I am considering having dividend investing as a small portion of my portfolio.

I have already done a lot of work to select, what I consider to be good dividend paying companies to invest in - but then I came across this: Vanguards High Dividend Yield ETF (VYM) (over 3% yield; and TER 0.08%).

I am thinking that investing in such a fund would be a lot less work from my end.

What is your opinion on Dividend Yield ETFs in general?

What are the advantages/disadvantages of such Dividend Yield ETFs compared to building and managing your own portfolio of dividend paying companies?

Don’t do that. In Switzerland, dividend are taxed as income, which is not the case for capital gain.

Even without taking in account taxes, high dividend stocks doesn’t have especially higher returns.

True - I will have to pay taxes on dividends received - but when I retire then I will have to sell my non-dividend paying ETFs and then I will pay tax on the capital gain then or?

Yes - the high dividend stocks doesn’t have especially higher returns - I agree - in fact I understand that often companies that do not pay any dividends at all are likely to have a higher returns because instead of paying out dividends they reinvest the profit into the company - thus giving the company a better chance to grow and prosper - thus increasing the share price.

So is there any reason all to consider doing any form of dividend investing (either ETF or own portfolio)?

Investing for dividends is a mistake even in jurisdictions where they tax you for capital gains exhibit Aexhibit B

Doubly so in Switzerland where you can take capital gains tax free and dividends are taxed to death (I’m paying 40%, it’s practically robbery to me)

If this is not obvious, pick up and do some MOOC on basic corporate finance will ya, or maybe even some basic algebra refresher cause this is like 2+2=4…

@hedgehog - OK so let me get this right: Basically you are telling me that anyone who is investing for dividends is a dumb-ass and should do some basic algebra refresher course…and you’re doing dividend investing yourself and paying 40% tax! I’m sure you don’t need to me draw the conclusion there…

I think people do dividend/DGI investing more for psychological comfort, it’s very reassuring seeing the dollars flow. in some countries like US the tax is actually about the same whether you take profits as dividends or capital gains so it probably doesn’t matter too much, but in switzerland it’s rather dumb to focus on dividends. there are not many other comparable countries without capital gains tax, do take advantage of it. I personally invest for total return not dividends - don’t need the money right now and can always sell later. I don’t actively avoid dividend stocks, anything close to index yield is ok, but high dividend yield usually means less room for company’s growth (or even worse - they just cough back your own money) and more tax for me

Wouldn’t it be worth it to actively avoiding dividend payouts and thus save on taxes in Switzerland, using something like low-yield index funds that still cover (most of) the market? Has anyone done the math on this?

Whether a fund distributes or accumulates dividends is completely irrelevant for taxation purposes in Switzerland. You will get taxed (income tax!) on dividends received by any Fund (accumulating or distributing) regardless of their distribution policy.

I have to agree with „hedgie“ here… actively looking for high dividends doesn‘t seem like a smart move for people taxed in Switzerland.

Accumulating ETFs are given a virtual dividend once a year by the Swiss Tax Office. So it is counted as if the dividend got paid to you and you reinvested it instantly. You can find these dividends in a search tool on their website.

Everybody agrees on the taxation question, of course we prefer untaxed capital gains to taxed dividends. But high dividends can point as well to a poor capital allocation from management.

Let me explain:

At the end of the year, management has to decide what it will do with the earnings they made. They can:

reinvest the money in the business

distribute it as dividends

acquire other businesses

buy back shares

Let’s leave buybacks and M&A for the moment: the capital allocation will depend mainly on:

the profitability of the business

the opportunities of re-investment in the business

We can agree that the best business to own is the one that is highly profitable (ROIC >>20%) and can reinvest its earnings at the same rate in the business, year after year after year. You obtain then a compounding machine, and tax-free in Switzerland.

But obviously, not all businesses are like that! So let’s look at the possibilities:

High profitability, High reinvestment opportunities : this is the above case: the management has better opportunities than the shareholder to reinvest the money, so they should not distribute dividends, but reinvest earnings in the business

High profitability, Low reinvestment opportunities : the business is a cash printing machine but it cannot grow. That is the example of See’s Candies in Berkshire Hathaway. See’s redistributed the earnings to Berkshire Hathaway, tax-free, where Buffett could acquire afterward other outstanding businesses. It only works because Berkshire is a holding so the dividends are not taxed. For the retail shareholder, there is obviously more friction tax wise.

Low Profitability, High reinvestment opportunities: Well obviously the shareholder would not like that management reinvest the money at a low profitability in the business. So re-investing in the business is a no-no. Dividends may be an option, but other options exist as well (for instance, Buffett acquired outstanding businesses (See’s candies) with the earnings of his original very poor business (Berkshire’s textile operations).

Low Profitability, Low reinvestment opportunities : the shareholder still does not want to have the money reinvested in the business. So better pay it out as dividends. However those will be small (low profitability) and poorly growing (low reinvestment opportunities)

So now that we have made this distinction, what can we say about companies paying a big dividend?

They might be in the second configuration, and in this case we should not expect them to grow that much. This is often the case of mature companies where growth opportunities are non-existent. So the shareholder will have dividends, but should not expect the stock to compound that much. Plus, if you are not in a holding structure, you get a lot of friction tax-wise.

