I would just buy a multi family property with 50-60% leverage. You can easily get a 4% net yield on your equity - even if the interest rate of your debt would rise up to 2 or 2.5%.

I know that it’s not diversified, but residential cashflow is stable and you can get insurance for the technical risks of the property.

So with 1 or 2m, i would be looking for a multi family house or two, get 4-5% out of it and my net worth wouldn’t even shrink…

Disagree on buying property to sustain a 4% SWR. It’s pretax anyway and doesn’t include real maintance costs. The value can drop as sharply as stocks did in the last couple of decades.

I am in general sceptical about bonds for swiss investors, and even more about bond funds. If I to have too much stocks exposure in my portfolio, I would rather complement it by cash than bond funds. I would invest sufficient amount in liquid saving accounts, and the rest in fixed term deposits and maybe individual bonds in CHF. With a positive and meaningful yield considering taxes on this income.

And Raiffeisen parts.

So I either have flexibility and if interest rates go down, I can try to shop for another account with higher rates. Or conditions and returns are fixed from the beginning and they are not so easy to change.

The goal for the cash investments is then to keep up with the inflation, not much more.

When I will be 50, I am planning to start building a ladder of 10 years fixed term deposits (Kassenobligationen). The goal is to have it running when I am 60. If you hold them at a bank that issues them, they are insured up to 100k CHF. Now Cembra look interesting in this respect, and we will see what will be the situation in many years.

You’re right, that’s pre-tax. And yes, IF your financing cost is 5% it’s not going to be profitable. Perhaps I am missing something and I’m happy for your comments…

As a simple calc: let’s assume you got 2m of equity, so with a 50% leverage thats a 4m property.

4m with a gross yield of 4% => 160k rent p.a.

Maintenance and vacany of 25%, so -40k; => 120k

Interest rate of 2% on your 2m debt, -40k => 80k = 4% net yield

If at 3% => 60k = 3% net yield

If at 5% => 20k = 1% net yield

These numbers aren’t that bad IMO and that’s with a conservative 50% leverage. You can easily get 60 or 65% debt on a multi family house.

P.S.: I’d buy a property nearby so I’d know the market and could do the property management myself. Otherwise, there’s a cost of another c. 4% of your rental income.

A lot can happen in 60 years, I wouldn’t count on low interest rates to continue forever.

The average gross yield is somewhere around 3.1%, so 4% is already high.

Your calculations also don’t include taxes, conservatively I’d say another 10%.

Are you sure you want to do property management when you are 75+ years old?

You can’t increase rent because of higher inflation.

In addition, what are you going to do in case you have a bad year/a few bad years with low occupancy and the yield is not enough to cover your living expenses? You can’t easily sell part of your apartment.

And I forgot another thing, I’m not sure how dofficult it will be to get such a high mortgage if you have no income. I expect banks lots of banks refusing to give you a mortgage.

I’ve briefly asked moneypark about financing of investment properties at some point. What they’ve told me: the income from an investment property has to exceed the theoretical 5% interest rate on the loan to be considered affordable. I’ve told the agent that this doesn’t appear to be realistic at current prices. He told me, that there are locations in CH where it is apparently possible and that if the affordability criterion wouldn’t be met, then they would look into one’s income as an additional guarantee.

As mentioned above the mortgage stress test @5% on the borrowed amount

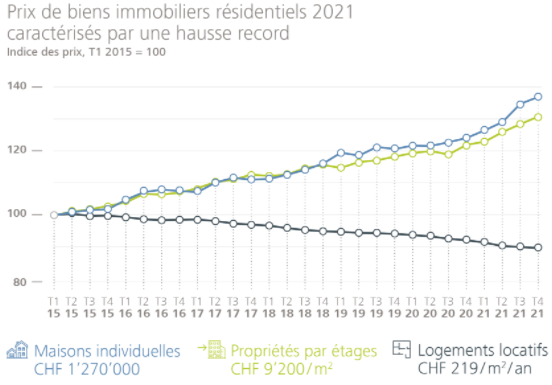

Rents are decreasing due to increase in supply - see chart below from Raiffeisen

Opportunity cost. Equities return 6% long term. On 2m this is average 120k per year hassle free and capital gains are not taxed either whilst you pay tax on rents and on any building price appreciation

Looking at equities another way 12m forward P/E on S&P500 is currently 20 and profits are growing. Even if you can achieve 3% net rent the P/E is 33 and your profit growth is fixed due to rent controls / even declining due to increase in supply

Thanks barto, interesting thougts. My thougts are:

3% net yield is currently and was historically easy to achieve using leverage

True, that’s a big con as it could lead to a default in a worst case scenario. I wouldn’t want to be heavily invested in stocks though in that scenario either, I guess that valuations would decrease significantly for growth stocks and dividend stocks would have to cut dividends…?

So does real estate if you look at total return. But yes, that’s actually a con for real estate as it’s illiquid so you either hold or sell everything. Tax implications are a con too.

I’m certainly biased working in the real estate sector but I just think residential rent is a more stable cashflow than dividend from stocks. That’s my main pro. And you can (currently) get a decent net yield so you can keep the asset and do not have to sell stocks in a bear market hence decreasing your net worth.

If I could afford a multi family house right now, I’d lock in the interest rate for 10 years and would put some money aside to be able to deleverage in 10 years time in order to mitigate the interest rate risk.

Historically stocks on average always performed better than real estate in real terms.

Yes, income tax and also taxes on appreciation of the house value. Maybe it’s too high, I’m not an expert in real estate taxes.

Yes, I know. But if the referenzzinssatz increases, so will your interest costs for the mortgage. Rents don’t rise with inflation, if the referenzzinssatz doesn’t increase.

I assume most of the time the property income is too low to cover the stress test % (5% as far as I know) that banks use for the mortgage affordability calculation.

For most people the goal/strategy for retiring early is not to preserve 100% of their capital until they die. Some even aim for/are fine with capital depletion. So they don’t rely on dividends only, but instead sell part of their stock to cover living expenses. Especially because dividenda are taxed, but capital gains are not.

Thanks for the information, I didn’t know that. Wouldn’t it be hard to find tenants that agree to this? Personally I wouldn’t sign such an agreement.

With this, inflation hits you twice, you pay more rent and you have lower purchasing power.

In the last 10 years my rent hasn’t increased a single time and also none of my friends rent increased. The contrary, due to decreasing Referenzzinssatz I was able to reduce the rent.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.

you can get a brief overview on different data here

you can get a brief overview on different data here