentioned.

** and we work in finance, he should know what compounding means.

The new iPhone is indeed expensive (1199 CHF / 1299 CHF for the cheapest options). I guess anyone who has to work more than 2-3 days to save that amount of money, should not be buying one. Then again, it’s totally fine if you’re overall frugal and then reach deep into the pocket for a few purchases you care about. Especially if it’s gonna serve you 3-4 years.

I’m really amazed that Apple manages to sell so many iPhones at this price. I earn a good salary in rich Switzerland, and I can barely afford a phone like this. In Poland this phone will sell for 5000 PLN, that’s more than average gross monthly salary!

To be fair, some people spend a significant time of their live on the phone so it might be good to not fully cheap out on that. (I would definitely not recommend spending 1k+ for an IPhone but I get why people do it)

What is the deal with companies rising their price ranges lately?

Nvidia is creating a new price range above the old one because they produced way too much last gen chips (lol mining). Apple broke into the 1-2k mark because they like money and Intel is apparently going to push up the prices too. It almost feels like hyperinflation but only in tech XD.

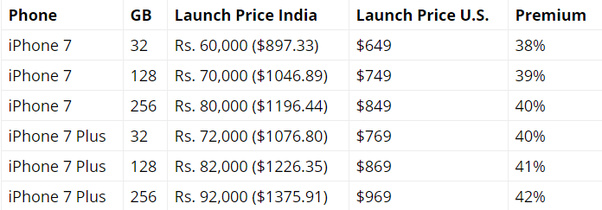

So observe the price of iPhone 7: from 649 to 549 to 449. That’s what you call inflation?

If anything, I guess the appetite for more high end and expensive electronics keeps growing. Rich people like to buy things that not everybody can afford, but oh snap, the iPhone X sold for 1000 bucks and it’s the best selling phone in the World! So I guess we can’t blame Apple.

And you make the same mistake again. You compare better and better graphics cards and say it’s inflation.

The $1199 is the “founders edition” price, the MSRP is $999. And the regular 2080 (not Ti) costs $699. So which one is better, 1080 Ti or 2080? Because they cost the same.

Fair enough, I guess that is one of the perks of having a small product-line.

I say it is like inflation, LIKE. It is of course not actual inflation.

And I am comparing the same tier of cards against each other. Kind of like the big-mac index compairs a big-mac (regardless of if it is made from actual meat or pink slime).

That is exactly the point, we do not know but unless it is an unusual performance increase it is a unusual price increase. Also they very rarely sold at MSRP in the last couple of years.

There is a very big difference with having the same MSRP and costing the same.

And don’t even get me started on this whole “founders” f*ckery.

Also @DrQuasar sorry for hijacking your thread with our shitposting.

Hi again guys ! No problem with the Iphone discussion. I like to listen to other people. It’s a good way to learn things about unknown topics (like Iphones for me) or human psychology.

My thinking about FIRE is not in net wealth but in passive income. I calculated that an after tax income of 60K francs would be enough. At the time being I have some “passive income” investments which I plan to hold forever and some “growth” investments which I plan to balance some day into “passive income”. My passive income is 7’992.-/13.32% for now.

I read somewhere that in Victorian England, rich people were thinking in “income” rather than “wealth”. Like A, who has a 2’000£ income is going to marry B who has 5’000£, that’s not a good match

I like this way of thinking.

Do you have the highest deductible? Have you considered moving to a cheaper insurer? I pay 5741.4 for me, my wife and my one-year-old son.

This is sad. You could consider moving to a cheaper commune/canton. I’m lucky enough to live in Zug where I pay 200 in taxes and I receive 300 back in family allowance.

Have you considered buying in Lidl and/or making some big shopping few times a year in Germany? This could translate into 20-30% lower bill.

This one is actually a pretty good bargain.

This is pretty high IMHO, but I don’t have any advice on how to lower it. I pay ~500 CHF.

What kind of insurance is that?

What’s in this category? Maybe you can promote more cost-less hobbies and sports in your family?

Make an agreement with your family that you cook for each other as a present or organize a picnic or something like that.

I have one advice: second-hand and shop in cheaper countries from time to time (for example on vacations).

I myself try to limit this cost by using less electronics - for example, I don’t have a TV. I keep one computer + 2 smartphones + 1 kindle and we’re trying to use it as long as it is possible (few years).

For example?

This is a phone? That’s pretty high IMHO. I usually use 5-10 CHF per month (+ my wife even less than that). We’re using cheap prepaid - Lyca and CoopMobile.

For example?

I buy second-hand on tutti.ch and ricardo.ch.

My friend have a dog and they buy dog food only in Germany. It’s a lot cheaper.

For example?

This is pretty cheap. Well done.

I don’t have a Garden and Dog, so in my case this lowers my bills few houndred bucks a year, but I still see lots of space for optimisations in your budget.

If you find this sad, then what should I say with 35’000 tax and probably around 25’000 for ahv. If I moved to Zug, the tax would be 25’000 and I would have an extra 2 hours commute every day, so no thanks

In 30 years this young guy who doesn’t save cos there’s no interest at the moment will sound like the older co-worker in your story further up.

“at work I have one 55 years old coworker, very nice guy but he had several health issues recently. We told him he could retire at 58 but he complained he didn’t have enough money to do so. He explained he has only his 2nd pillar and would have to wait some years before getting AHV. Someone told him to save some money but he replied he can’t, he spend every penny every month.”

I have some colleagues like this and it really never ceases to amaze me, cos I’m at a company who pays really really well, and they have been there 30 years.

The only “poor” guys of my colleagues that I can have some sympathy for, are the divorced. I’ve seen enough court cases where they are truly fleeced, although of cos I’m mostly only hearing the guy’s side of the story.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.

.

.