They might as well be in the last case, but in this case you have a mediocre business, which is not expected as well to grow.

Sometimes outstanding and growing businesses pay as well dividends. in my opinion this is a capital allocation error, and the company is thus handicapped by the management.

So, in a nutshell, I am not at all convinced by a retail investor chasing dividends…

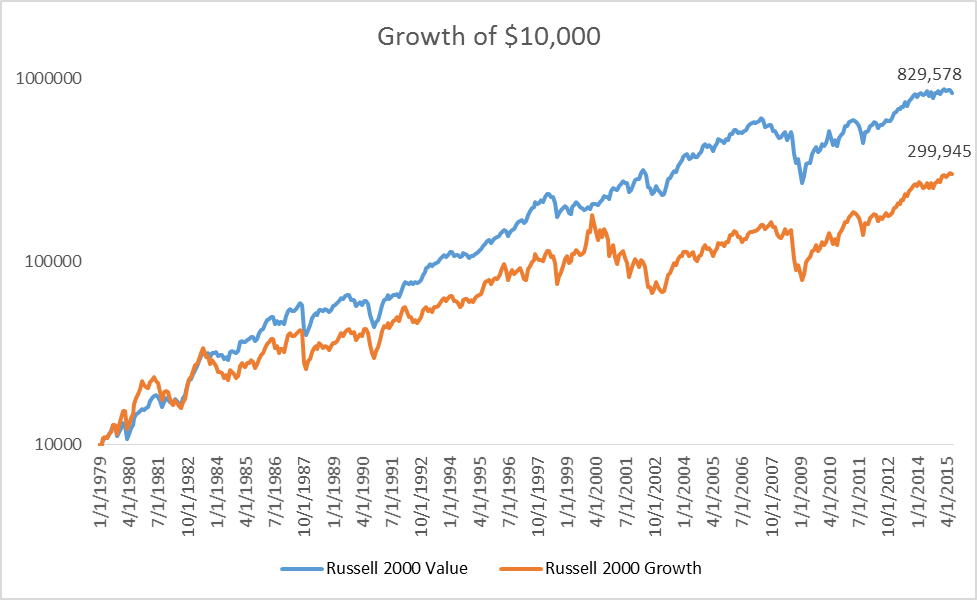

Yes, theoretically. You can buy Growth funds, which have a lower yield. However, until now, Value and Blend funds have shown higher total returns. The reduction in taxes wouldn’t compensate the lower returns of Growth.

Here is another whitepaper against dividend investing:

Funny quote;

Warren Buffett’s Berkshire Hathaway has never paid a dividend. Actually that’s not

entirely true – they paid one single $0.10 dividend in 1967 and Buffett later joked,

“I must have been in the bathroom when the decision was made.”

The case for vs. against dividends is certainly not black or white.

It depends much on the company, its age, its business, etc.

An advantage of a dividend is that it is a always non-negative number - at least, I’ve never seen a negative dividend so far.

Not to be neglected if you want a passive income - isn’t it what Mustachians are looking for ?

Stock price performance can be negative, despite a brilliant management, smart reinvestment, stock buybacks, etc. …

It would be more interesting to see if the companies Berkshire Hathaway is invested in are themselves dividend-adverse. I have the impression that Berkshire doesn’t know what to do with all the cash they earn from dividends (and insurance premiums), and that they have invested this cash in recent years mostly in treasuries, waiting for cheaper stock prices.

indeed, no black and white here, but may be some false hopes on behalf of sellers and buyers.

For my part, I do own a dividend ETF (SDGPEX), but I wouldn’t buy it again if I started all over again. Although I cannot complain so far, it will most probably not fulfill the role I had planned in the long run. I’d roll that part of my portfolio into the existing bread-and-butter World ETF or a value, quality or low volatility ETF.

Here are my thoughts from my finance journal before the buy and my now:

Then: Income-stream

Now → I actually don’t need that for the foreseeable future, as I’m in the saving/investing phase. (The Swiss tax situation was irrelevant at that time point.)

Well-managed companies that look for enough cash to satisfy investors

→ Debatable, as @Julianek has discussed. Dividends may as well be paid at the cost of necessary investments.

Simple way of capturing high-quality or overlooked companies

→ That may be true, but you may need to consider other factors such as P/E ratio, dividend continuity, P/B value etc. See B. Graham’s criteria or an example from a German dividend aristocrat blog. And you can buy a value ETF outright.

Lower volatility

→ Again, this factor can be captured more effectively by buying a dedicated low-vol ETF.

“Compared with other equities, the performance of [investing in high-dividend-yielding and dividend growth equities, J.] has been time-period-dependent and largely explained by their exposure to a handful of equity factors: value and lower volatility for high-dividend-yielding equities and lower volatility and quality for dividend growth equities.”

I do recognize the psychological benefit of receiving a regular and constrained income, and I’m truly fascinated how value and/or dividend investors chose their stocks. But this topic - like much of the whole factor debate - is on my “too hard pile” (a lovely concept I borrowed from Warren Buffet). I’m not convinced that I benefit by focusing on it. I have other things I understand and do better.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.

?

?