Now, moving from 0 to 4.5 euro / month is not good for me, in particular because I am almost not using the account.

Still I will need a euro account with cheap (free) withdraws from within euroland and cheap (free) SEPA transfer: are there any suggestion from the Mustachian in this forum for an alternative?

If you’re already a PostFinance customer, a EUR account with a EUR Debit Mastercard doesn’t cost anything extra, as far as I know. With the ‘SmartPlus’ package, withdrawal in EUR is free. With the cheaper ‘Smart’ package, withdrawal in EUR costs CHF 5. Not including third-party fees, of course.

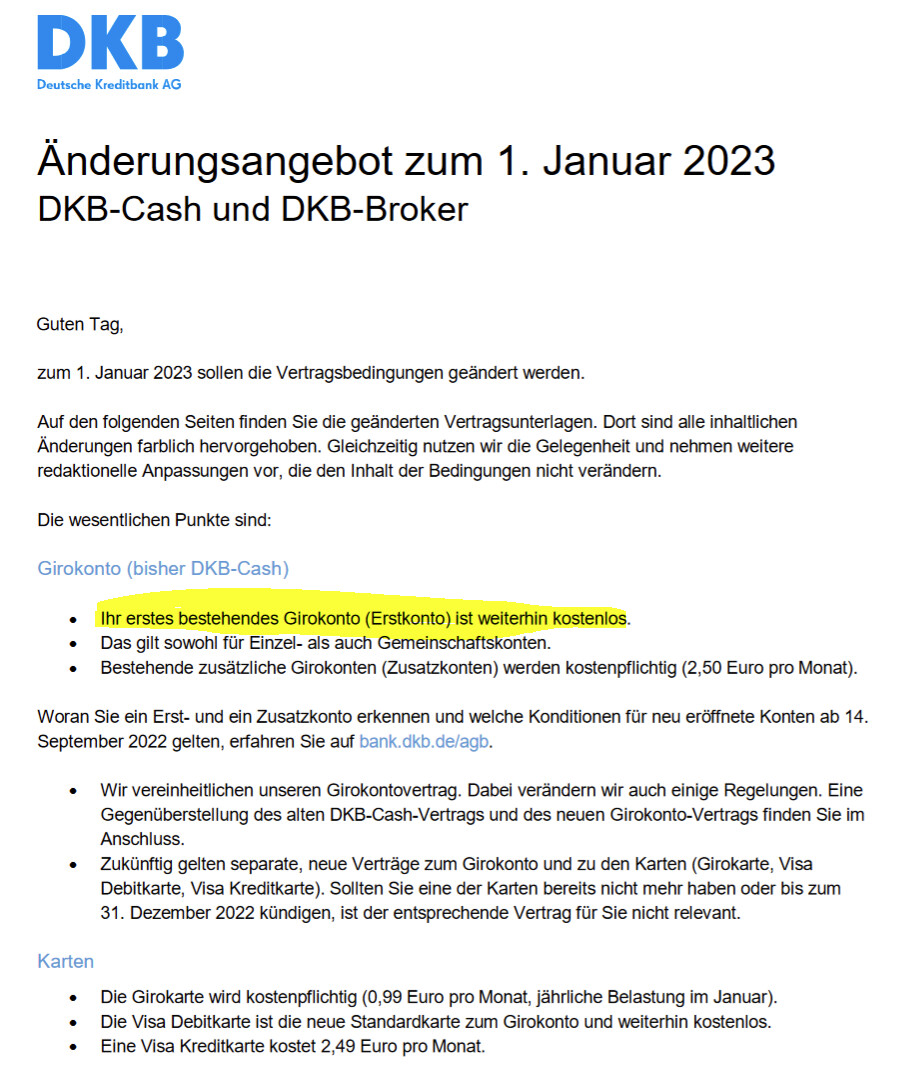

" 1. Das Kontoführungsentgelt entfällt in den in Ziffer 1 e) des Girokonto-Vertrags geregelten Fällen sowie bei Erstkonten, die vor dem 14. September 2022 eröffnet wurden."

How about Wise? (They’ve now made SEPA transfers free)

where they say

“The account management fee at the DKB applies immediately to all accounts opened after September 13, 2022. For existing customers, the new regulation will come into force from January 2023.”

First account opened before 14.09.22 remains free. I can’t find it now but when I first saw this news there was a clause that an account with “active” status is also free. For this you just need to deposit 700+ EUR per month. With more than 2 EUR accounts from IB, Revolut, DKB, YUH, N26 it is possible to organize a cyclical cash flow that doesn’t look like it, if necessary.

I’d assume so as well, but to be sure you’d have to check the current account contract (Ziffer 1 e) des Girokonto-Vertrags geregelten Fällen). The DKB footnote also states that accounts opened before 14 September 2022 would be free, but the article linked above states the opposite. So I’d check the contract to be sure.

Brilliant case of confusing customer communication. Why does everything need to be so complicated? At least the document is more readable without the gender language, now, if they’d only stop with the legalese and just say what they mean…

Sorry, would have translated for you, had I known. Am a bit surprised to be honest, since DKB has (like many German banks though) not been to friendly/accommodating to non-German speaking customers, from what I’ve heard.

Yes - the regulation that says that accounts opened before the cutoff date continue to be free.

They make their money by currency conversion, at reasonable rates (no, I didn’t say “free”).

Receiving EUR is free. They used to charge cents for outgoing SEPA transfers but announced dropping them.

Been using TransferWise for years before I opened my IBKR account and moving my FX conversion over to that. Wise offer cheap local bank transfers in many countries, which is handy when you want to pay someone that doesn’t accept international debit/credit cards (though I don’t mean high-risk businesses by that).

Don’t rely on third-party articles or info - but it’s still going to be free.

Just want to add, as I recently discovered, that some foreign banks (in my case, Italian) charged a hefty fee when receiving money from an account in CH, even though it was in EUR and using SEPA. Such fees don’t seem to be applied when the money come from the EU (i.e., DKB).

The EU regulation regarding fees (fees must be the same for international and domestic transfers) applies only to transfers within the EEA. Avoid banks that do charge more for the few countries outside. While perfectly legal, I’d recommend not dealing with businesses whose pricing schedules have been written by shrewd ****oles.

Though keep in mind when making a bank transfer from your Swiss account, unless it’s friends and family. Recipients may not be amused by paying additional fees and it’s probably often pointless to explain that their own bank is at fault.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.